This is another crazy day with lots of meetings, so I thought I’d use the opportunity to answer a question I’ve gotten from several members about Adobe.

Tomorrow I have all day to work on a CTA update, which many members have asked for.

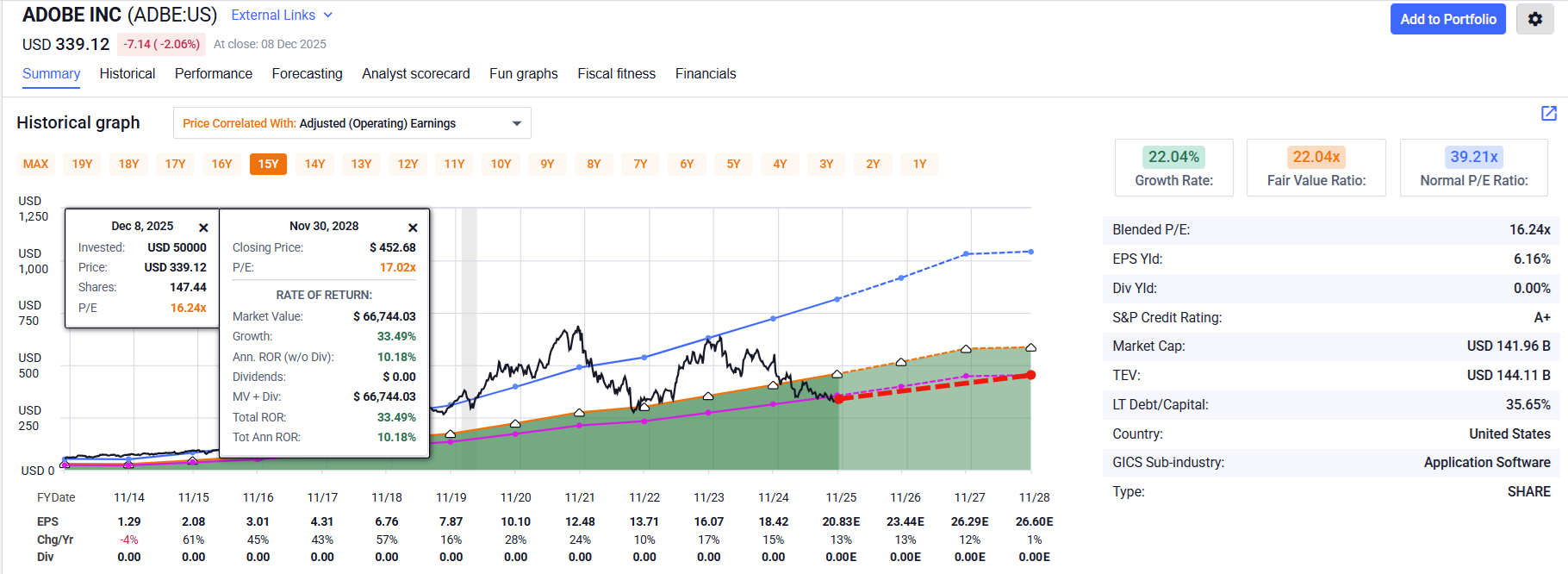

Adobe is releasing earnings on December 10th after the market closes.

Why Adobe Might Be A Coiled Spring Opportunity

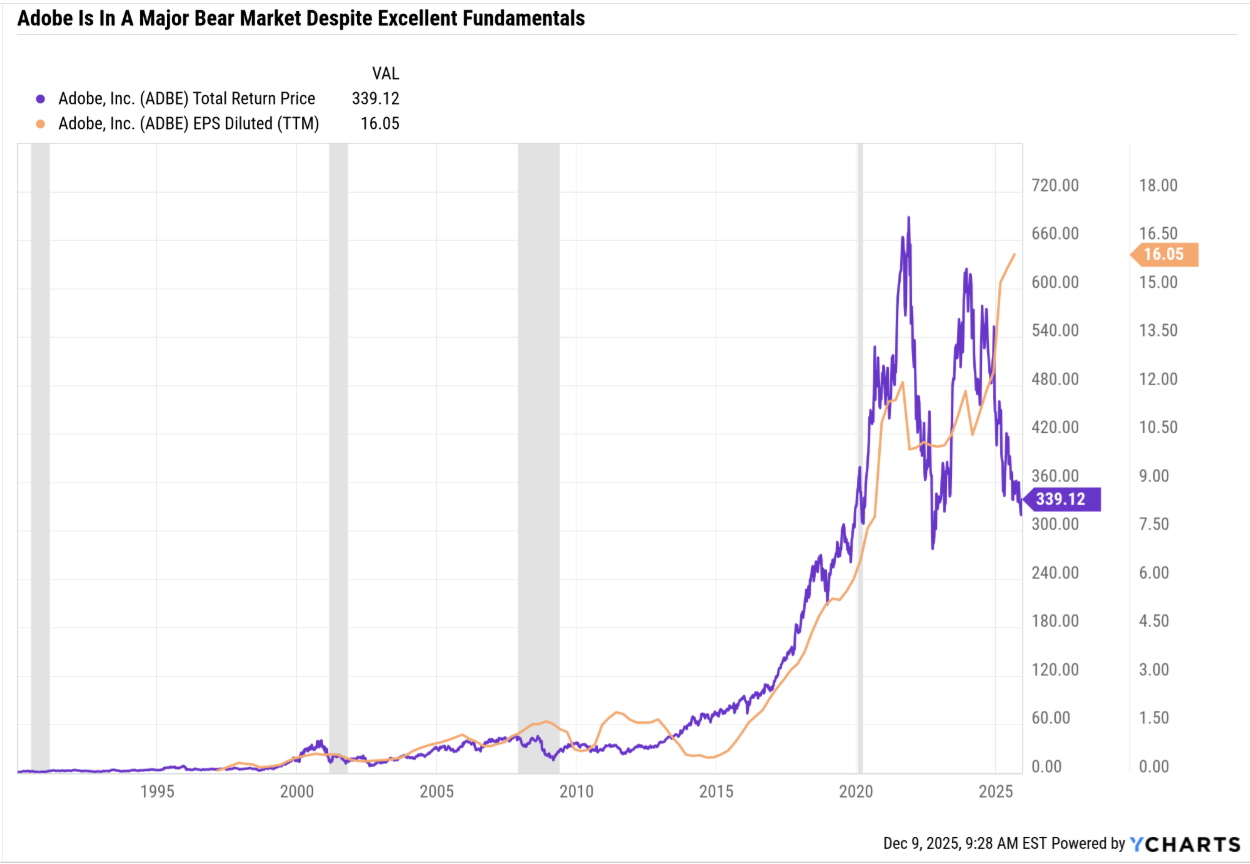

Adobe is one of those rare opportunities in which an A-rated blue-chip crashes…BUT the fundamentals haven’t crashed with it.

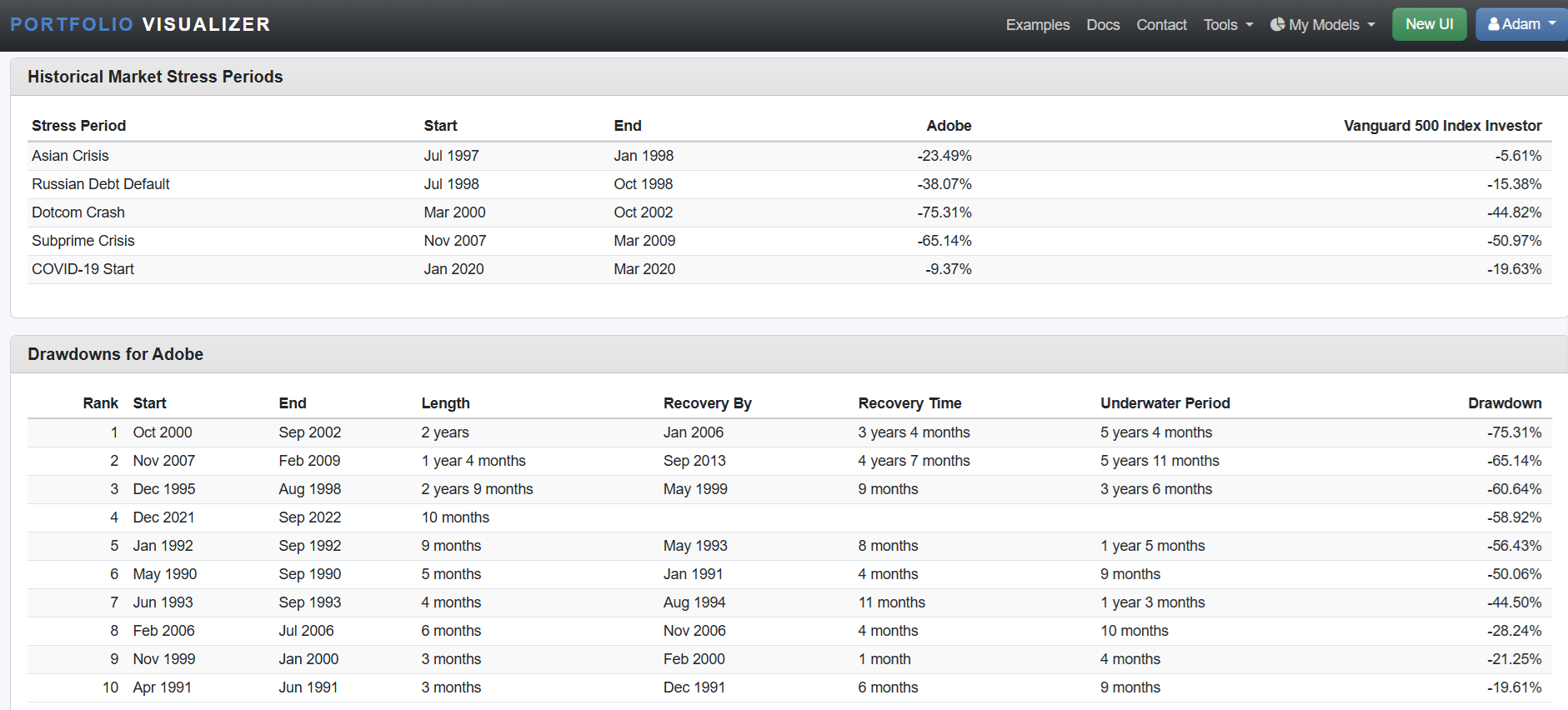

It’s not that Adobe doesn’t experience 50% bear markets; typically, when they do, earnings decline by 30% to 60%.

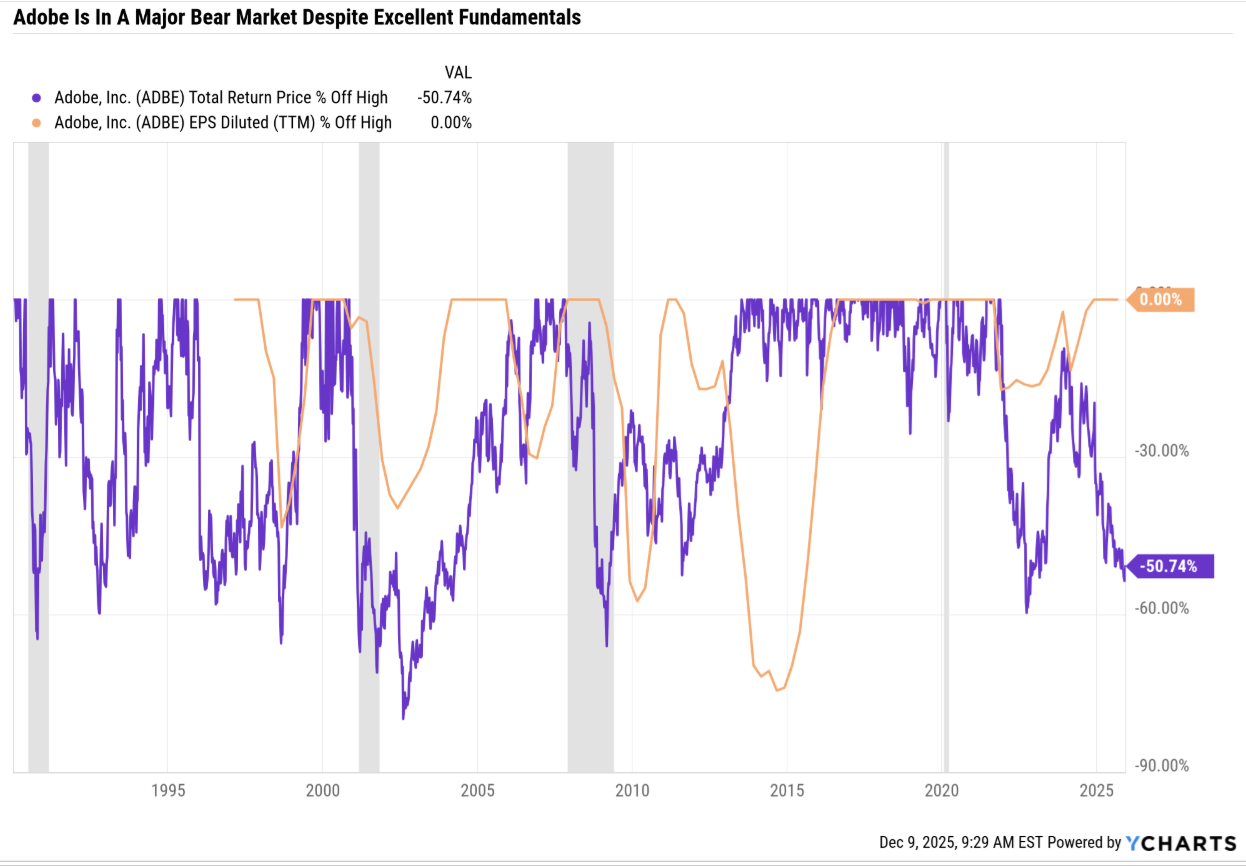

Adobe is in the 4th-worst bear market since 1990, BUT the earnings are at a record high.

The reason for the discrepancy? AI disruption and investor fears that Adobe will be disrupted by AI applications like Sora, Nano Banana, and VEO 3.1, leading to a significant slowdown in growth and further compressing the P/E.

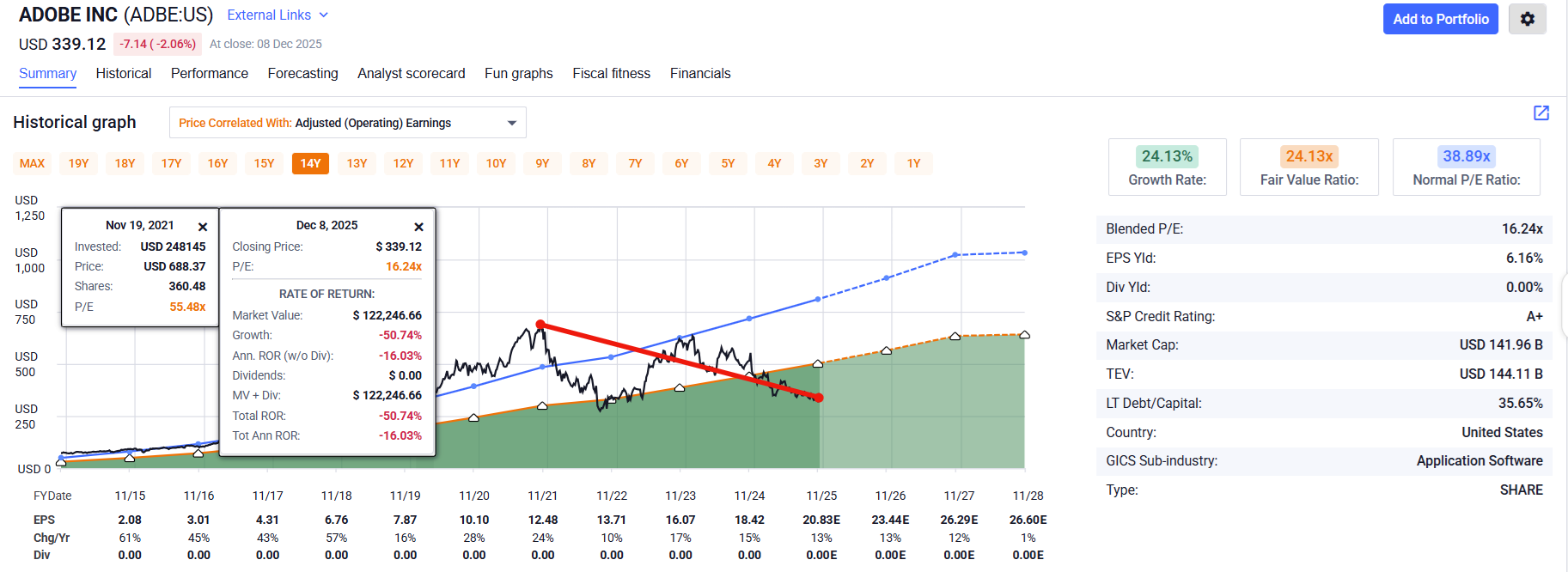

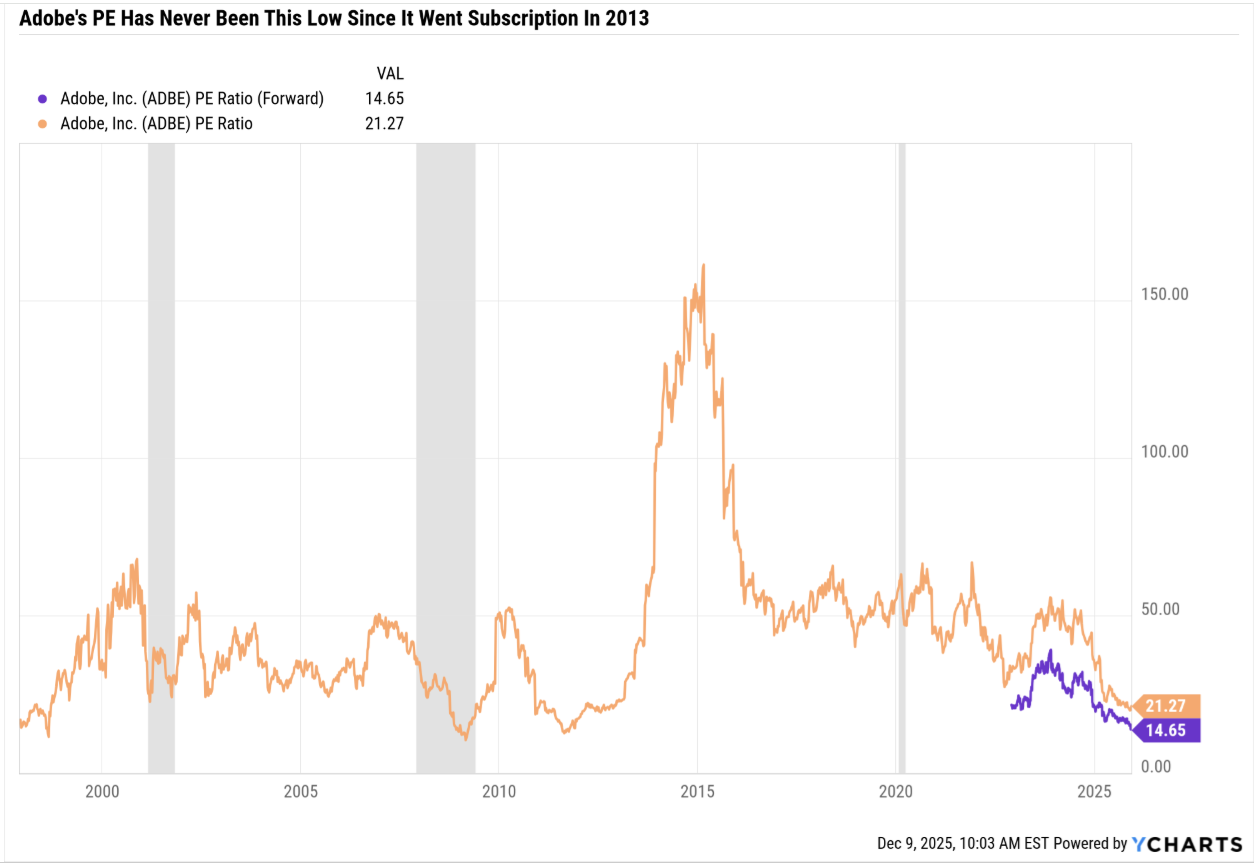

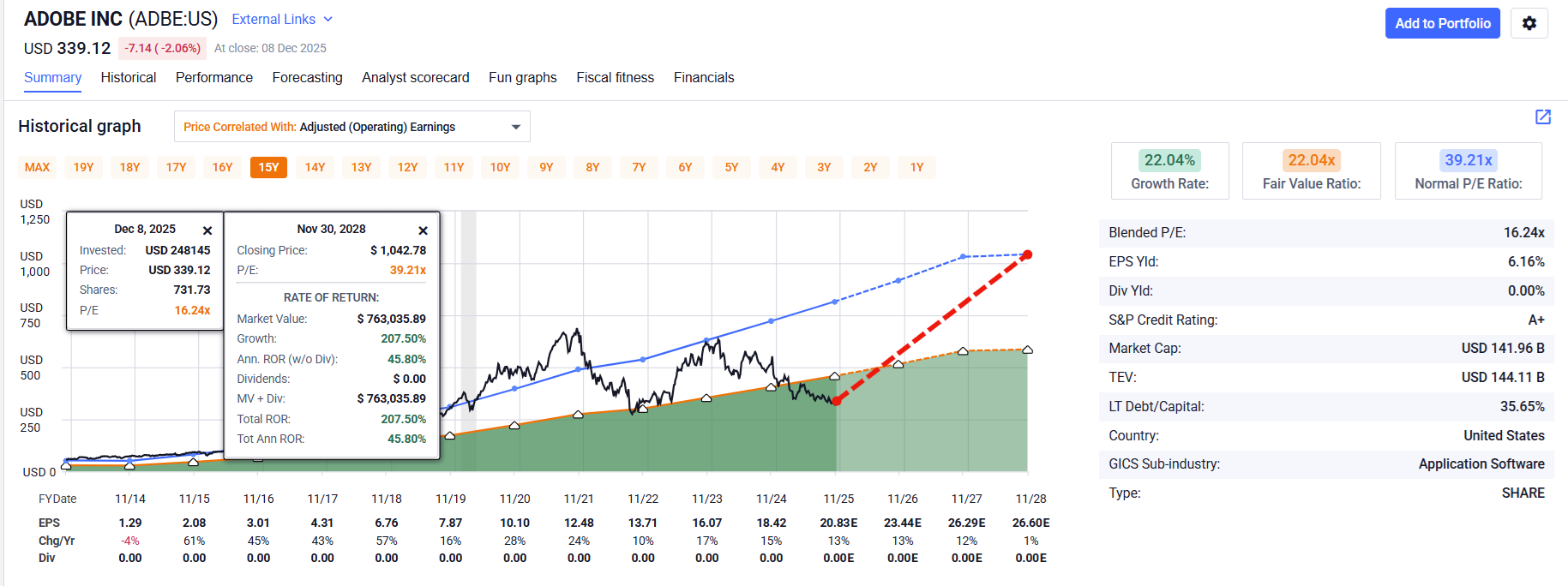

Adobe began its bear market at an elevated PE of 55 (but not in a bubble by any means), and concerns over growth slowing to a crawl (note the 1% growth in 2028) mean that the PE has fallen to levels not seen since before it went all subscription in 2014.

Correction: ADBE went subscription in 2013… so that’s the correct time frame for analysis.

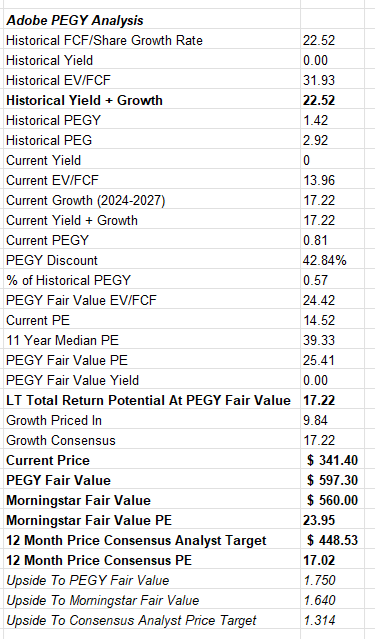

So let’s take a look at the PEGY analysis, and what that can tell us about Adobe’s current nearly 60% bear market. Is this the bottom? Is it the best buying opportunity in Adobe in decades? Is this a coiled spring going into earnings, with expectations so low that ZEUS should buy it today before the market closes?

Let’s combine the best human analysis with the best FactSet consensus data and Morningstar’s Dan Romanoff’s expertise to come up with a comprehensive answer…one that could potentially make us all a lot of money 😉

PEGY Analysis: What Does The Best Available Consensus Data Tell Us?

In Fiscal 2028 1% growth is expected, so does that mean that Adobe’s growth is going to stall out? Are we looking at a PE that might compress to 8.5 (about half its current level, or a 75% bear market)? Or is the growth outlook justifying a much higher PE? Are we looking at a “rising like a phoenix from the ashes to soar to new heights” kind of opportunity?

The free cash flow per share growth rate is expected to slow…BUT only from 22% since 2013 to 17% CAGR. That’s still Mag 7-level growth, and a 42% PEGY discount indicates massive upside potential if ADBE achieves its current growth consensus.

Right now the stock is priced for 9.84% growth so the question you need to ask yourself is this…Do I realistically think that Adobe can grow faster than 10% over the next 3 years?

If you buy today and it only grows at a 10% CAGR, you are buying at fair value, so the total returns expected would be 10% CAGR.

If they grow slower than 10% CAGR, then multiple compression MIGHT continue, though 14X forward PE for an A-rated company growing at even single digits likely doesn’t have much further to go in terms of multiple compression.

And if ADBE can accelerate growth to above 17%? Closer to its historical rate of 20% to 25%? Then the multiple of 14X could return to its historical 31X, which would mean explosive upside potential.

FAST Graphs Analysis: What Kind of Return Potential Are We Talking About?

Bull Case: ADBE Growth Outlook Returns To Historical Rates, And PE Returns Back To 39

208% total return potential = 46% CAGR

You can see the bullish case for Adobe proving Wall Street wrong in its growth expectations could be massive, a more than 3X in 3 years.

OK, but what is actually likely?

Base Case: ADBE Current Growth Outlook Justifies A New PEGY Fair Value PE of 25 to 26

99% total return potential = 26% CAGR

A 3X in 3 years is approximately the equivalent of 3X in 5 years (24% CAGR), so ADBE definitely fits the Buffett-style “fat pitch” bucket in terms of the risk profile being highly attractive.

Venture Capital seeks 3X returns every 5 years for overall portfolios.

So Buffett-style “fat pitches” are a way to earn Venture Capital returns from blue-chip bargains hiding in plain sight without fees or locking up your money for 7 to 15 years.

Conservative Case: Continued PE Compression (17)

33% total return potential = 10% CAGR

The current analyst 12-month consensus implies a 17X forward earnings multiple, suggesting a 10% return potential over the next 3 years.

Bearish Case: Growth Outlook Falls To Zero (8.5 Rule of Thumb PE)

-33% total return potential = -13% CAGR

ABDE has potential downside if the growth outlook deteriorates, though most likely it will deliver double-digit returns over the next 3 years (10% to 25% CAGR).

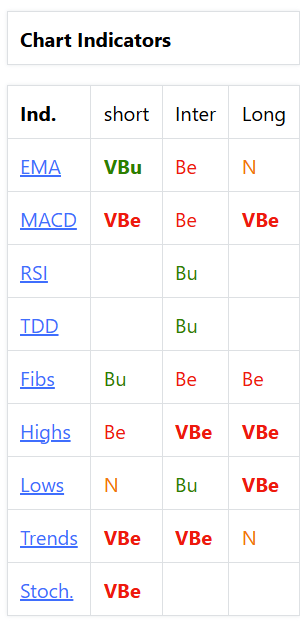

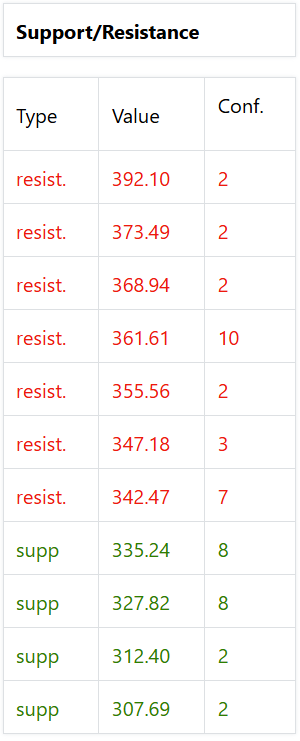

Technicals: What Are The Trading Algos Seeing?

Adobe isn’t in free fall, BUT the algos are not that excited because they are potentially seeing the recent rally off the bottom running out of steam.

For Adobe to become a Wall Street darling, it would need to close above the $361.61 resistance level, which is very strong.

If Adobe Pops 6% On Earnings, the Algos Will Likely Interpret It as “Breakout, Everyone Into The Pool”

The question is… is the 10% to 25% CAGR likely returns from Adobe worth the company's overall risk profile?

Personally, ADBE looks like an excellent opportunity that I would LOVE to own BUT due to launching GNG and having to fund $43K in monthly expenses during a period of no revenue I am unable to justify a 3X in 3 years starter position simply because ADBE doesn’t offer superior return potential to what we already own.

Adobe (ADBE): The "Content Supply Chain" for the AI Era – Comprehensive Investment Report (2025-2030)(Gemini 3 Pro Deep Think, FactSet Consensus Database, Morningstar’s Dan Romanoff)

One Sentence Summary Adobe is evolving from a software toolmaker into the "Central Nervous System" of the digital economy, leveraging its commercially safe "Firefly" AI to dominate the $200+ billion content market while maintaining massive profitability through 2030.

TLDR Summary

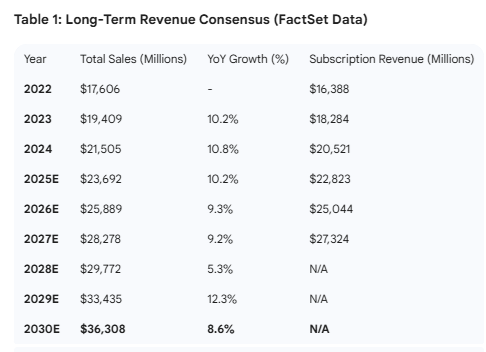

Financial Consensus: FactSet data projects Adobe to grow revenue from ~$17.6 billion in 2022 to $36.3 billion by 2030, maintaining a steady growth trajectory while driving Earnings Per Share (EPS) to $32.20. This confirms its status as a "Compounder" that grows reliably rather than a volatile hype stock.

The "Safe AI" Moat: While competitors like Midjourney face copyright lawsuits for "scraping" images, Adobe’s AI (Firefly) is trained exclusively on images Adobe owns. This makes it the only "commercially safe" option for Fortune 500 companies (like Coca-Cola or Nike) that cannot risk getting sued over an AI-generated ad.

Strategic Pivot: The company is successfully linking its creative tools (Photoshop) with its marketing data tools (Analytics) to create a "Content Supply Chain." This allows them to sell massive contracts to CEOs who need to not just make ads, but manage and measure them across the globe.

Defensive Edge: Morningstar assigns Adobe a "Wide Moat" due to Switching Costs. Because the entire creative industry standardizes on Adobe files (.PSD, .PDF), it is nearly impossible for a professional agency to switch to a cheaper competitor without breaking their workflow.

Expanding the Funnel: To fight low-cost rivals like Canva, Adobe launched Adobe Express—a simpler, web-based app. This captures students and small business owners early, creating a "farm system" of users who will eventually upgrade to the expensive professional tools.

Valuation Opportunity: Trading at $339 (as of Dec 8, 2025) against a Morningstar Fair Value of $560, the stock is trading at a 39% discount. This suggests the market is irrationally fearful that AI will kill the design industry, creating a "margin of safety" for investors.

The "Seat" Risk: The primary investment risk is "Seat Compression." If AI makes designers 10x more productive, companies might hire fewer designers. Adobe must successfully pivot to charging for "AI usage" (Generative Credits) to offset any loss in the number of user licenses.

Capital Powerhouse: Adobe is a cash machine. With projected Net Income exceeding $14 billion by 2030, the company has the firepower to aggressively buy back its own stock (reducing share count) and acquire emerging startups, securing its long-term dominance.

A Picture (Or Table😉) Is Worth A Thousand Words

Analysis: The company is effectively doubling its size during the AI transition. The growth is not explosive (like Nvidia), but it is incredibly consistent, characteristic of a "Utility" stock.

Insight: By 2030, for every $100 Adobe collects, it keeps nearly $48 as profit. This is elite performance, well above the industry average.

Strategic Note: With FCF projected to cross $11 billion by 2027, Adobe has a "war chest" to acquire any startup that threatens it, or retire shares to boost EPS. Note: 2029-2030 FCF estimates were not available in the provided data.

Deep Dive Report

1. Executive Summary: The Thesis for the "Content Factory"

In the technology world, Artificial Intelligence (AI) is often seen as a disruptor that kills old companies. The popular fear is simple: "If a computer can generate a logo in 5 seconds, why do we need Photoshop?"

This report argues the opposite: Adobe is weaponizing AI, not dying from it. In the new "Age of AI," companies need to create thousands of personalized ads, videos, and posts every day. Humans cannot do this manually. They need a factory. Adobe is that factory.

The investment thesis rests on three pillars of durability that extend through 2030:

Commercial Safety: Big brands like Nike and Coca-Cola cannot risk using "wild" AI tools that might infringe on copyrights. Adobe Firefly is the only enterprise-grade, legally indemnified solution.

The Integration Lock-In: An AI image generator is useless if it sits on a separate website. Adobe embeds AI inside the tools professionals already use.1 You don't just "generate" an image; you edit it, layer it, and format it—all within Adobe's walls.2

Financial Durability: The FactSet consensus data provided for this report paints a picture of exceptional health. Revenue has grown consistently since the dawn of Generative AI in 2022 and is projected to reach $36.3 billion by 2030, with profit margins approaching 48%.

However, this growth is currently on sale. With a valuation heavily discounted compared to its fair value, the stock offers a "margin of safety" for investors willing to bet that creativity is not going away.

2. Business Overview: The Three Clouds

Adobe was founded in 1982, but it has reinvented itself into a cloud subscription business. It operates in three main segments.

2.1 Digital Media: The Creative Cloud (The "Studio")

This accounts for ~50% of revenue. It includes the iconic tools: Photoshop (images), Illustrator (graphics), Premiere Pro (video), and After Effects (animation).3

Why it wins: It is the "language" of design. If you want to work in Hollywood or Madison Avenue, you must speak "Adobe."

2.2 Digital Media: The Document Cloud (The "Paperwork")

This includes Acrobat and Adobe Sign.4

The Moat: The PDF is the global standard for documents. This segment is a quiet cash cow (~10% of revenue) that grows as the world goes paperless.

2.3 Digital Experience: The Marketing Cloud (The "Megaphone")

This segment (~25% of revenue) helps companies sell.

The Loop: Morningstar analysts emphasize that Adobe creates a loop: once an artist makes an ad in Creative Cloud, the marketing team uses the Experience Cloud to email it to customers, track who clicks it, and manage the online store (Magento). Adobe is the only company that connects the creation of content with the delivery of content.

3. Financial Analysis: The Growth of the AI Era (2024-2030)

The quantitative case for Adobe is based on its ability to grow steadily while printing cash. The data below covers the entire "Age of AI," from the launch of ChatGPT/Midjourney through the projected maturity of the technology in 2030.

3.1 Revenue Growth Trajectory

FactSet consensus estimates show that AI is not slowing Adobe down; it is powering a steady ascent.

Table 1: Long-Term Revenue Consensus

YearTotal Sales (Millions)YoY Growth (%)Subscription Revenue (Millions)Source2024$21,50510.8%$20,521FactSet2025E$23,69210.2%$22,823FactSet2026E$25,8899.3%$25,044FactSet2027E$28,2789.2%$27,324FactSet2028E$29,7725.3%N/AFactSet2029E$33,43512.3%N/AFactSet2030E**$36,308**8.6%N/AFactSet

Analysis: The company is effectively doubling its size during the AI transition. The growth is not explosive (like Nvidia), but it is incredibly consistent, characteristic of a "Utility" stock.

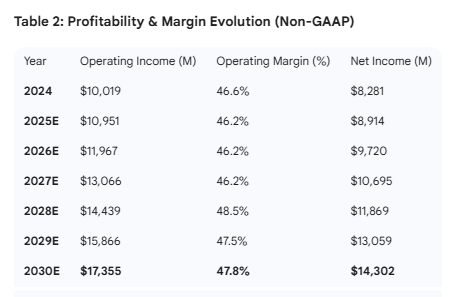

3.2 Profitability: The 48% Margin

Adobe is one of the most profitable companies on earth. It costs them almost nothing to sell one more digital subscription, so as they grow, their margins expand ("Operating Leverage").

Table 2: Profitability & Margin Evolution (Non-GAAP)

Insight: By 2030, for every $100 Adobe collects, they keep nearly $48 as profit. This is elite performance, well above the industry average.

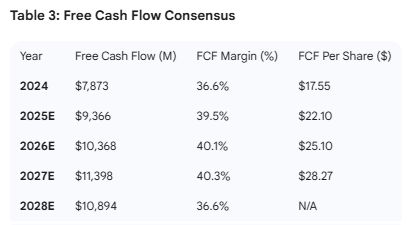

3.3 The Cash Flow Machine

Adobe does not pay a dividend.5 Instead, it generates massive "Free Cash Flow" (cash left over after bills) and uses it to buy back its own stock.6

Table 3: Free Cash Flow Consensus

Strategic Note: With FCF projected to cross $11 billion by 2027, Adobe has a "war chest" to acquire any startup that threatens it, or simply retire shares to boost EPS. Note: 2029-2030 FCF estimates were not available in the provided dataset.

4. Deep Research: The AI Pivot – From "Tool" to "Assistant"

The single most important variable for Adobe is Firefly, their Generative AI model.

4.1 The "Clean Data" Moat

Most AI models (like Stable Diffusion) were trained by scraping the open internet. This creates "copyright traps" where a user might accidentally infringe on an artist's work.

The Solution: Adobe trained Firefly only on Adobe Stock images (which they own) and public domain content.

The Guarantee: Adobe offers IP Indemnification. If a business gets sued for using a Firefly image, Adobe pays the legal bills.7 This makes Firefly the standard for corporate America.

4.2 Monetization: "Generative Credits"

Adobe has introduced a consumption model called Generative Credits.

How it works: A subscription gives you 500 "generations" a month. If you are a power user (like an ad agency making 10,000 variations), you pay extra for more credits.8

Why it matters: This allows Adobe to make more money from AI usage, even if they don't add new users. It turns the AI boom into a direct revenue stream.

5. Strategic Growth Vector: The "Content Supply Chain"

While AI creates images, the Digital Experience segment is where the money is made.

5.1 The Problem with Marketing

CMOs (Chief Marketing Officers) are drowning in content. They need to put ads on TikTok, Instagram, TV, and Websites, all personalized for different users.9

5.2 The Adobe Solution

Adobe connects the Creative Cloud (making the asset) to the Experience Cloud (managing the asset).10

GenStudio: A new product that lets marketers "self-serve." A marketer can take a Photoshop file, use AI to change the background to "Winter," and publish it to Instagram—without needing to bug a designer. This unlocks massive productivity and opens the CMO's budget to Adobe.

6. Competitive Landscape: Frenemies and Rivals

Adobe operates in a complex world where it competes with and partners with the same companies.

6.1 Adobe vs. Canva

The Threat: Canva is free, easy, and web-based. It is winning the "amateur" market (students, social media managers).

Adobe's Defense: Adobe Express. Adobe built a Canva-clone that is compatible with professional Photoshop files. This defends the low end while keeping users in the Adobe ecosystem.

6.2 Adobe vs. Midjourney / OpenAI

The Threat: AI tools that create stunning images from text.

Adobe's Defense: Workflow Integration. You can create an image in Midjourney, but you can't edit it easily (layers, text, vectors). Adobe puts the AI inside the editor. Professionals don't just want an image; they want a working file.

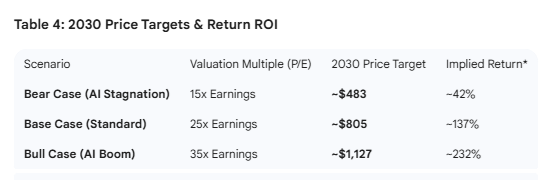

7. Valuation and Investment Scenarios

Adobe is a premium company trading at a discount.

7.1 Historical Context

Current Price: ~$339.12 (Dec 8, 2025)

Fair Value: $560.00 (Morningstar Estimate)

Discount: ~39% Undervalued

7.2 2030 Valuation Models

Using the FactSet consensus 2030 EPS estimate of $32.20, we can model potential returns.

Table 4: 2030 Price Targets & Return ROI

ScenarioValuation Multiple (P/E)2030 Price TargetImplied Return*Bear Case (AI Stagnation)15x Earnings~$483~42%Base Case (Standard)25x Earnings~$805~137%Bull Case (AI Boom)35x Earnings~$1,127~232%

*Note: Returns calculated from a $339 entry price.

Investment Implication: Even in the "Bear Case" where Adobe is valued like a slow-growth utility company (15x), investors still make a profit. In the "Base Case," the stock price more than doubles.

8. Risk Analysis: What Could Break the Thesis?

8.1 "Seat Compression" (Deflation)

This is the structural risk of the AI era.

Mechanism: If AI makes designers 5x more productive, companies might fire designers to save money.

Impact: Adobe charges "per seat" (per person). Fewer designers = fewer subscriptions. Adobe must succeed in selling Generative Credits (usage) to make up for lost seats.

8.2 The "Good Enough" Problem

For 90% of people, a free AI image from ChatGPT is "good enough." They don't need the power of Photoshop. If the world settles for "good enough," Adobe loses its pricing power.

9. Conclusion: The Long-Term View

Adobe is a rare combination of safety and growth. It has successfully navigated the transition to the cloud, and now it is navigating the transition to AI. By building the "Safe AI" for business and integrating it into the tools professionals already use, Adobe has built a defensive wall around its empire.11

The financial data support a bullish view: a company doubling its revenue during the "Age of AI" while maintaining elite profit margins. At a 39% discount to fair value, Adobe represents a compelling opportunity for investors who believe that the future will require more digital content, not less.

Final Recommendation: For investors with a 5+ year horizon, Adobe is a core holding. It is the "pick and shovel" play for the creative economy—the indispensable platform that powers the visual world.