Today, it’s drinking from a firehose on news, and since I have to publish this at 4 PM EST (more appointments!), let’s get straight to it!

Update on GNG Progress: Portfolio Tracking

Glenn Ford (GB Medici) will be joining GNG Research soon (he helped build the NIH PubMed system, so we’re so excited to have him join the team! 3 guys and some algos…and only 1 of whom CAN’T Code😉) but for the next week or two it’s still just me and Connor and as you can imagine, there are a lot of bugs to be worked out to get portfolio tracking done right.

It was the most requested feature for Dividend Kings, but the SA tech stack didn’t permit it.

Connor will be providing an updated article in the next 2 days, but for now, I can tell you that we’re planning on releasing model portfolio tracking next Wednesday, Nov 12th.

What we can provide today is live trade data on ZEUS for anyone who wants to follow along.

At the moment, everyone’s email notifications are on, so unless I hit a special button, every time I update, it sends an email to everyone.

We’ll change it so that you opt in to email notifications on any model portfolio to avoid this.

We’re working very hard to make sure that everything not only accurately tracks in terms of profits, dividends, and values (intra-day values coming on Nov 9th) but also the portfolios valuations.

Preliminary Portfolio Tracking (Still In Alpha, Coming Nov 12th)

A Lot More Features To Come But Baby Steps😉

Earnings You Have To See To Believe!

Usually, 75% of companies beat earnings expectations (10-year average) because analysts reduce estimates going into earnings. In other words, the bar is lowered, so that companies can easlily step over it.

But this is the first time in years that analysts, tired of being sandbagged by guidance, didn’t cut guidance. estimates.

Last quarter, analysts started the quarter expecting 3% growth, and thanks to big tech, we got 13%.

This quarter, 7% growth was expected, and we’re at 13.8% with Nvidia on tap later to push us over 14% (NVDA’s biggest customers just all announced more spending).

The market continues to underestimate the scale of the opportunity, and Nvidia remains one of the best ways to play the AI theme."

After a string of recent announcements solidified its dominance in the AI race, shares of the Santa Clara, California-based company ended Wednesday's session up 3% at $207.04, giving it a stock market value of $5.03 trillion.

Huang announced $500 billion in AI chip orders on Tuesday and said he plans to build seven supercomputers for the U.S. government.

Nvidia now has $450 billion in orders for 2026, a year when the consensus is for $281 billion in sales, up from $201 billion.

In other words, if Nvidia can get the supply, it can generate over 100% sales growth in 2026. The orders are there, the demand is there.

They are supply-constrained by Taiwan Semi (chip wafers) and SKHynix (memory chips).

The AI boom that keeps getting bigger?

Like how Microsoft did $35 billion in capex this past quarter? Up 75% YOY? And still grew free cash flow 34%? YOY?

This is from Morgan Stanley, Citigroup, IDC, and Nvidia

These are the latest consensus estimates for growth spending from the five hyper scalers (Open AI going public will unlock even more estimates, Anthropic too).

Cumulative growth spending (R&D + capex) is up from $5.5 trillion from 2023 through 2030 to $6 trillion, and now total growth spending is expected to grow 21% CAGR through 2030…while free cash flow growth is up from 18% CAGR to 22%.

On a per share basis (due to 1% to 2% net buybacks), that’s 23% to 24% CAGR FCF/share consensus on the hyper scalers.

FCF margins are expected to rise 4% CAGR to 19% by 2030…despite $6 trillion in growth spending.

$16.3 trillion in revenue over 8 years from just five companies…that is the scale we’re talking about.

$2.043 trillion per year from just 5 companies.

If Hyper scalers Were There Own Country They Would Have The 11th Largest GDP In The World (Ahead of Russia)

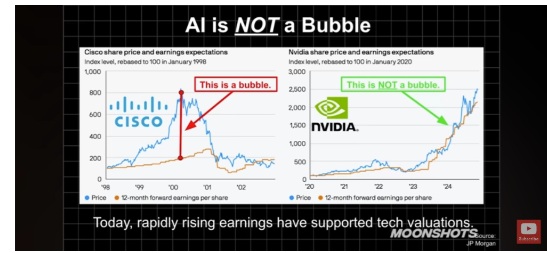

Despite the huge numbers and hyperbolic headlines, spending remains mostly cash flow based. You can always find examples of mania but as a whole this is not an AI bubble yet.

Welcome To The Age Of AI: Where Completely True Facts Sound Batshit Crazy😂😉

The numbers keep getting bigger, just like the greatest CEOs in history, who have almost $600 billion in free cash flow, say it will. They say, “we’re supply constrained, so we spend more on growth,” and then they do, crush earnings, and people are still baffled by rising stock prices?

No matter how high stock prices go…that doesn’t make it a bubble; what makes it a bubble is if fundamentals don’t keep up.

If Jensen’s $450 billion potential sales guidance is accurate, then NVDA is potentially trading at a forward PE of 14.6.

Yes, there are plenty of funny memes out there. I’m one of the people making them. 😉

This is for You, Michael Batnick 😂

But the sales are real, the profits are real.

All the hyper scalers are supply-constrained. As soon as new capacity is available, it sells out immediately. So yes, the sales are showing up, and the free cash flow is expected to grow.

Last Night, after hours, 5% crash rule filled on Nvidia

It’s Not Just Big Tech Earnings That Are Growing

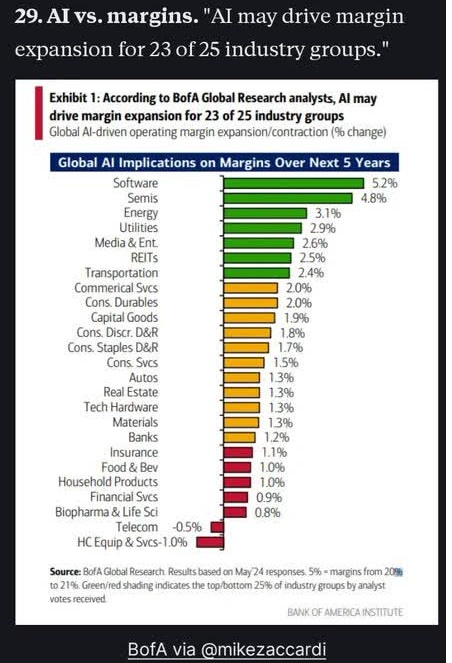

Margins are expanding in 7 out of 11 sectors, and Bank of America expects AI will keep driving that.

And wait, it gets better! The earnings growth…it’s showing up!

“Where is the proof this is profitable?” RIGHT HERE!

This isn’t forecasts, it’s real. This is trailing earnings growth, which is now accelerating into double digits! The earnings recession that occurred for most of the stock market during the best economy in 30 years? It’s over! Bubble? Late cycle? Earnings growth is just starting for the median US company, and it’s due to AI.

If sales grow faster than costs, margins go up.

60% of business costs are labor.

If revenue grows faster than wages? Then margins go up.

Growth accelerates.

S&P PEGY Update

Last week, the 3-year FCF/share growth consensus was 14.0% and its down a bit to 13.1% now.

Potentially a sign of higher capex estimates in 2027 (due to the AI spending boom)

This Might Be Why 3-year FCF/Share Growth Dipped The Past Week

Of course, what matters is that the broader market’s 1.09 PEGY is far from a bubble and in fact, means that if stocks were to rise 10.7% by year's end, it would be a PEGY of 1.21, the 10-year median.

Currently, 12.1% growth is priced in vs the 13.8% growth we’ve just had, and 13.4% is currently expected over the next 12 months. If the growth keeps up at today’s levels? Then this isn’t a bubble; fundamentals justify it.

Economic Update: Growth Might Be Accelerating!

The analyst consensus has been rising to catch up to the strong economic data.

This is what I was predicting because economists are not comfortable saying 4% growth, in case the economy rolls over and they lose their jobs.

If you predict 4% and its 1% you can get fired.

If you predict 1% and its 4% everyone is so happy they don’t care that economists had predicted nine consecutive months of slowing growth, and only the real-time Fed models were correctly saying that was incorrect.

That big grey line that is rising steadily by the week? That’s business investment…ie, AI growth spending.

The numbers keep rising, and new announcements seem to come every day.

Of course, Anthropic is trying to raise money at $350 billion (vs $174 billion today), so they are going to be optimistic, but free cash flow profitable in 2028 (and by a healthy amount) could be a game-changer for frontier labs.

7 million work seats from 1 million enterprise clients, with work seats up 40% in 2 months.

No matter what you might have heard in headlines, the AI boom is real, these are real accounts, real revenues, and growth rates are accelerating.

Of course, Sam Altman is CEO of a private company, so he could be lying about hitting $100 billion in sales by 2027 (previous forecast $90 billion in 2028), BUT so far the news seems to be at least making these claims reasonable.

And the good news is that the retail sales easing we’ve seen in recent weeks (likely government shutdown related) have reversed (at least this week).

Once the government reopens, the only significant recession risk goes away.

Congressional Budget Office estimates a 2 month shutdown takes 2% off GDP.

Tariffs (per Yale’s Budget Lab) max impact -1.1% by May 2026.

What is the risk of a shutdown lasting until the end of the year (-3% to GDP)? The only realistic way I can imagine the US a recession in the foreseeable future?

A 5% risk of a shutdown lasting until the end of the year and causing a recession.

What about tariffs? Some good news (potentially) on that front.

If the Supreme court overturns the tariffs, then not only would they go away, but the US government would have to potentially return the money, so the negative earnings headwind (which AI has helped the S&P overcome with 14% growth this quarter) would get a $130 to $140 billion estimated boost in profits.

In other words, we MIGHT be on the verge of pure stimulus for the economy, which might already be growing at 4%.

Yale Budget lab estimates that tariffs will be weighing on growth by 1.1% by May.

Without them, GDP growth could be 3.6% to 5.1% (plus 0.6% stimulus boost next year) = 4.2% to 5.7% GDP growth vs 3.5% 1990s average.

Novo Nordisk Earnings & Human Earnings: Preliminary Takes Coming Tomorrow

Novo and Humana had 2 more limits filled due to earnings that disappointed.

Novo has reduced guidance for the 4th time but rather than rush an analysis I’ll save that for tomorrow so I can do some member PEGY analysis.

ZEUS Real Time Update

Global Payments (GPN) PEGY Analysis

GPN has been badly beaten down as you can see, allowing us to buy aggressively at PE ratios that haven’t’ been seen in decades.

As you can see GPN is currently trading at the lowest PE in 20 years (at least).

GPN IPOd in 2001 and this is the worst bear market in its history.

Earnings were solid but of course the WorldPay acquisition and its high execution risk is the reason the stock is trading at a PE under 6 vs a historical 20X.

Non-Growth Adjusted Return Potential

You can see why GPN is one of my 3 deep value stocks in ZEUS 2026, because the return potential if it can return to historical growth rates, is extraordinary.

A 4X in 2 years…or at least that’s what historical valuation SEEMs to show.

So let’s double-check that the PEGY thesis is holding after earnings.

Worldpay Debt Explains Why The Discount Is 45% And Now 66%

The power of PEGY is that the debt GPN is taking on to acquire Worldpay, which is $7.7 billion including taking on Worldpay’s debt, means that while the PE is 3X lower than its historical norm, the EV/FCF is just 45% lower.

And that means that as the debt is paid off over time, the EV/FCF will also recover and you can see how the return potential is still impressive.

Remember that paying down debt increases intrinsic value because it reduces interest costs AND also minimizes the risk of default.

The deal is expected to close within Q1 of 2026 when UK regulators clear the deal.

Member FAST Graphs Request