In part 1 of this special report series, I explained why Tobacco stocks have historically been attractive and what high-yield investors need to know about the future of the nicotine industry.

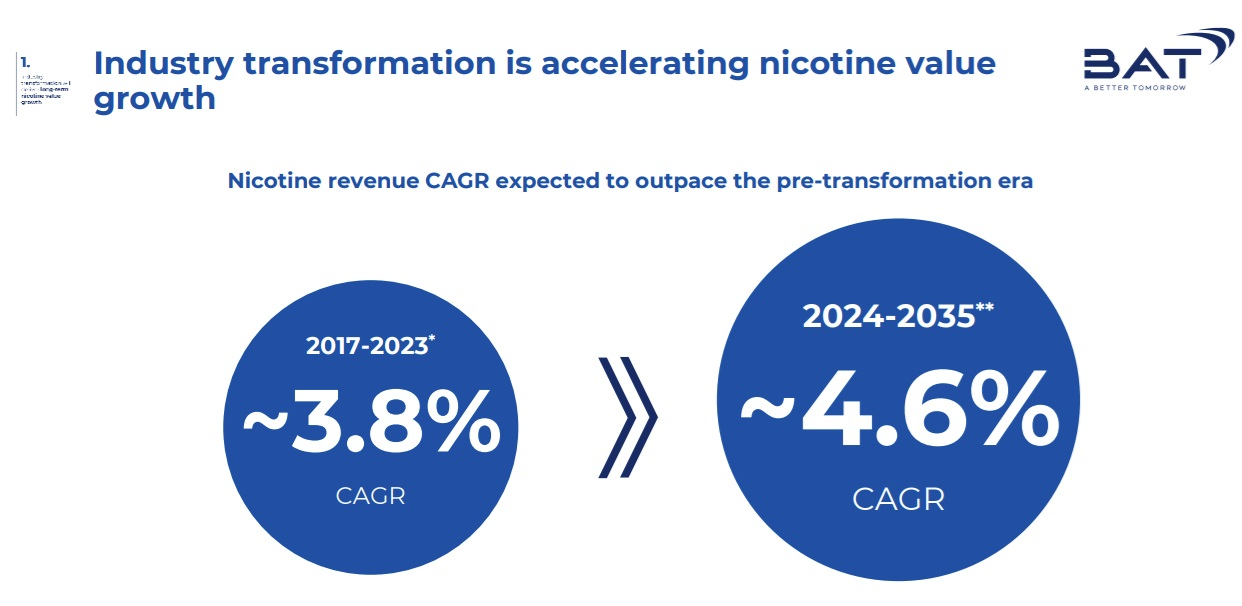

The nicotine industry is actually growing faster, thanks to the rise of reduced-risk products like vaping, heat sticks, and oral nicotine pouches.

And thanks to iQOS, the first popular heat stick brand, Philip Morris International (PM) has become the growth leader among tobacco dividend aristocrats.

So let’s take a closer look at Philip Morris International, from the perspective of the PEGY ratio and valuation analysis, to see whether the global leader in reduced risk nicotine is a potentially attractive buy today, and whether or not it’s a potentially attractive addition to the Ultra ZEUS portfolio for 2026.

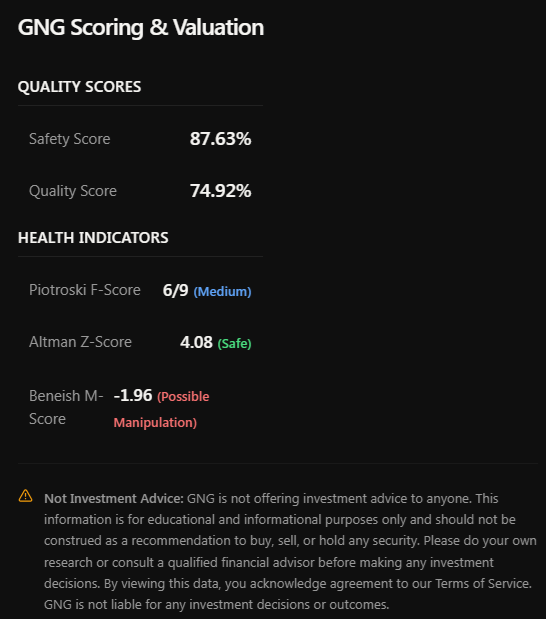

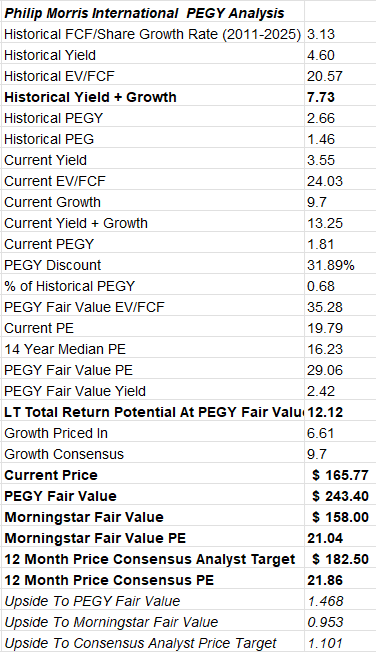

Philip Morris GNG Summary

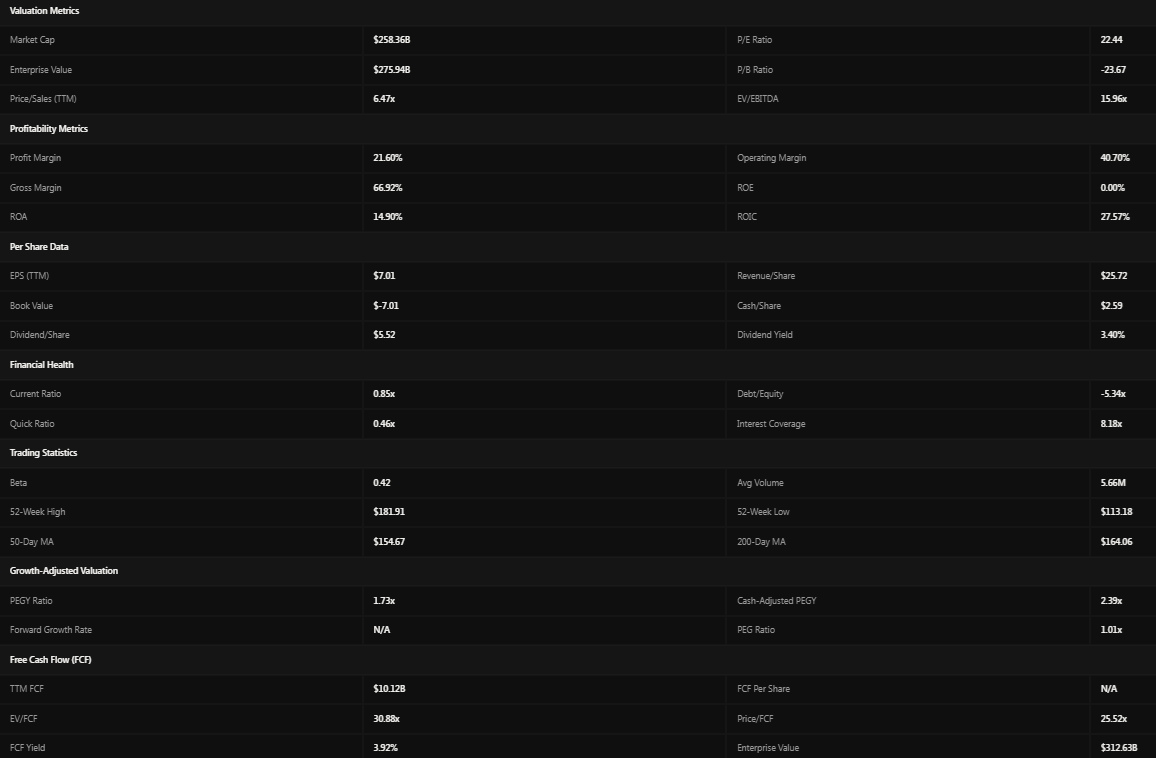

Philip Morris Valuation Analysis

There are two schools of thought when it comes to investing in companies. The first, is the classic deep value approach made famous by Ben Graham, Buffett (early in his career), and Joel Greenblatt.

And then there’s the Peter Lynch and Buffett (after he met Charlie Munger) approach of buying wonderful companies at fair prices.

So let’s take a quick look at how PM is looking from the traditional PE perspective.

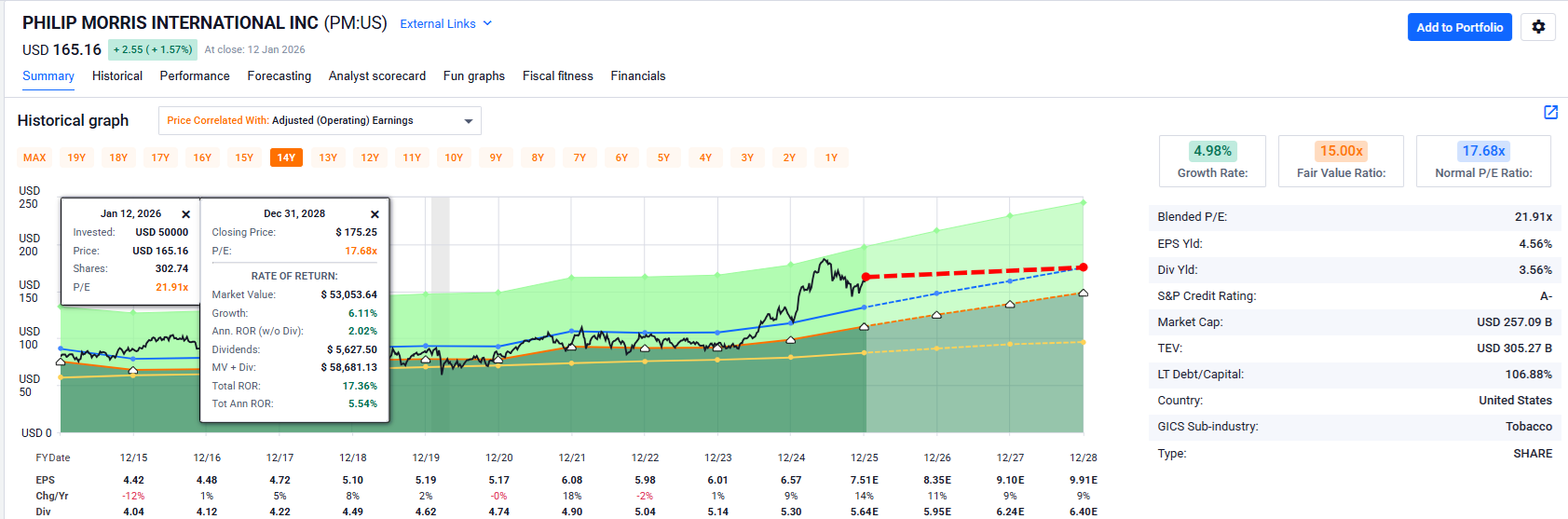

If you just look at PM over the last decade, the 5% growth company traded at an average market-determined fair value of 17 to 18, and today appears fairly overvalued, with just 17% total return potential over the next three years, despite industry-leading growth.

But valuation is both art and science, so let’s consider the PEGY ratio and what that says.

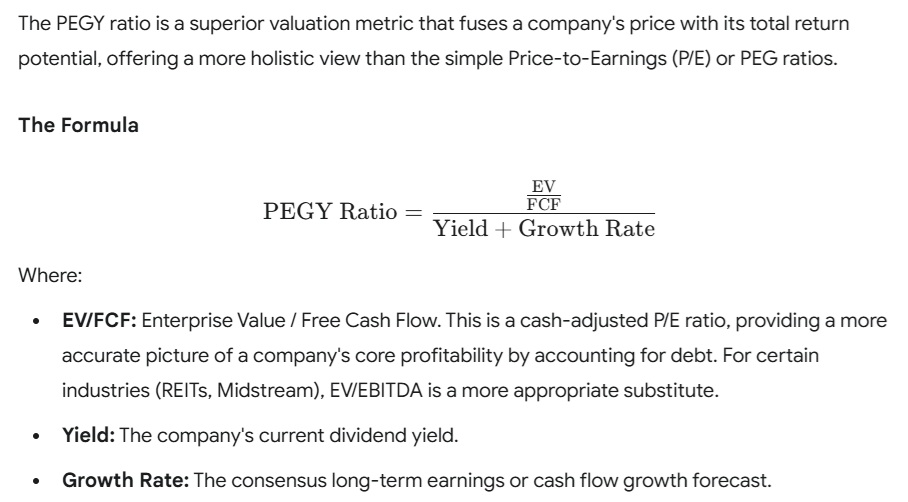

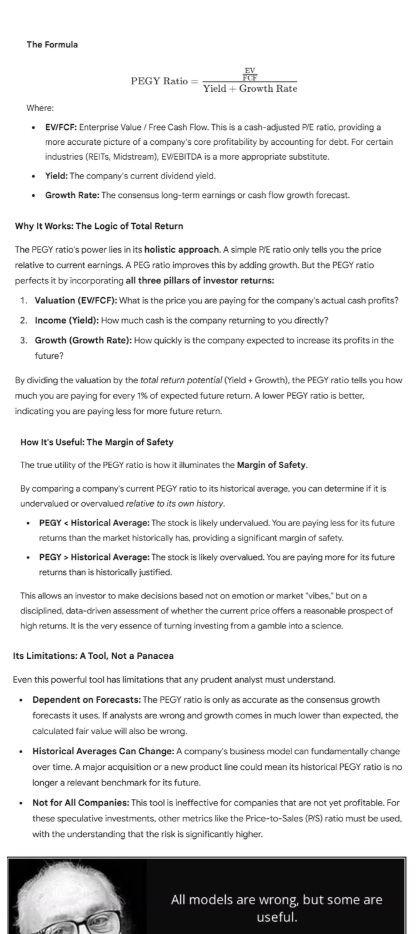

A Brief Review Of The PEGY Ratio

I believe BM Cashflow Detective (a DK member) came up with the original idea for combining the popular PEG ratio (which was invented in the 1960s but popularized by Peter Lynch in 1989) with yield. That way you’re getting the PE multiple per unit of expected future total return.

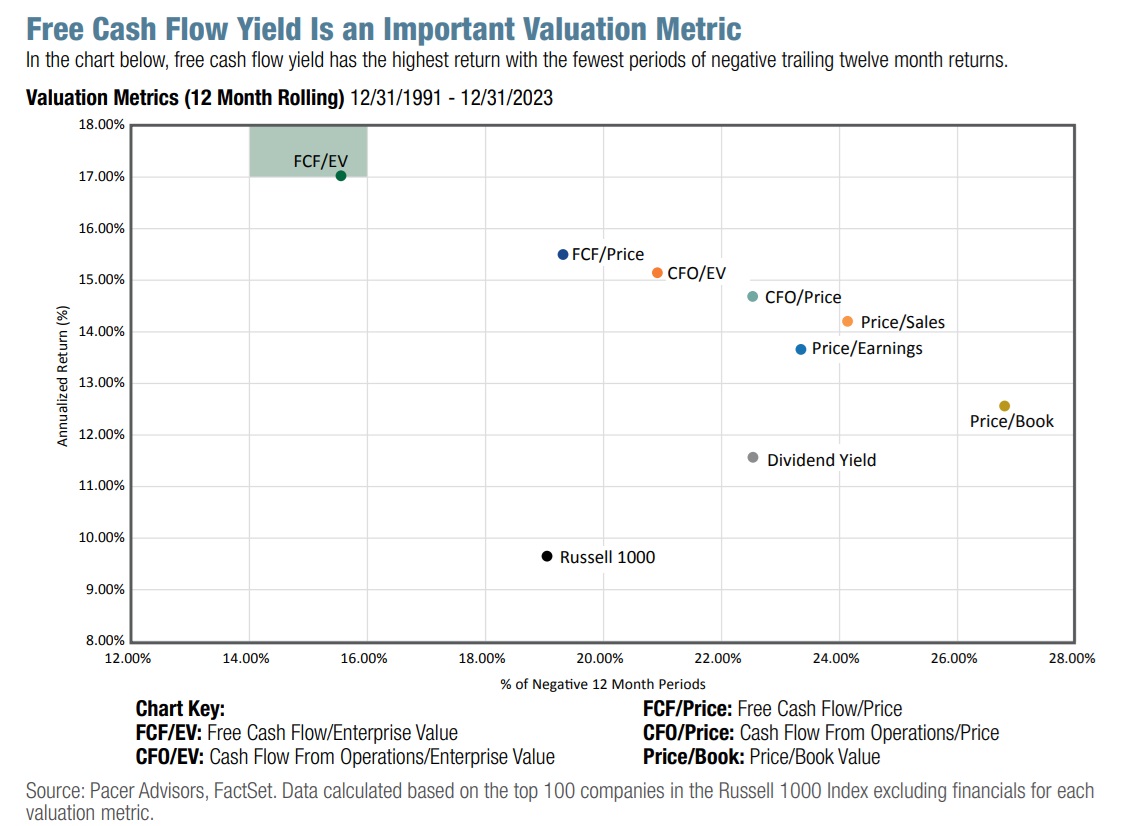

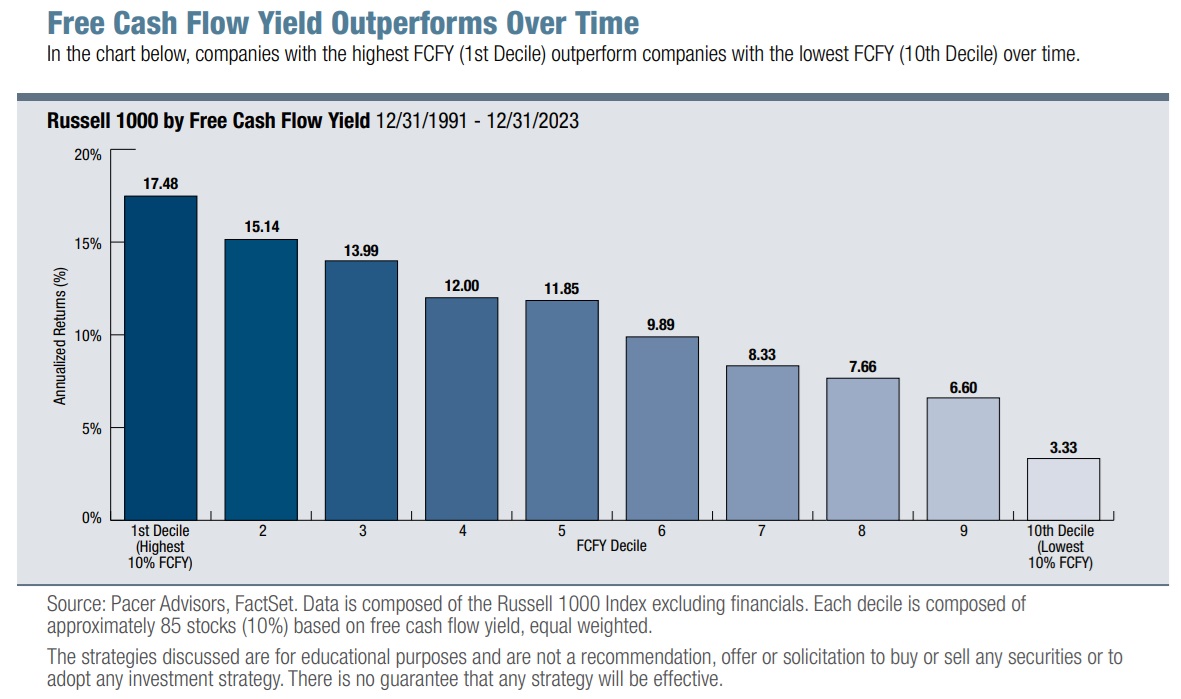

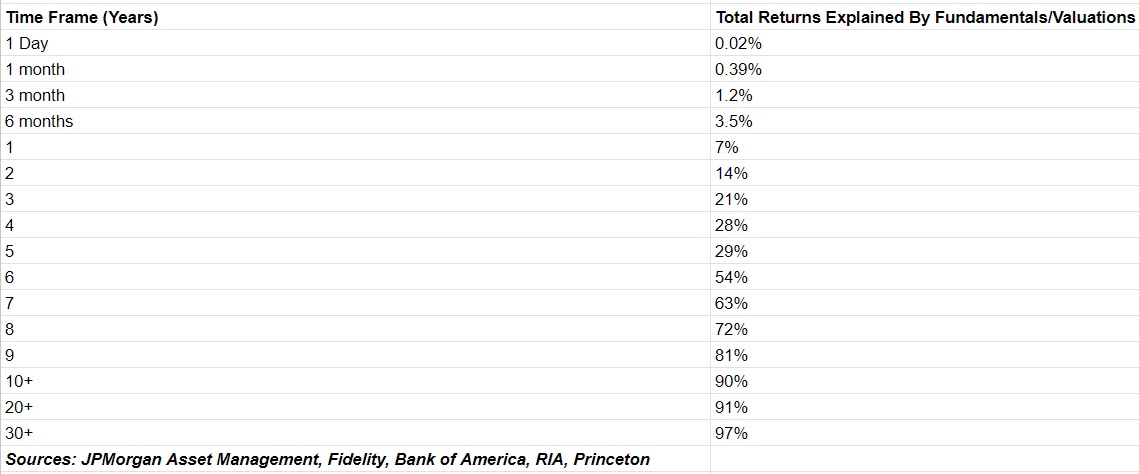

What I did was replace the PE with EV/FCF which the last 35 years of data indicate is the most accurate valuation metric.

Since 1991, using EV/FCF as your valuation metric would have resulted in not just superior returns, but also lower volatility.

Value Stocks Never Stopped Working IF You Were Measuring Valuation Correctly

By combining the approach of Lynch, Greenblatt, and Buffett, we’re trying to create the best valuation metric yet.

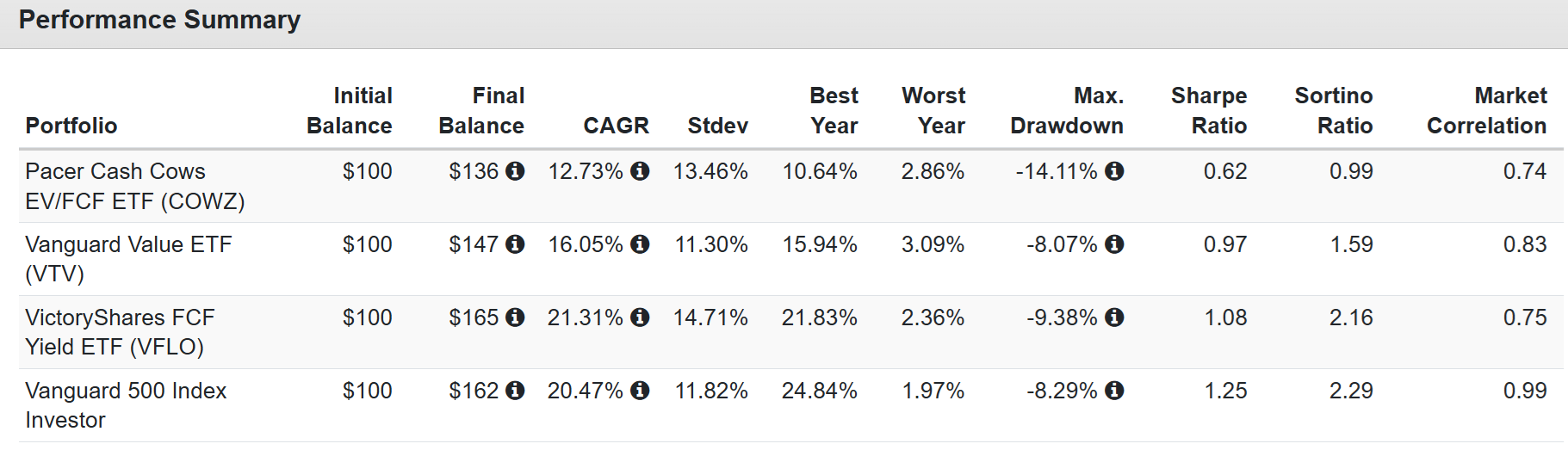

We’re working on an advanced kind of “walk forward” backtest (like what Pacer Funds and Victoryshares did) to confirm that the PEGY ratio is superior to EV/FCF and PE vs historical PE valuation methodology.

We’ll offer valuations for several metrics so that members can have the best available data and make their own minds up about whether or not a stock has sufficient margin of safety for their needs.

If we’re right that PEGY is better than PE and EV/FCF, then we’ll create an ETF based on it (that includes optimal safety measures and rules to ensure we minimize the edge-case errors that have hurt COWZ in recent years).

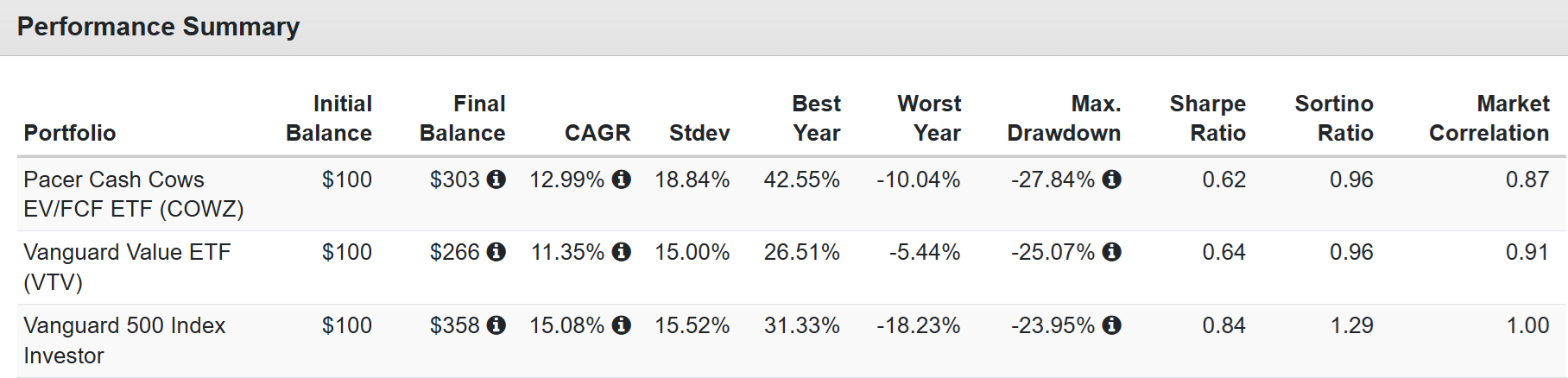

Since July 2023

VFLO uses a similar strategy as COWZ BUT also adjusts for growth, and you can see the results are significant.

How do we know that EV/FCF hasn’t stopped working?

Since January 2017

Based on the last 8 years of real-life market data, where COWZ has significantly beaten traditional value stocks, I have 81% statistical confidence that EV/FCF remains superior to traditional valuation metrics.

And in case you think 1.65% annual outperformance isn’t meaningful.

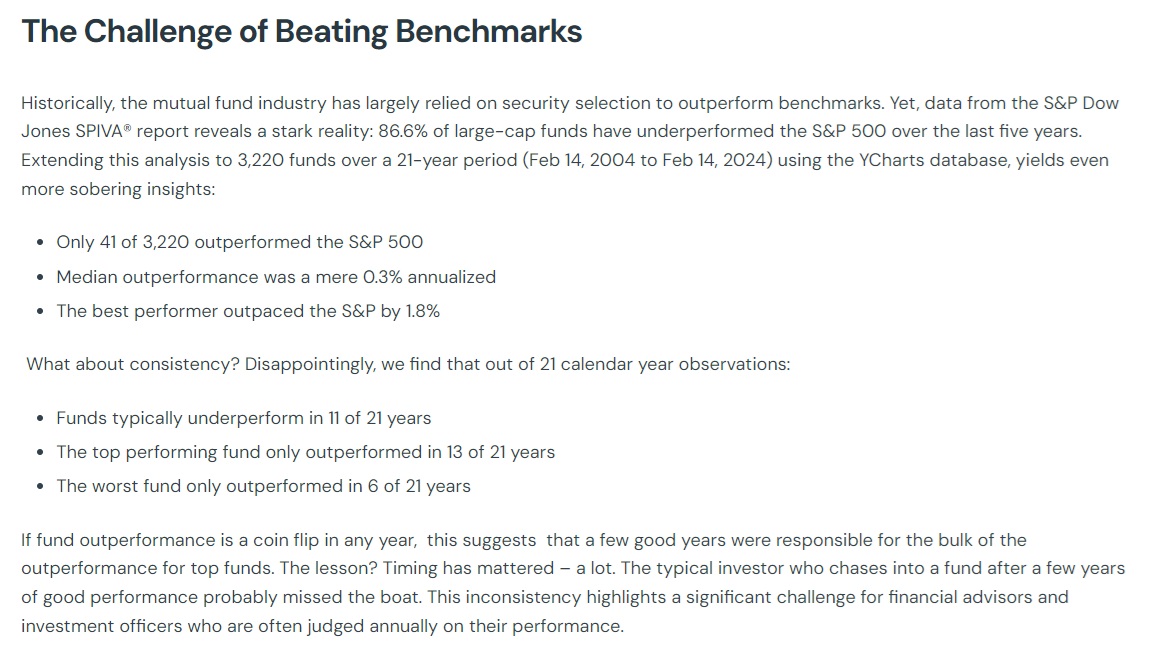

Outperforming any benchmark (like VTV) is very challenging for active managers to do.

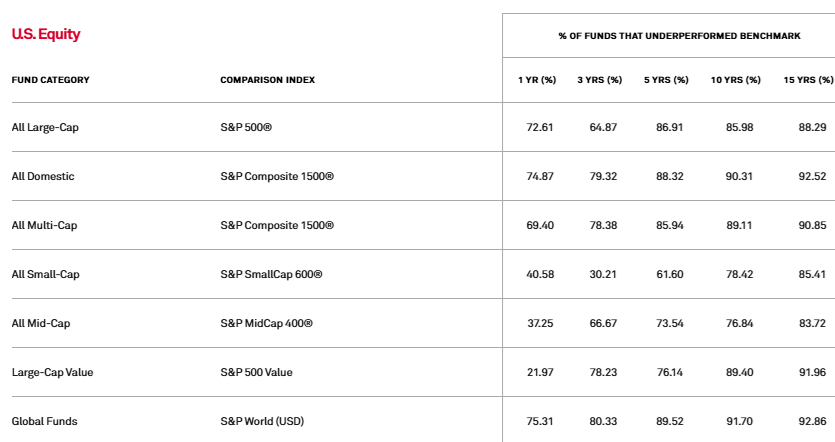

No matter how specialized the fund, 85% to 95% of fund managers can’t even keep up with their benchmarks over the long-term, and as you just saw, the 22 fund managers that beat the S&P for decades, the best one did so by just 1.8% per year.

So beating the value benchmark by 1.65% is on par with the best value manager in America…but in a 100% rules based ETF that’s based on EV/FCF with no other adjustments.

So now here’s PM’s PEGY Analysis.

PM PEGY Analysis

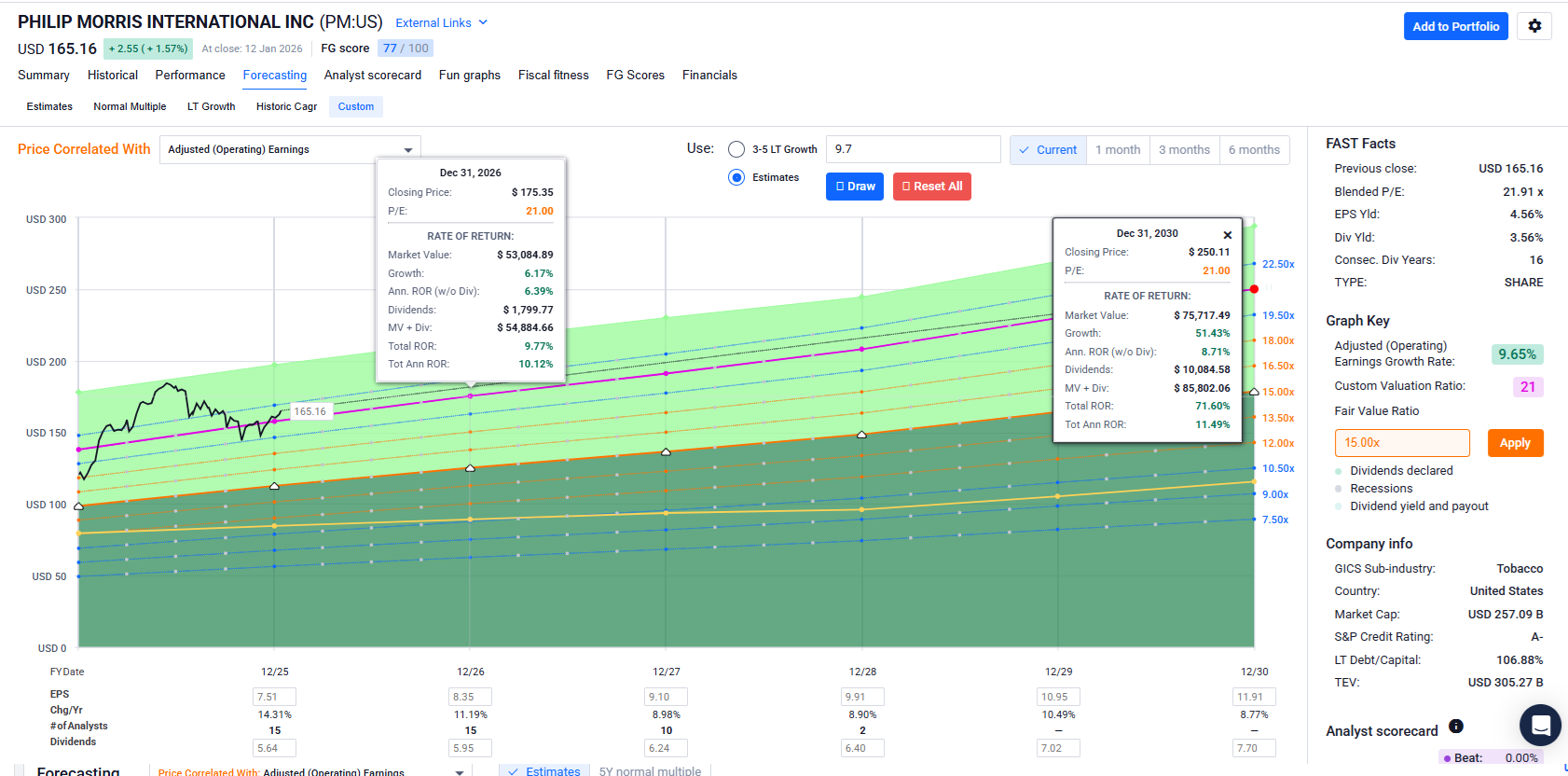

For the past 14 years, PM has had a very modest 3% growth due to its heavy investments in iQOS, but finally those are starting to pay off with almost 10% FCF/share growth expected through 2030.

Like most consumer staples companies, EV/FCF has historically been around 20X.

The reason that consumer staples like KO and DEO (alcohol) have historically traded around 20X to 25X earnings is that their EV/FCF metrics (which factor in debt) are pretty stable.

The same is true for utilities.

And midstreams.

And REITS.

In other words, PE ratios (which don’t include debt) are hiding the fact that most stable, recurring cash flow blue-chip businesses trade around 20X to 25X EV/FCF (or EBITDA for midstreams, REITs, and utilities).

In other words, PM’s historical valuation has indicated investors were willing to sacrifice total returns in the short-term (7% to 8% expected returns) in exchange for achieving the industry lead in heat sticks (the #1 growth driver of the nicotine industry).

The $16 billion acquisition of Swedish Match gave it Zynn, the #1 brand in oral nicotine pouches, and a foothold in the US (in 2018, it tried to buy Altria, but the deal collapsed due to the Juul/vapocalypse uncertainty at the time).

PM’s spin-off from Altria meant that it was a global company other than in the US, and thanks to buying out the US rights from Altria, PM now has the ability to (or soon will) be selling all its RRPs in the US.

That gives it the best of all worlds in terms of de-risking itself from a regulatory and product perspective.

With the yield + growth outlook at 13.25%, which is about 2X its historical norms, on a PEGY basis, PM is actually undervalued, by about 31%, which would make it a potentially strong buy because at its PEGY fair value of $243 and a 2.43% yield it would offer 12% to 13% CAGR long-term return potential.

However, understandably, many investors might not feel comfortable paying 29X earnings for PM, which historically trades at 16X to 18X.

Note that Costco grows at 10% too and historically trades at 35X earnings, not apples to apple,s but an example of how 29X earnings for 10% growth that’s super stable is not outrageous.

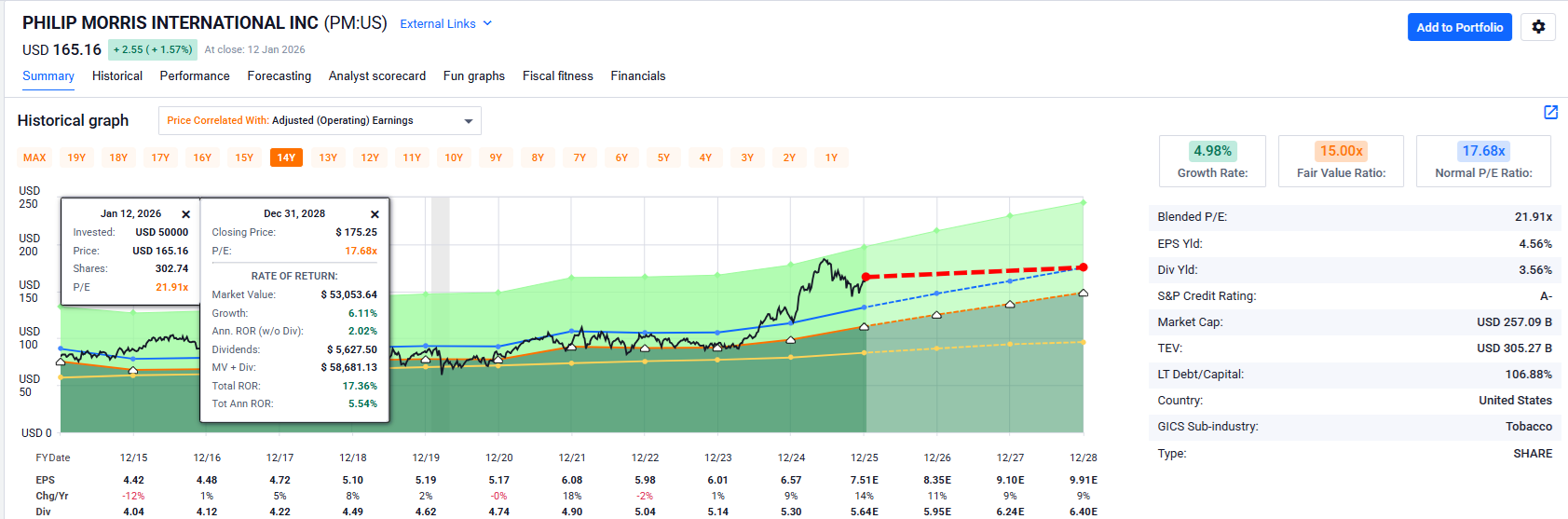

FAST Graphs: Let’s Take A Look At PEGY, Morningstar, and Analyst Fair Value

First, here’s the normal historical 10-year average PE return potential.

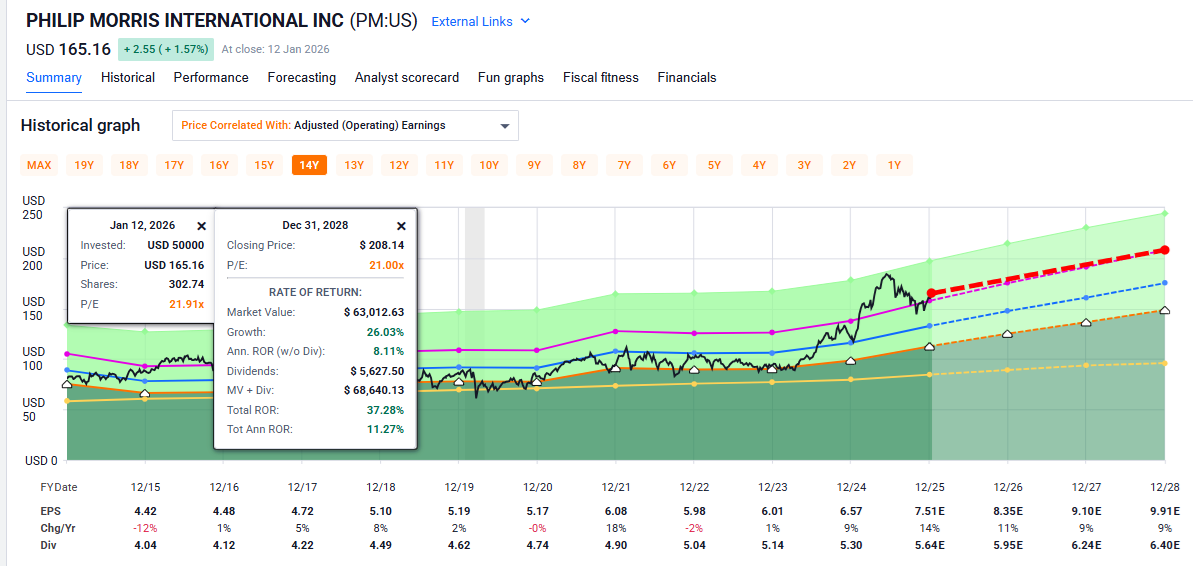

This 24% historical premium would make PM a hold, but take a look at what the fair value PE might actually be, according to analyst consensus, Morningstar’s DCF analysis (which factors in growth), and the PEGY analysis.

Morningstar Fair Value: 21X PE, Analyst Consensus 21.9X

Morningstar believes that PM’s new normal fair value PE based on its faster growth rate is a reasonable 21X, which equals a 24X EV/FCF (PEGY says 35X).

I consider this a pretty reasonable conclusion given that the growth rate has doubled and the PEGY at today’s level would be 2.4 vs a historical 2.66.

A 10% PEGY discount at Morningstar’s fair value estimate.

Morningstar/Analyst Consensus Fair Value: 21-22X PE 5 Year Outlook

So, a solid 11% to 12% CAGR total return potential for the next 1 to 5 years for PM, the highest credit rating nicotine dividend aristocrat.

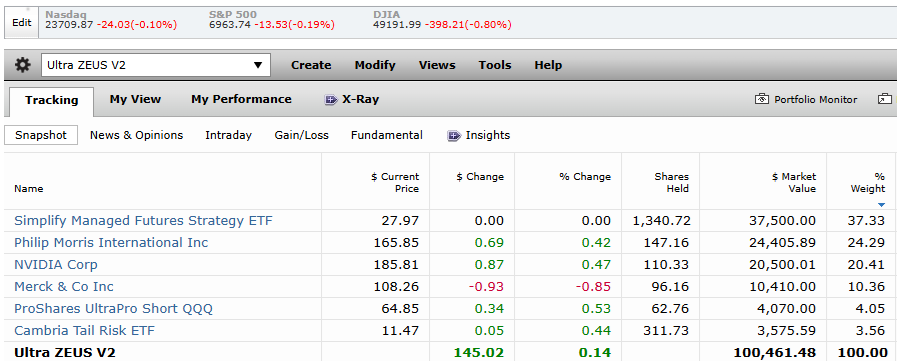

Is Ultra ZEUS Buying PM?

So most likely, Philip Morris is a reasonable buy (even if our official rating is “hold”) but the question is “Should I actually buy it?”

That’s up to you to decide based on your specific goals and whether you believe PM can make your portfolio better for your specific goals.

So let’s use the Ultra ZEUS portfolio as an example of such an analysis.

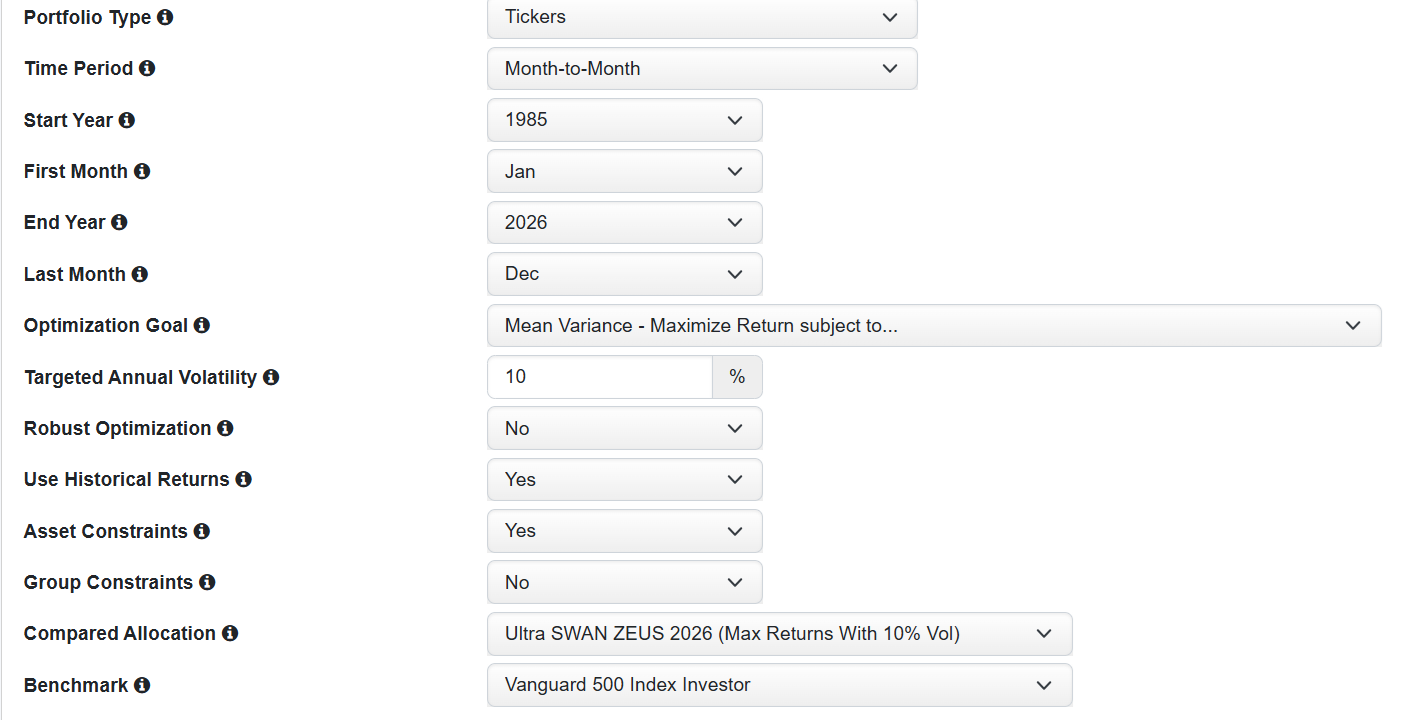

So that’s the settings I’m using, and please remember that Ultra ZEUS 2026 is a one-year portfolio with very specific goals.

Thus, the 87-page report outlining how it was created.

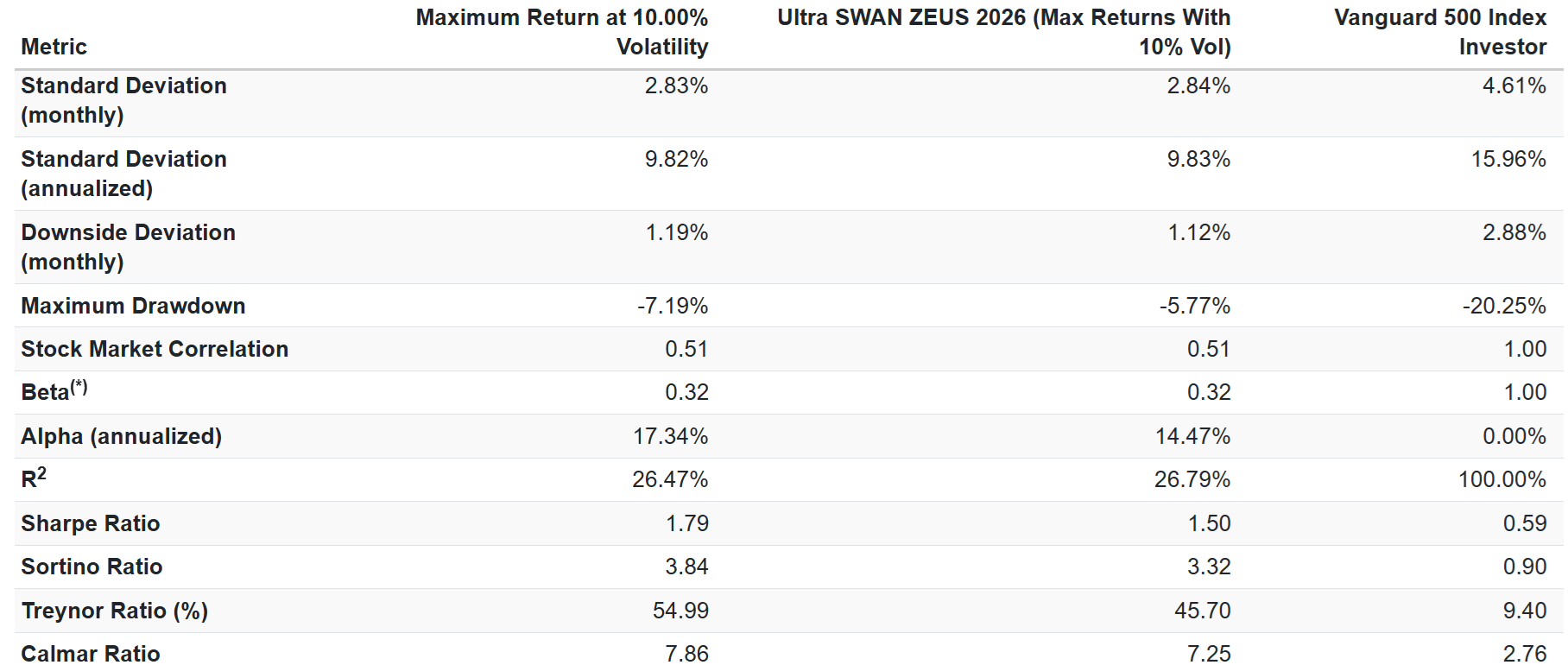

Optimized Using Historical Data Through July 2023

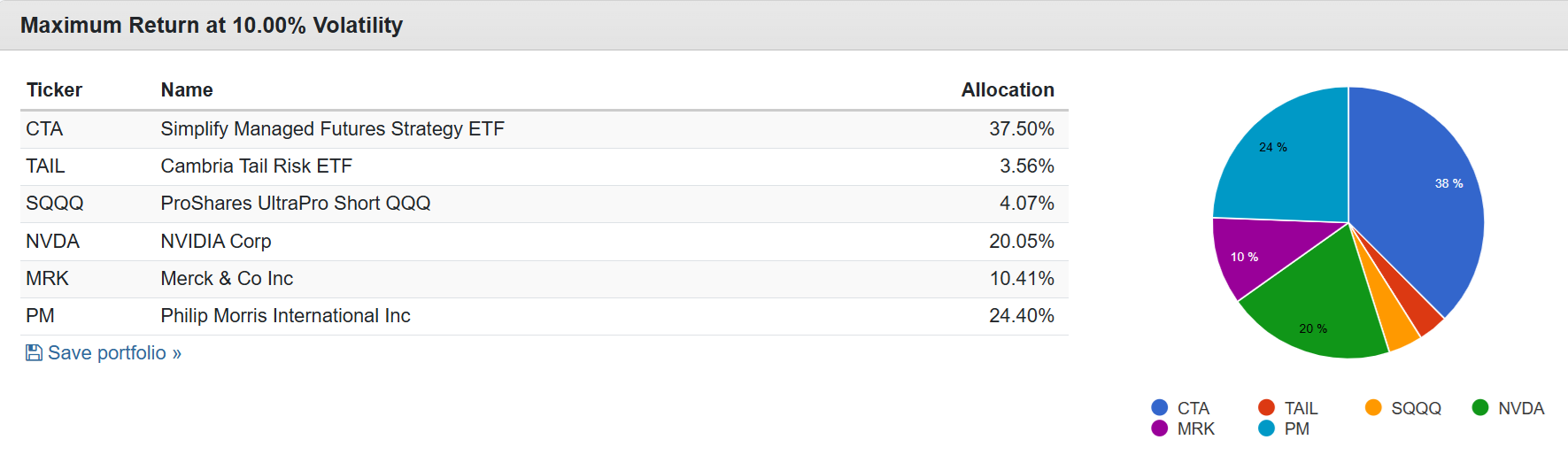

So I ran the optimizer with VFLO included to see what % of stock ETFs might make Ultra ZEUS better, and this is the result.

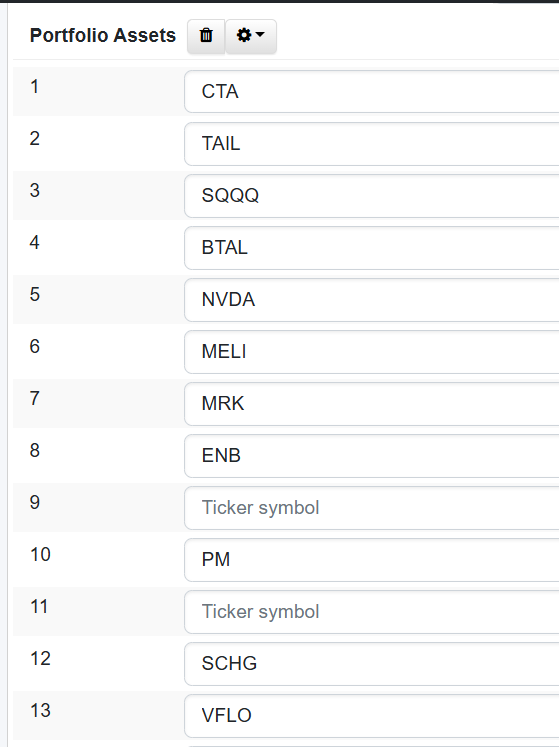

Replace some CTA and all negative-convexity hedges with a very large allocation to PM.

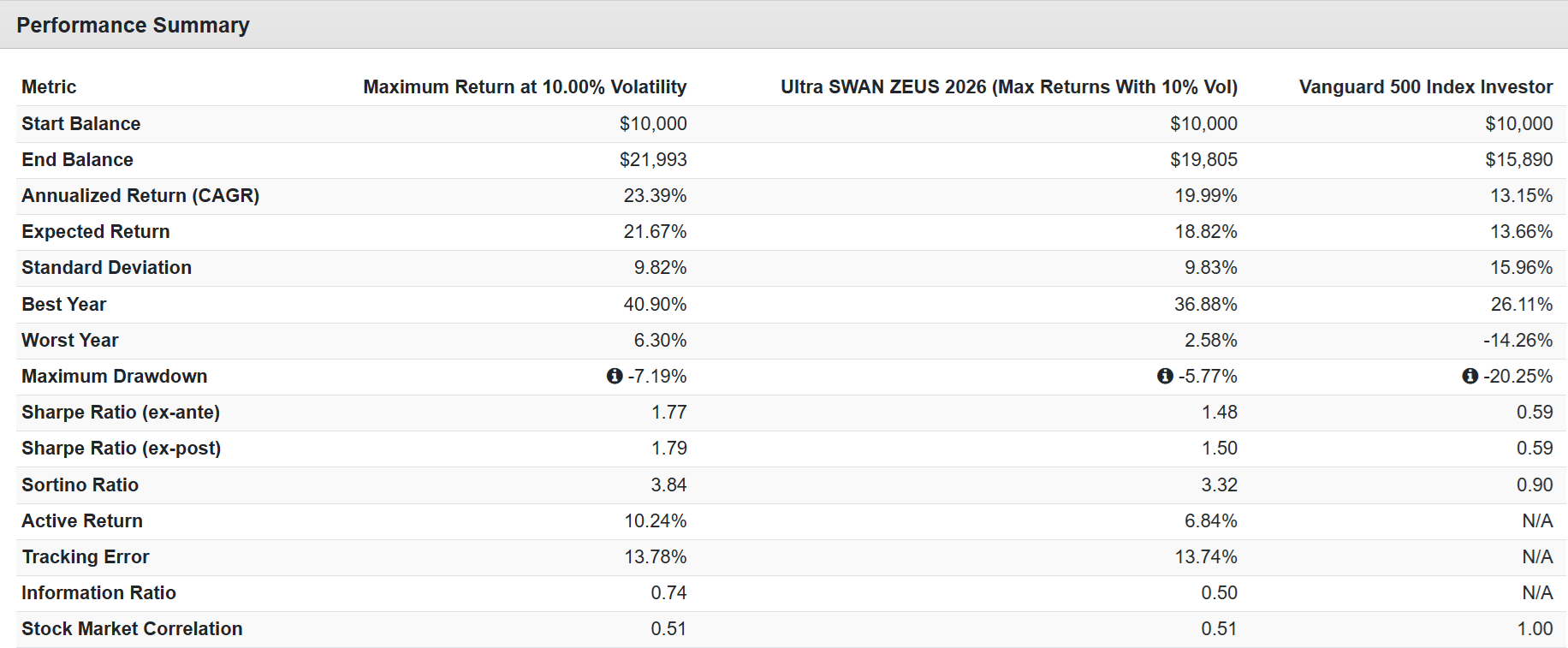

The overall returns were much stronger (because negative convexity hedges were replaced with growth stocks), but take a look at the actual volatility.

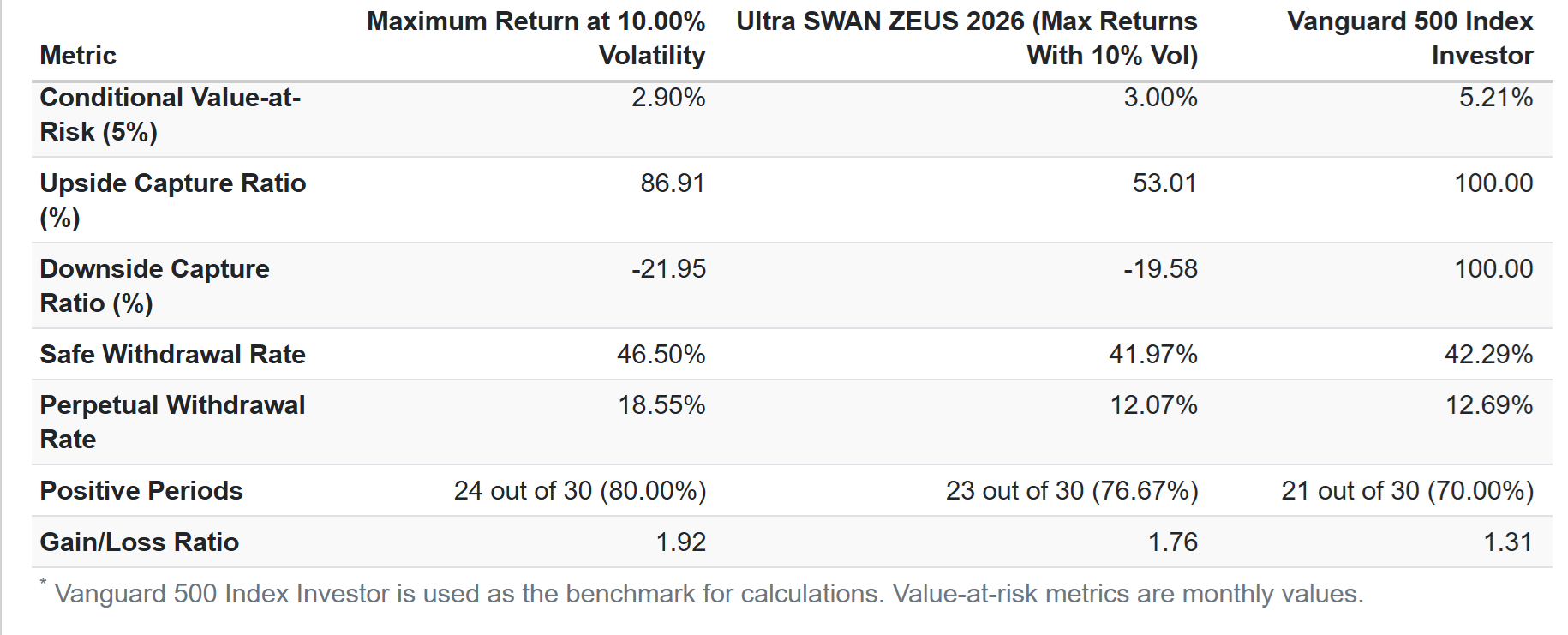

In any other year than 2026, a 0.51 beta portfolio is exactly what we’d be after, and this simpler (and more profitable) version of ZEUS is what I’d use.

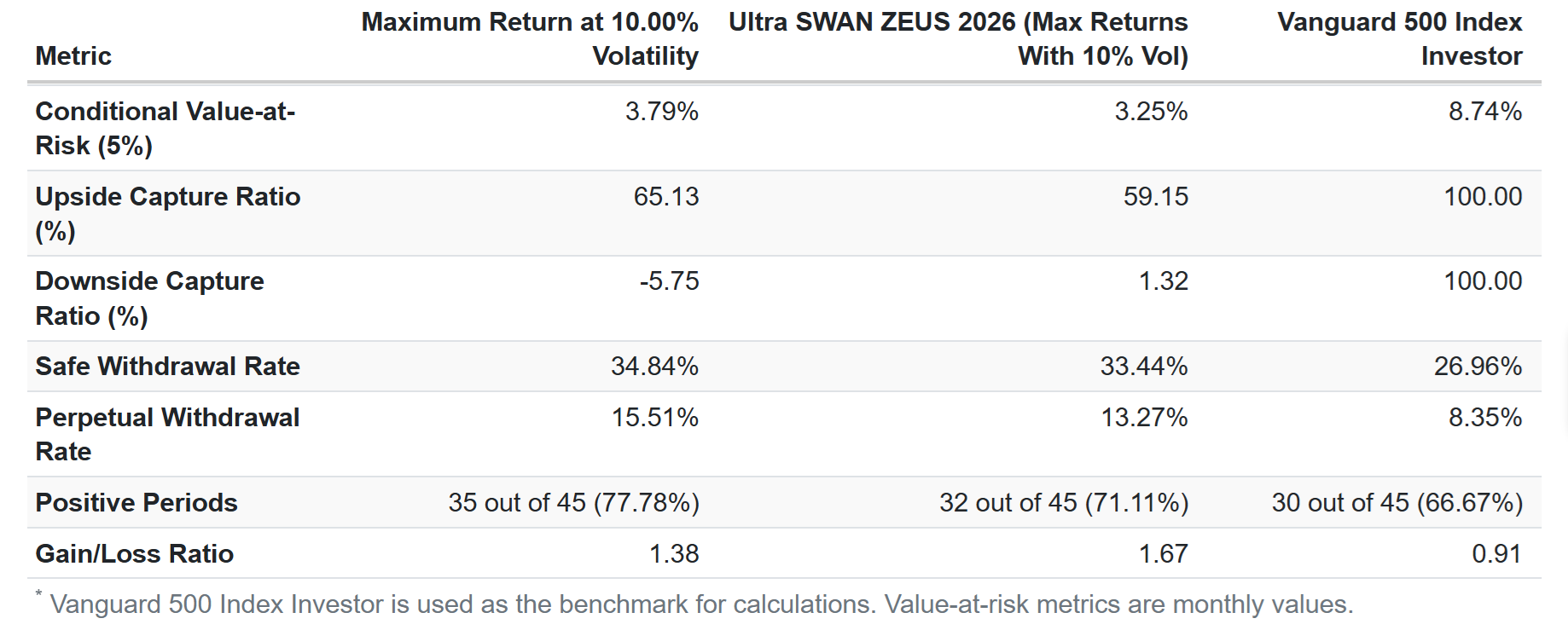

After all, the downside capture ratio on this better-performing version of Ultra ZEUS is the same, and the upside capture ratio is so much higher, and the tail-risk (conditional value at risk) is also the same.

CVAR = the average of 5% worst months = “realistic worst case” month.

BUT the S&P’s normal tail risk = 10%, which means this time frame is a low volatility period. And that says that this much more stock-heavy portfolio is actually overfitted.

So let’s replace VFLO with COWZ so we can test all the way back to April of 2022, a period of time with 16% annual stock volatility (vs historical 15%) instead of just 12%.

A better representation of historical volatility.

A more realistic Ultra ZEUS portfolio, with MELi and EPD replaced with PM and the negative-convexity ETFs reduced from 16% to 8% with CTA reduced by 5% (and NVDA still at 20%).

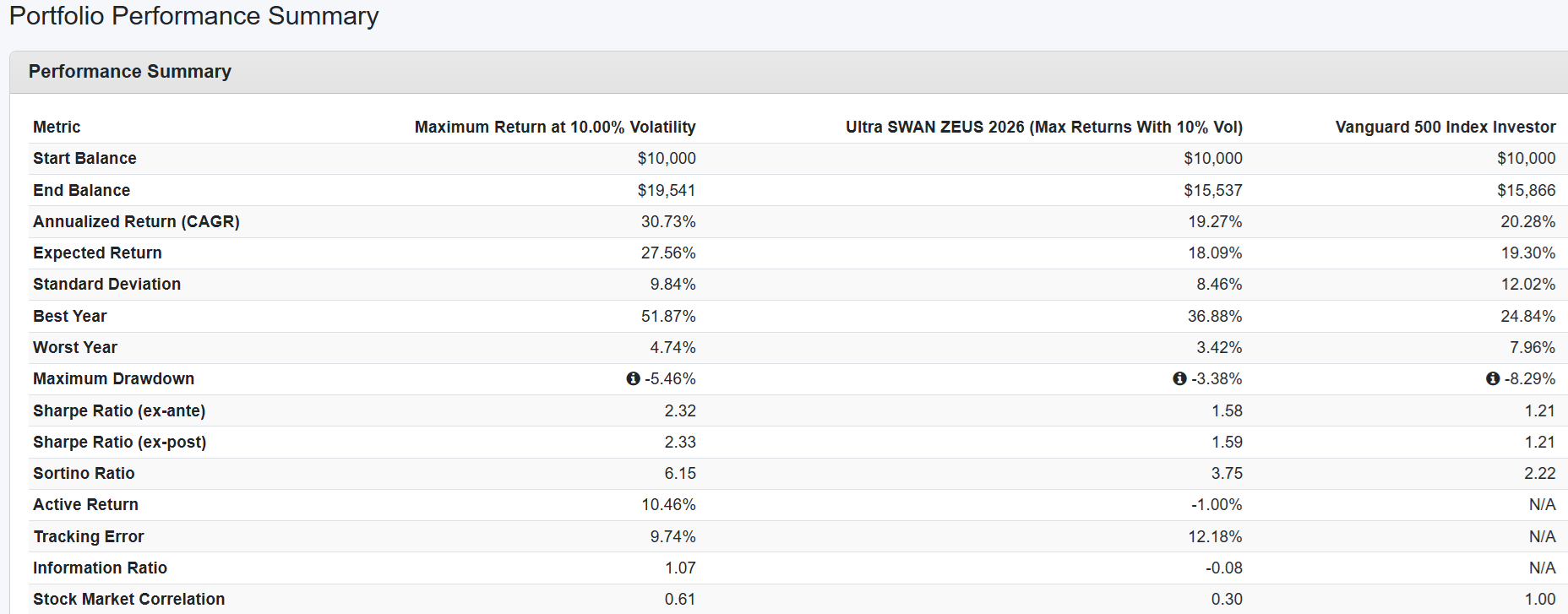

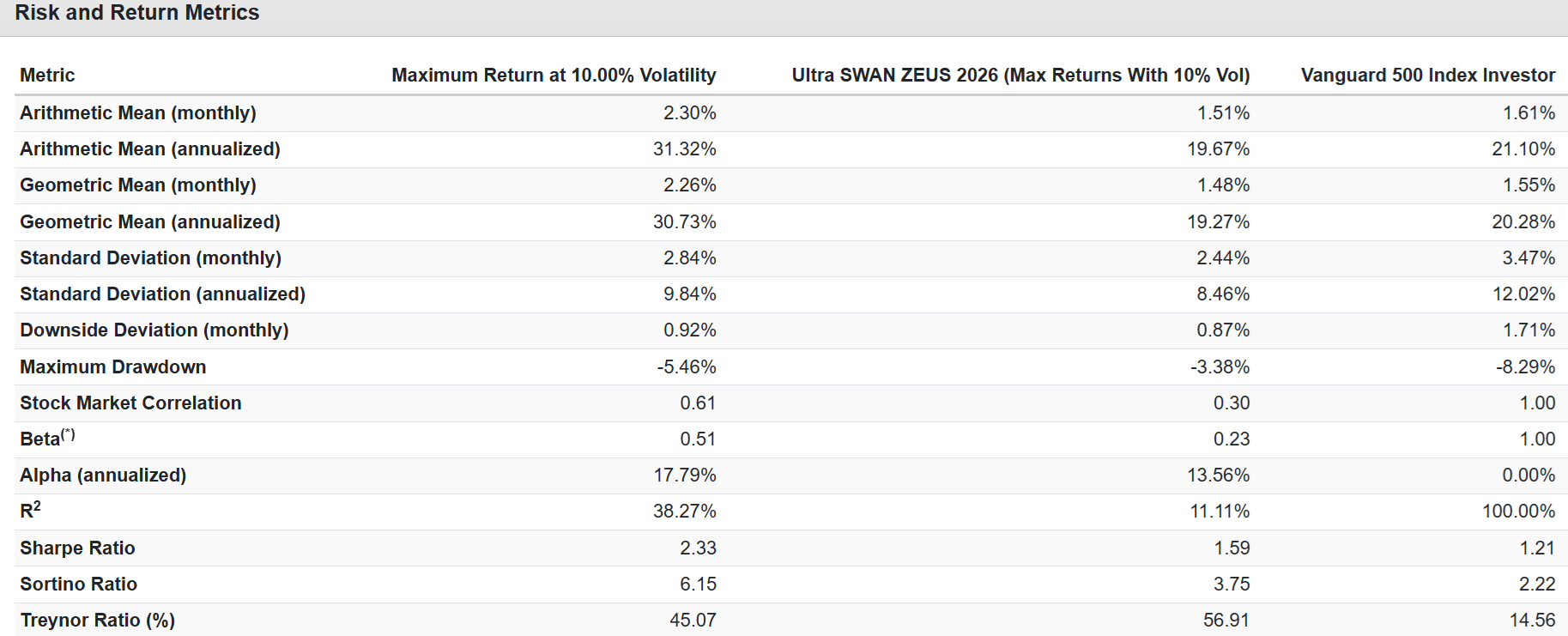

OK, but how does this compare to Ultra ZEUS in what matters most? The dual mandate of maximum returns for minimum volatility?

OK, and what about the volatility metrics?

The beta is identical at 0.32. OK, and what about the tail risk and downside captures?

It’s a better portfolio in terms of the reward/risk ratio (upside capture/downside capture) and has similar tail-risk and is up more consistently (79% of months instead of 71%).

OK, but what about the actual volatility of returns over time?

OK, that’s really impressive.

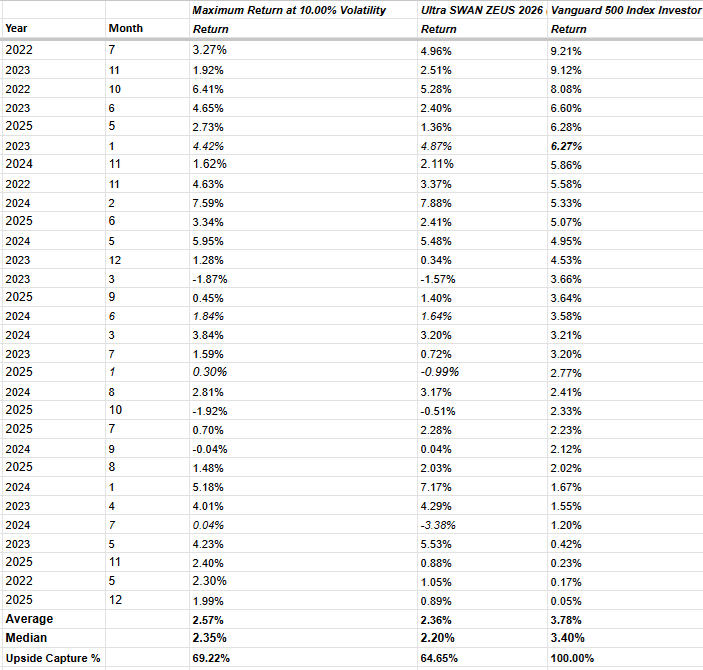

What about the monthly returns?

When The Stock Market Is Up (65% of Months)

That’s not surprising and a solid example of a highly defensive portfolio.

54% stocks, 46% hedges.

8% negative convexity hedges, 20% growth, 34% value, 38% managed futures

A promising improvement to a year when the stock market is expected to experience 20% FCF/share growth (23% if the tariffs are overturned).

Be only as defensive as is absolutely necessary to preserve the defensive characteristics, but otherwise bet on American economic and corporate profit growth greatness.

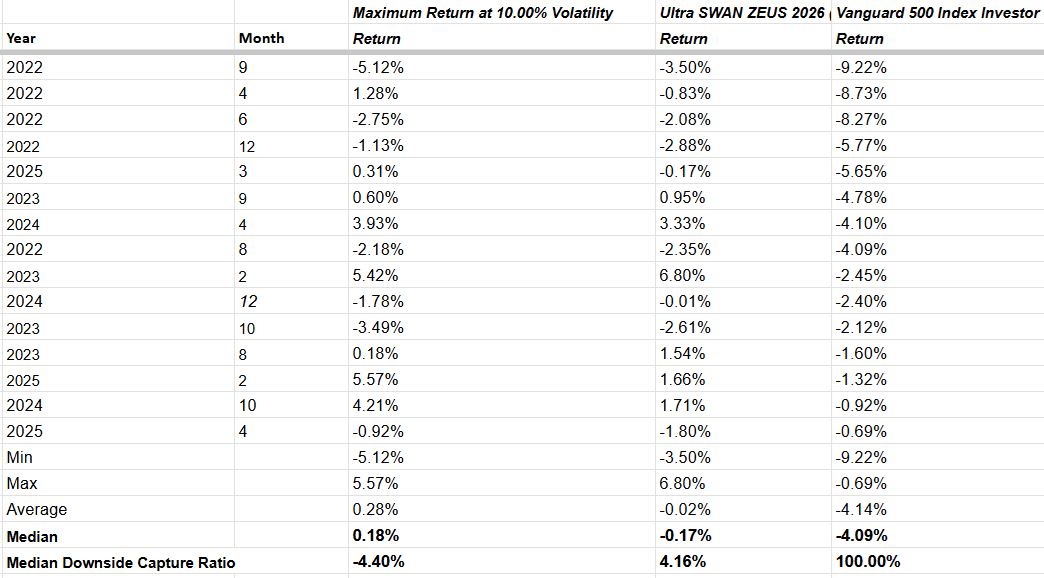

Months When The S&P Is Down

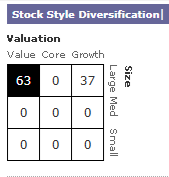

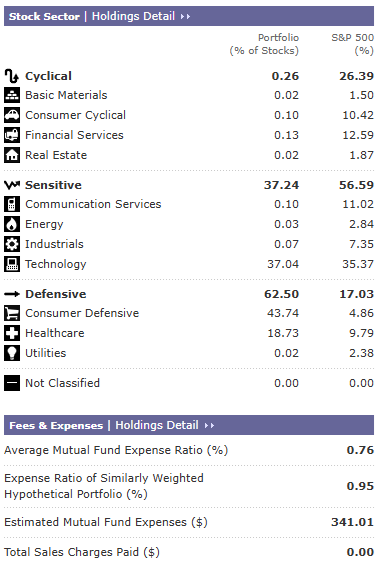

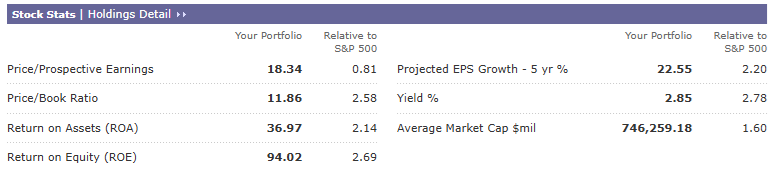

Morningstar Analysis of Ultra ZEUS V2

Let’s run Ultra ZEUS V2 through Morningstar and see how it compares to Ultra ZEUS.

A modest undervaluation but a still nice and low PEG of 0.95 with a forward PE of 19 (vs 16 right now).

The valuation profile isn’t as good (Ultra ZEUS V1 has a 16 PE vs 40 historical).

A more defensive portfolio.

A more concentrated portfolio, but a slightly lower risk one at the same time.

The yield is the same, the growth rate is slightly faster, the forward PE is a tad higher, but the returns on equity is about 20% higher.

22.55% growth + 2.85% yield (higher than VYM’s 2.7%) + 1.66% valuation boost (8% discount over 5 years) = 28.25% CAGR 5-year total return potential per Morningstar’s DCF models and analysts.

Ultra ZEUS V1 is 25% CAGR, up from 23% in the first version in 2023.

Conclusion: Switching to V2 Unless The Monthly “Top Buy List” Screening Finds An Even Better V3

I have to say Ultra ZEUS V2 is better than Ultra ZEUS. At the end of the month, we'll rebalance to V2, unless I figure out an even better version.

An extra 5% on the upside capture in a positive month and 10% better downside capture in a down month.

Owning PM instead of negative convexity ETFs is superior to our long-term goals.

If the evidence is compelling enough, and based on accurate data, I will change my mind and believe anything.😉😂🤣

Full Deep Dive Report

Courtesy of FactSet, Morningstar, and Gemini 3 Deep Research (Primary report), and Chat GPT 5.2 Pro Deep Research (Fact-checking and filling out any additional useful details that would be important to retired income investors).

Philip Morris International (PMI): Retirement Income Investment Report

Executive Summary:

Philip Morris International (PMI) stands out in 2026 as a premier income stock for retirees focused on dividend safety and low volatility. PMI has successfully pivoted from declining cigarette volumes to a growth trajectory centered on smoke-free nicotine products (notably IQOS heated tobacco and ZYN nicotine pouches), which now generate over 40% of its revenuelinkedin.compmi.com. The company offers a dividend yield around 3.6%-3.9% with 17 consecutive years of annual increasespmi.com, providing a reliable income stream that has grown faster than inflation. This dividend is well-covered by free cash flow despite occasional GAAP earnings distortions from non-cash write-downssuredividend.com. PMI’s balance sheet remains solid (rated A– by S&P)cbonds.com, and management is on track to deleverage after the 2022 Swedish Match acquisition, targeting ~2× net debt/EBITDA by 2026pmi.com. Key risks like regulatory changes have recently abated – notably, a proposed U.S. menthol cigarette ban was withdrawn in early 2025reuters.com, and a C$32.5 billion settlement in Canada resolved a major litigation overhang without direct impact on PMI’s cash flowsnasdaq.com. With growing contributions from smoke-free products (and U.S. expansion rights regained), PMI is positioned to deliver steady earnings growth (~9–12% annually through 2027). Its low beta (~0.4) indicates much lower stock volatility than the broader market, underscoring PMI’s suitability as a “sleep-well-at-night” core holding for retirement portfolios.

Adam’s Note: 55 year streak adjusted for the MO/PM spin-off.

Investment Summary & Key Takeaways:

Secure, Growing Dividends: PMI has increased its dividend every year since its 2008 spin-off, now paying an annualized $5.88 per sharepmi.compmi.com. The payout ratio on adjusted earnings is around 75%, indicating that the dividend is well-supported by free cash flow after funding growth investments. Even though GAAP earnings occasionally make the payout appear high (over 100% during impairment years), PMI’s strong cash generation ensures the dividend’s safetysuredividend.com.

Smoke-Free Transformation Validated: PMI has reinvented itself from a traditional tobacco company into a nicotine technology leader. Over 40% of net revenues now come from smoke-free products like IQOS and ZYNlinkedin.com, and management aims to exceed two-thirds by 2030pmi.com. This rapid transformation supports a higher valuation multiple than tobacco peers, as PMI is capturing growth where others are managing decline.

ZYN Dominance and U.S. Expansion: Thanks to the 2022 acquisition of Swedish Match, PMI owns ZYN, the U.S. market’s leading nicotine pouch brand. ZYN’s U.S. shipment volumes surged by about 37% year-on-year in 2025 despite supply constraintsreuters.com, underscoring massive demand. PMI is investing $600 million in a new Aurora, Colorado factory slated to start production in 2026denver7.com, which will resolve capacity bottlenecks and improve margins by localizing output. Notably, the FDA authorized all 20 ZYN pouch varieties in the U.S. through its stringent PMTA process in early 2025, cementing ZYN’s regulatory approval and competitive moatbusinesswire.com.

IQOS U.S. Re-Entry Catalyst: After regaining full U.S. rights, PMI is executing a careful U.S. launch for IQOS, its heated tobacco system. Pilot programs began in Austin, TX and later Fort Lauderdale, FLbusinesswire.com to refine the marketing approach. A major catalyst is expected when the FDA approves the latest-generation IQOS ILUMA device (PMI submitted applications in Oct 2023 and anticipates authorization by late 2025 or early 2026tobaccoreporter.com). ILUMA’s bladeless Smartcore induction heating eliminates the need for cleaningiqos.com and offers a superior user experience, which should accelerate smoker conversion in the U.S. once approval is granted.

Reduced Regulatory Risk: The regulatory climate has recently tilted in PMI’s favor. In January 2025, the new U.S. administration withdrew the FDA’s proposed menthol cigarette ban, removing a significant threat to the industryreuters.com. Meanwhile, a 2025 Canadian court settlement resolved all pending tobacco litigation for C$32.5 billionnasdaq.com. PMI’s Canadian subsidiary (RBH) has been deconsolidated since 2019 due to creditor protectionreuters.com, so the settlement (funded by RBH’s future cash flows) does not directly burden PMI’s balance sheetnasdaq.com. These developments clear two major clouds that had hung over tobacco equities.

Financial Strength and Deleveraging: PMI used debt to fund its smoke-free pivot (notably the $16 billion Swedish Match deal), but is now diligently deleveraging. Net Debt/EBITDA spiked to ~3× post-acquisition, but management is prioritizing debt reduction over buybacks, aiming for ~2× leverage by end of 2026pmi.com. This discipline protects PMI’s A– credit ratingcbonds.com and keeps interest costs manageable. The debt maturity profile is well-laddered (e.g. a 4.875% note due 2026 is the next significant maturity), and PMI has ready access to financing if needed at investment-grade rates.

Low-Volatility, Defensive Profile: PMI’s stock exhibits a 5-year beta of ~0.4, meaning it is only about 40% as volatile as the S&P 500. In practice, PMI tends to hold its value better during market downturns – a valuable trait for retirees. Its combination of stable, high-margin consumer-staple earnings and a secular growth kicker from smoke-free products makes PMI a defensive stalwart that can still deliver growth. This low volatility and reliable income earn PMI a place as a “core” holding in income-focused portfolios.

Tax-Efficient Income for U.S. Retirees: Despite PMI’s global footprint, U.S. investors enjoy favorable tax treatment on its dividends. PMI is incorporated in Virginia and qualifies as an “80/20” company (≥80% of income from non-U.S. operations)pmi.com. Therefore, PMI’s dividends are treated as qualified for U.S. tax purposes (taxed at lower long-term capital gains rates), and U.S. residents generally owe no foreign withholding tax on PMI payouts. This enhances PMI’s net yield compared to many foreign stocks.

Summary Tables and Charts: (Data as of January 2026)

Adam’s Note, the lower beta is compelling and indicates that PM might knock BTI and MO out of contention in a head-to-head optimization showdown.

Full Deep Dive Report

1. Introduction: The Case for PMI in a Retirement Portfolio

Retirees in 2026 face a challenging investment landscape. Fixed-income yields have risen from post-2008 lows, tempting some investors to favor bonds, yet equity markets (especially in tech) are pricey and volatile. In this environment, the ideal retirement investment is one that provides reliable, growing income, inflation protection, and capital stability. PMI fits this profile uniquely well.

Traditionally known as a tobacco company, PMI has transformed itself into what is essentially a “nicotine tech” company, pivoting aggressively away from cigarettes toward reduced-risk alternatives. This is not just semantics – it fundamentally alters PMI’s long-term outlook. Instead of presiding over a declining business (like Altria with U.S. cigarettes), PMI is leveraging technology (IQOS devices, novel nicotine pouches) to grow its user base and revenues. For retirees, this means PMI can offer both the defensive characteristics of a consumer staple and the growth potential of a tech-driven company.

With the full integration of Swedish Match (ZYN) and a major U.S. expansion underway, PMI’s growth profile through the late 2020s is far superior to that of legacy peers, even as it maintains a conservative financial approach suitable for income investors. The following sections delve into PMI’s dividend sustainability, financial strength, risk factors, growth drivers, and peer comparisons to illustrate why PMI is a compelling “sleep-well-at-night” stock for retirement portfolios.

2. Financial Architecture and Dividend Analysis

The first priority for any retirement investment is preservation of capital and reliability of income. PMI’s financial strategy is explicitly designed to support a stable and growing dividend while funding its business transformation.

2.1 Dividend Track Record and Safety

PMI has an outstanding dividend pedigree. Since its spin-off from Altria in 2008, PMI has raised its dividend every single year, now 17 consecutive years of increasespmi.com. As of January 2026, the quarterly dividend is $1.47 per share (annualized $5.88)pmi.com. This consistency reflects a corporate culture that treats the dividend as sacrosanct – essentially a fixed cost to be met before discretionary spending.

Adam’s note, 55 Year streak = Dividend King, S&P considers it a dividend king and so do I.

A common concern is PMI’s payout ratio, which on a GAAP earnings basis can appear high (even over 100% in certain years). For example, in 2024, PMI’s reported EPS was depressed by a $2.3 billion non-cash impairment for its Canadian unit, causing GAAP EPS of only $4.52suredividend.com. Naturally, paying $5.88 in dividends against $4.52 EPS yields a payout over 100%. However, this is an optical issue. PMI’s underlying free cash flow easily covered the dividend, and after adjusting for one-time charges, the payout was ~75% of adjusted earningssuredividend.com. As a Sure Dividend analysis noted, PMI has at times paid out more than its net income, yet due to strong cash flows and low capital needs “the dividend remains relatively well-covered”suredividend.com. In essence, PMI’s true payout ratio hovers in a safe 70–80% range when excluding currency hits and special charges – a “sweet spot” that balances a generous return to shareholders with some retained cash for debt reduction and reinvestment.

Free Cash Flow (FCF) is the more relevant metric for dividend safety. In 2025, PMI generated about $12 billion in operating cash flow and had capital expenditures around $1.5 billion, leaving ample FCF to cover roughly $8 billion in annual dividends. Even during heavy investment cycles, PMI’s dividend has been fully FCF-funded. This gives comfort that PMI can continue its streak of annual raises. Management’s stated target is a ~75% payout over timepmi.com, allowing for modest dividend growth roughly in line with earnings growth.

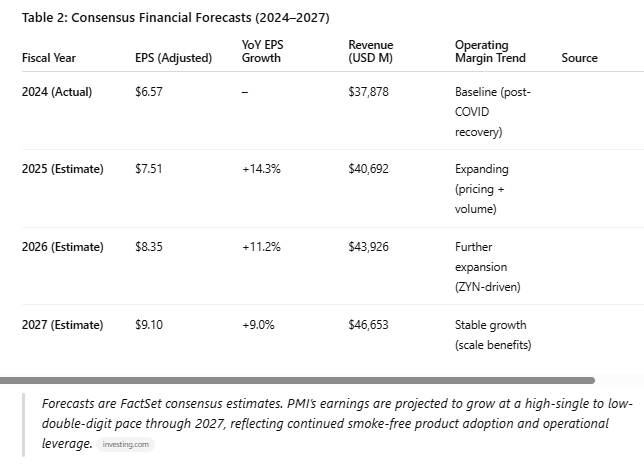

In summary, PMI’s dividend is safe and likely to keep growing. The company’s earnings are on an upswing (FactSet consensus expects ~9–12% EPS growth annually for the next few years), and the dividend will be lifted accordingly (recent increases have been in the mid to high single digits). Retirees can count on PMI for a steady, inflation-beating income stream.

2.2 Free Cash Flow Coverage and Capital Allocation

Beyond dividends, PMI’s capital allocation priorities have balanced debt management and growth investment. During 2023–2024, PMI temporarily paused share buybacks (after ~$1 billion repurchased in 2021–22) to focus on integrating Swedish Match and reducing debtpmi.compmi.com. This prudence benefits dividend investors because it strengthens the balance sheet supporting those dividends.

By early 2026, with leverage coming down (see Section 6.1), PMI has hinted it may reinstate share repurchases once its leverage goal (~2× EBITDA) is in sightinvesting.com. A resumed buyback (if announced in 2026–27) would further boost EPS and signal management’s confidence in cash flows. However, PMI has made clear that debt reduction and dividend growth take precedence over buybacks in the near terminvesting.com.

It’s worth noting PMI’s capacity to invest in growth without jeopardizing dividends. Even while paying out ~75% of earnings, PMI has funded the rollout of IQOS worldwide and the expansion of ZYN production. For instance, the new $300 million+ U.S. factory for ZYN (Aurora, CO) is being paid for out of operating cash flowtruthinitiative.orgdenver7.com. PMI’s capital expenditures (~$1.5 billion/year) remain modest relative to its $11–12 billion in annual operating cash flowpmi.com. Thus, PMI can invest sufficiently in capacity and product development to secure future growth, all while sustaining its dividend. This is a hallmark of a well-managed income stock.

2.3 Tax Considerations for U.S. Investors

Retirees often worry about the tax implications of international holdings. PMI, despite its global operations, is actually a U.S.-incorporated company (Virginia) and is exceedingly tax-friendly for U.S. shareholderspmi.compmi.com:

Qualified Dividends: PMI’s dividends qualify for the lower long-term capital gains tax rates (0%, 15%, or 20% depending on income) for U.S. investors, rather than higher ordinary income ratespmi.com. This materially increases after-tax yield for retirees.

No Foreign Withholding: Because PMI meets the “80/20 company” rule (the vast majority of its business is outside the U.S.), it is effectively treated as a domestic payer for tax purposespmi.com. There is no Swiss or international withholding tax deducted from PMI’s dividend for U.S. residents. This contrasts with many foreign stocks (e.g., British American Tobacco) where a portion of the dividend is lost to foreign tax.

In practice, owning PMI is as simple as owning any blue-chip U.S. stock from a tax perspective. Investors still should consult their tax advisor for individual circumstances, but generally PMI’s dividend enjoys the most favorable tax treatment available.

3. Growth Engines: IQOS and ZYN Drive a Smoke-Free Future

The crux of PMI’s investment thesis – and what differentiates it from a high-yield bond proxy – is the growth potential embedded in its smoke-free product portfolio. Unlike its peers, PMI is not relying on price hikes alone; it has real volume growth drivers.

By Q3 2025, smoke-free products contributed 41% of PMI’s net revenueslinkedin.com and an even higher share of gross profit. Management’s ambition is to become a majority smoke-free company by 2025 and about two-thirds smoke-free by 2030pmi.com. Let’s examine the two flagship platforms enabling this transformation:

3.1 IQOS: Heated Tobacco Leadership

IQOS is PMI’s heated tobacco system, which consists of devices that warm tobacco sticks (branded HEETS or TEREA) to release nicotine aerosol without burning tobacco. IQOS has been a runaway success internationally:

Market Adoption: In key markets like Japan, IQOS has achieved remarkable penetration. By early 2025, PMI reported that heated tobacco units (HTUs) exceeded 50% of total nicotine product sales in many major Japanese cities, and nationally IQOS’s HTU share reached a record 32.2% of the tobacco marketpmi.com. This is up from virtually zero a few years ago, proving that smokers will switch at scale when offered a satisfying alternative. IQOS is also the leading brand in many EU countries for heated tobacco, with over 11% share of the overall tobacco market in Europe and much higher in cities like Athens and Romepmi.com.

Technology Edge: The latest IQOS ILUMA device uses a Smartcore Induction System™, a bladeless heating method that heats the tobacco from within the sealed stickiqos.com. This innovation eliminated the main pain points of earlier devices (no more blade breakage or tedious cleaning required). As a result, ILUMA provides a more convenient and consistent user experience, which has driven higher user retention. The elimination of cleaning is a major advantage over competitors’ devices and over earlier IQOS versions – it makes the product truly plug-and-play like a cigaretteiqos.com.

Economic “Razor & Blade” Model: IQOS employs a classic recurring revenue model. PMI sells the electronic device (one-time sale, often at a discount) and then makes steady profits on the consumables (the tobacco sticks). Because heated tobacco sticks are taxed somewhat lower than cigarettes in many markets (due to reduced harm policies) while sold at comparable prices, PMI’s margin on HTUs can exceed that of cigarettes. This dynamic – more profit per stick plus the potential for users to consume nearly as many sticks as before – means IQOS can boost PMI’s profitability as it scales. Already in H1 2025, smoke-free products (mostly IQOS) accounted for 44% of PMI’s gross profitpmi.com, indicating healthy margins.

Regulatory Moat: PMI’s IQOS is the only inhalable nicotine product to receive FDA’s “Modified Risk Tobacco Product” (MRTP) authorization (granted in July 2020 for IQOS 2.4 and in 2022 for IQOS 3)tobaccoreporter.comtobaccoreporter.com. The MRTP status means IQOS can be marketed (in the U.S.) with claims like “reduces exposure to harmful chemicals” – a powerful differentiator that no e-cigarette or other heated tobacco product has in the U.S. so far. This underscores PMI’s scientific lead and creates a high barrier to entry. PMI has also obtained PMTA (premarket) authorizations for multiple IQOS versions, something very few companies have achieved for any tobacco producttobaccoreporter.com.

Looking ahead, the U.S. re-launch of IQOS is a huge opportunity. IQOS was pulled from the U.S. in late 2021 due to a patent dispute (now resolved)tobaccoreporter.com. PMI now has full rights as of April 2024 and is reintroducing IQOS methodically. As noted, pilot sales are ongoing in a couple of cities with the IQOS 3 device. But the real inflection will come with IQOS ILUMA’s U.S. debut once FDA grants approval, expected by 2026tobaccoreporter.com. Given ILUMA’s improved user appeal, PMI expects adoption in the U.S. (where ~30 million still smoke) to be significant. The company has set a goal to capture 10% of the U.S. nicotine market by 2030tobaccoreporter.com – a target that, if reached, would add tens of billions in revenue. Achieving even a portion of that would sustain PMI’s growth for many years.

In sum, IQOS provides PMI a “second act”: a product with rising volumes, pricing power (since it’s unique), and reduced regulatory risk (authorities prefer smokers switch to IQOS rather than continue smoking). This stands in stark contrast to Altria, which has no successful heated product (it recently bought NJOY e-vapor, but that is tiny) and to BAT, whose glo heated device is far behind IQOS in market share.

3.2 ZYN: The Oral Nicotine Phenomenon

The other star of PMI’s portfolio is ZYN – a nicotine pouch that contains pharmaceutical-grade nicotine and flavor crystals, but no tobacco leaf. Users place the pouch between the gum and lip to absorb nicotine, much like snus, but ZYN is tobacco-free. This product was acquired via Swedish Match in late 2022 and has proven to be a game-changer in the U.S.:

Explosive Growth: ZYN is experiencing growth rarely seen in consumer staples. In 2025, U.S. shipment volumes of ZYN jumped roughly 37% year-over-yearreuters.com. The growth was actually constrained by supply – PMI struggled to produce enough to meet demand through much of 2024. By Q1 2025, as new capacity came online, U.S. ZYN shipments exceeded 200 million cans in the preceding 12 monthspmi.com, and growth accelerated to +53% year-on-year as stock shortages began to easepmi.com. ZYN’s rapid rise has made it the dominant U.S. nicotine pouch brand, far outselling the next competitor (BAT’s Velo and Oral On! have single-digit share). The brand’s momentum is so strong that it has been called “the fastest growing brand in U.S. convenience stores across all categories”linkedin.com.

Supply Expansion: Recognizing the immense demand, PMI is heavily investing to expand ZYN production. The company built a large new factory in Aurora, Colorado, slated for first output by late 2025 and full production in 2026denver7.com. Additionally, it expanded an existing plant in Kentucky, targeting total capacity of ~900 million cans annually by 2025truthinitiative.org. These investments (totaling over $800 million) will ensure PMI can keep shelves stocked and even expand distribution (ZYN is still rolling out in some markets and retail channels). Importantly, local U.S. manufacturing also lowers unit costs and speeds up innovation/response to demand. The bottleneck that limited ZYN sales is effectively being removed, which bodes well for continued double-digit growth.

Regulatory Endorsement: In January 2025, the U.S. FDA granted marketing authorization (PMTAs) for all 20 ZYN pouch varieties that Swedish Match sellsbusinesswire.com. This was a landmark because it made ZYN the only FDA-authorized nicotine pouch on the U.S. market. Competing products (often made by smaller firms or sold as “synthetic nicotine” products) did not go through the approval process and face regulatory crackdowns or eventual removal. Thus, ZYN now enjoys a de facto regulatory moat – it is officially vetted as appropriate for public health (for adult smokers seeking alternatives)truthinitiative.org. This not only validates PMI’s approach to harm reduction but also protects ZYN from being copied by unapproved rivals. As long as PMI maintains strict quality and marketing standards, ZYN should remain in the FDA’s good graces.

Margin and Brand Power: ZYN’s economics are attractive. It’s a premium-priced product with a loyal following (repeat usage is high once people switch from cigarettes or vape). Swedish Match’s experience showed they could raise price ~4% annually without hurting volumes, indicating strong brand equity. From a cost standpoint, nicotine pouches are cheaper to make than cigarettes (no costly tobacco leaf, simpler manufacturing). With scale, ZYN likely carries high margins, contributing substantially to PMI’s earnings growth. It also diversifies PMI’s portfolio, as it caters to consumers who might not want to vape or use a device like IQOS. This broadens the reach of PMI’s smoke-free mission.

It’s worth highlighting that ZYN is fueling growth not just in the U.S. PMI is introducing nicotine pouches in other markets (often under ZYN or local brand names). For example, it’s seeing promising uptake in Scandinavia (where oral nicotine is culturally accepted) and even emerging markets like Pakistan and South Africapmi.com. While the U.S. will remain the largest profit pool for ZYN (due to sheer size of the market and higher pricing), international expansion adds another leg of growth in the late 2020s.

For retirees assessing PMI, the rise of ZYN is crucial. It demonstrates that PMI is not a one-trick pony tied only to IQOS – it has another independent growth engine. Nicotine pouches could appeal to a segment of smokers who don’t want to inhale anything, giving PMI a shot at converting those who may not try IQOS or e-cigarettes. This multi-pronged approach increases the probability that PMI can keep growing total nicotine users, or at least share-of-users, even as global smoking rates decline.

In sum, IQOS and ZYN are transforming PMI’s business mix, with combustible cigarettes increasingly taking a back seat as a cash cow. This transformation underpins PMI’s valuation premium and its long-term viability, which is crucial for an income investor with a 10+ year horizon. Whereas a pure cigarette company faces inevitable volume decline, PMI can offset (and indeed exceed) those declines with IQOS and ZYN growth.

4. U.S. Market Expansion: A New Frontier

For over a decade after its 2008 spin-off, PMI was absent from the United States market (Altria had the U.S. rights to Marlboro and IQOS). That changed dramatically in recent years: PMI re-acquired U.S. IQOS rights (effective April 2024)tobaccoreporter.com and bought Swedish Match (giving it U.S. ZYN and a U.S. salesforce). Now, PMI views the U.S. as a critical growth market – understandably, since the U.S. is the world’s largest profit pool for tobacco/nicotine.

Effective January 1, 2026, PMI even reorganized its entire company to reflect this focus, creating a separate PMI U.S. division alongside PMI Internationalpmi.compmi.com. This structural change underscores how important the American market is to PMI’s future. Let’s explore what PMI is doing in the U.S.:

4.1 U.S. Strategic Realignment

Under the new organizational model, Stacey Kennedy serves as CEO of PMI U.S., and will drive the U.S. strategy focusing on both ZYN and IQOSpmi.compmi.com. PMI’s decision to split reporting segments into “International Smoke-Free”, “International Combustibles”, and “U.S.” segments from 2026 onward means investors will get clearer visibility into U.S. performancepmi.com.

This move should be seen as a positive: it implies accountability and empowerment of the U.S. team to aggressively grow market share. The U.S. unit can tailor marketing and distribution specifically to American consumer preferences (which do differ from Europe or Asia). It also may pursue U.S.-specific partnerships or acquisitions if needed. PMI has relocated its corporate headquarters to Stamford, CT, and has manufacturing in North Carolina (for IQOS heatsticks) and Kentucky (for ZYN)businesswire.com – indicating it’s “all-in” on building a U.S. presence, not just exporting products from abroad.

From an investor standpoint, success in the U.S. provides currency diversification and a natural FX hedge (more U.S. dollar earnings to offset the impact of a strong dollar on overseas earnings)reuters.com. It also potentially unlocks a massive new earnings stream. PMI essentially has the opportunity to compete for the 30 million U.S. smokers that Altria currently services – but with reduced-risk products that Altria lacks. If PMI captures even a fraction of them, the incremental revenue and profit are substantial.

4.2 IQOS U.S. Rollout Progress

PMI’s approach to the U.S. IQOS rollout has been cautious but deliberate:

Pilot Markets: In late 2024, PMI launched a “IQOS ILUMA City Pilot” in Austin, Texastobaccoreporter.com. Austin was chosen for its tech-savvy demographics and perhaps more receptive regulatory climate. The pilot was aimed at testing marketing tactics, pricing, and consumer responses. The results were positive enough that PMI expanded the pilot to Fort Lauderdale, Florida in 2025businesswire.com. In these pilots, thousands of smokers signed up for the “Be the First” program to try IQOSbusinesswire.com. PMI gained valuable insight into American adult smokers’ preferences (menthol vs. regular, device financing models, need for retail kiosks, etc.). By 2025, IQOS was commercially available in Austin and building a presence in South Florida, with dedicated IQOS stores/lounges and even a tie-in promotion at the Miami Formula 1 Grand Prixbusinesswire.com.

Regulatory Status: Currently, PMI is restricted to selling the older IQOS 3. Why not ILUMA already? Because PMI wisely decided to file ILUMA through the FDA’s MRTP and PMTA process (applications submitted Oct 2023tobaccoreporter.com). Rather than flood the market with the older tech, PMI wants to wait for ILUMA’s likely clearance. The FDA review is expected to complete by late 2025 or early 2026tobaccoreporter.com. Once ILUMA is authorized, PMI can market it with reduced-exposure claims (thanks to MRTP precedent from earlier IQOS versionstobaccoreporter.com) and leverage its better user experience. This suggests a national rollout in the U.S. could start in earnest in 2026, possibly with a marketing blitz and broader city launches as ILUMA becomes available.

Competitive Landscape: In the U.S., the main competition in alternatives is vaping (e-cigarettes like Juul or Vuse). No other heated tobacco product is being sold currently (BAT’s Glo is absent; Japan Tobacco’s Ploom not in the U.S.). This means PMI has a first-mover advantage in heated tobacco. Vaping has made huge inroads among U.S. smokers, but IQOS offers a different value proposition – it uses real tobacco (some smokers prefer that) and has a ritual closer to cigarettes. Also, IQOS devices are only sold to adults 21+ with heavy controls, whereas the vaping category has been dogged by youth usage issues. PMI’s positioning of IQOS as a controlled, clinically-backed product could appeal to regulators and certain consumers. The withdrawal of the menthol ban also helps IQOS – had menthol cigarettes been banned, that might have pushed menthol smokers to try illicit vapes instead of IQOS. Now, with no ban, PMI has to compete for menthol smokers the old-fashioned way, but at least the playing field remains stable, and IQOS does have menthol HeatSticks which menthol smokers can try.

The bottom line is that PMI’s re-entry into the U.S. is a significant upside driver not reflected in historical results. The U.S. operations in 2025 were still relatively small (just a few hundred million in revenue mainly from ZYN). By 2028 or 2030, U.S. revenue could be in the many billions if IQOS gains traction. This is akin to a large new market opening up for PMI – something Altria cannot replicate since it’s confined to the U.S. already, and BAT struggles with (BAT is in the U.S. via Reynolds American, but primarily with legacy products and Vuse e-cig, which, while #1 in U.S. vaping, is facing heavy competition and regulatory uncertaintly). PMI thus has a unique dual-market growth story: mature markets overseas switching to smoke-free AND a nascent U.S. expansion.

5. Regulatory and Litigation Landscape

Tobacco is a heavily regulated industry, and any income investor must weigh regulatory risk. However, as noted in the Key Takeaways, the regulatory climate as of 2026 has actually improved for companies like PMI, especially relative to worst-case fears from a few years ago.

5.1 Menthol and Flavor Bans: Winds of Change

In 2022, the FDA under the prior administration proposed a nationwide ban on menthol cigarettes and flavored cigarsreuters.com. Menthols are ~30% of the U.S. cigarette marketreuters.com and a ban would have been a severe hit to Altria and BAT (though PMI itself doesn’t sell cigarettes in the U.S.). For a while the ban seemed imminent, but political changes intervened. On January 21, 2025, the new (Trump) administration withdrew the proposed menthol banreuters.com. This was confirmed by a White House regulatory filing and widely reported by Reutersreuters.com. The ban’s withdrawal is critical for the industry’s stability.

Even though PMI doesn’t directly sell U.S. menthol cigarettes, the ban would have caused market disruption – potentially driving smokers to illicit products or higher quit rates, shrinking the overall nicotine market that PMI is now entering. Its removal keeps the status quo. Moreover, it suggests the current U.S. administration is less inclined to pursue prohibition-style tobacco regulations. This reprieve extends to flavors in cigars (Swedish Match had a cigar business that would have been impacted, although PMI might exit that business anyway).

Additionally, the FDA in 2022 had floated the idea of mandating ultra-low nicotine cigarettes (to reduce addiction). That too seems to be on the back burner with the change in leadership. For PMI, the absence of these drastic measures means it can execute its smoke-free transition with less external shock. Regulatory stability is invaluable for planning and valuation – investors can be more confident that the cash flows from combustibles (though declining slowly) won’t fall off a cliff due to a sudden ban. And those combustible cash flows are what fund the dividend and new product investment in the interim.

5.2 Litigation Settlements: Clearing the Deck

Litigation is another perennial risk for tobacco. A major headline in 2025 was the resolution of the Canadian tobacco class actions. After over two decades of legal battles, a global settlement was reached to resolve all outstanding Canadian tobacco lawsuits for C$32.5 billion in March 2025nasdaq.com. This settlement included PMI’s Canadian affiliate Rothmans, Benson & Hedges (RBH).

The important part: RBH has been under creditor protection (CCAA) since 2019 and was deconsolidated from PMI’s accountsreuters.compmi.com. PMI did take a one-time impairment charge in 2024 anticipating the settlementpmi.com, but going forward PMI will not be paying this settlement out of its own pocket. RBH will fund its portion through its own future profits and a big initial payment (likely using a form of structured payout overseen by the Canadian courts)nasdaq.com. In fact, PMI stated the implementation of the plan is expected in 2025 with “no impact on its consolidated financial statements”nasdaq.com.

This effectively rings fences a huge potential liability. It means PMI’s global cash flows and dividend are shielded from the Canadian settlement, beyond what’s already been expensed. It’s a relief because earlier, the uncertainty around Canada (and other lawsuits) often weighed on valuations. Now there is more clarity: in the U.S., the industry has the 1998 Master Settlement Agreement, and in Canada, this new settlement closes the book. There will always be litigation risk (e.g., small cases pop up internationally), but nothing of the scale of these has been looming.

5.3 Ongoing FDA Oversight: A Double-Edged Sword

PMI actually thrives under stringent regulatory oversight relative to smaller competitors, because PMI can meet the high standards:

Modified Risk and PMTAs: As mentioned, PMI remains the only company with an MRTP for a nicotine inhalation product (IQOS)tobaccoreporter.com. Also, Swedish Match (now PMI) got the first-ever MRTP for a smokeless product (General Snus in 2019) and now has the only authorized pouch (ZYN)businesswire.compmi.com. These achievements are akin to an “FDA seal of approval” that solidify PMI’s products’ legitimacy. The FDA’s rigorous review is a high barrier that PMI has repeatedly proven capable of clearing.

Competitive Filtering: In the e-cigarette space, FDA has denied millions of vape product applications. Many small players’ products are technically illegal or under enforcement discretion. Similarly, for nicotine pouches, as noted, ZYN is alone in being authorized; many rivals face potential removal. For PMI, this is an opportunity to grab market share as competitors get weeded out. It’s already happening in pouches – e.g., one competitor, On! (owned by Altria) had been allowed to stay on market pending review, but if it doesn’t get authorized, its growth will stall. ZYN’s recent FDA nod in Jan 2025 gives it a major marketing point and assurance to retailers that it’s here to staytruthinitiative.org.

Science and Harm Reduction: PMI has invested over $9 billion in R&D for smoke-free products. It has a scientific workforce publishing studies, running clinical trials, etc. This not only has led to approvals, but positions PMI favorably as regulators globally consider how to handle new nicotine products. PMI can engage with regulators armed with data. The U.S. FDA’s granting of MRTP for IQOS explicitly found that IQOS “[reduced] exposure to harmful chemicals” for smokers who switchtobaccoreporter.com, validating PMI’s harm reduction narrative. As more public health bodies accept the continuum of risk, PMI’s early lead could translate into policy advantages (e.g., tax differential maintenance, positive labeling).

In short, PMI has navigated the regulatory minefield effectively, turning what could be threats into areas of strength. The key risks to monitor now are mostly macro (currency, which we discuss next) and execution of the U.S. expansion, rather than existential legal or regulatory threats.

6. Financial Outlook: Debt, Currency, and Volatility

We’ve covered growth and dividends; now a brief look at other financial factors relevant to PMI’s risk/reward profile for retirees:

6.1 Debt and Deleveraging

PMI took on significant debt for the Swedish Match acquisition (approximately $16 billion) and to a lesser extent for previous buybacks. At its peak, net debt was about $40+ billion, and net debt-to-EBITDA reached ~3.0× in 2023. Management publicly committed to reduce this to ~2.0× by 2026pmi.com.

Progress is underway: by late 2025, net debt/EBITDA was already trending down (approx. 2.5×) through a combination of EBITDA growth and actual debt paydowntobaccoinsider.com. PMI has been prioritizing using excess cash for debt reduction over share repurchases. This is prudent and bond-rating agencies have responded. Fitch Ratings, for instance, revised PMI’s outlook back to Stable in 2025 citing “meaningful progress in deleveraging towards its target of 2×”fitchratings.com. S&P in March 2025 affirmed PMI’s A– credit rating with stable outlookcbonds.com, reflecting confidence that the company will manage its balance sheet conservatively.

PMI’s debt is well-structured: its maturity profile is staggered so that no single year poses a refinancing cliff. For example, the next major maturity is a $1.7 billion 4.875% note due Feb 2026bondblox.com. PMI has plenty of liquidity and likely will refinance part of it in advance or potentially redeem some (PMI recently announced it would redeem a portion early)finance.yahoo.com. Other large maturities fall in 2028 and 2030, giving PMI time to retire debt gradually. With an A– rating, PMI’s new debt issuances have reasonably low coupons (though higher than the ultra-low rates of a few years ago, of course).

For retirees, PMI’s handling of debt is reassuring. The company maintains an interest coverage ratio well above 10×, and its interest expense is only ~5% of operating profit (not a threat to profitability or dividends). By reducing leverage, PMI is also preserving future flexibility – once at 2× leverage, PMI could resume buybacks or pursue bolt-on acquisitions without jeopardizing the dividend or rating. It’s essentially future-proofing its balance sheet for a higher-rate world.

6.2 Currency Exchange Rates

One of PMI’s peculiar traits is that, historically, 100% of its revenue was ex-U.S., but it reports in U.S. dollars. This has made it extremely exposed to currency swings. A strong dollar can reduce the reported USD value of PMI’s international sales and profits (a “translation tax”). In 2022 and 2023, the dollar’s strength shaved several percentage points off PMI’s reported growthpmi.compmi.com. For example, in 2023 PMI’s adjusted EPS grew 11.9% in constant currency but only ~8.7% in USD due to exchange headwindssimplywall.st.

PMI employs hedging to smooth some short-term volatility (it hedges a portion of major currency cash flows), but it cannot eliminate currency impact for the long-term. However, the expansion of U.S. operations is naturally reducing PMI’s FX exposure. As ZYN and eventually IQOS generate more revenue in U.S. dollars, a growing share of PMI’s earnings will be in USD, providing a natural hedgereuters.com. By 2027, if perhaps 15–20% of sales are from the U.S., that’s 15–20% less that is subject to translation when the dollar swings.

In the meantime, investors should be aware that currency moves can cause short-term noise in PMI’s results. A weakening of emerging market currencies (e.g., in Latin America or Eastern Europe) or a strengthening of USD against the Euro or Yen will affect quarterly earnings. That said, these FX fluctuations typically don’t affect the underlying local profitability or the dividend (which is set in USD). Long-term, currencies tend to ebb and flow. As of early 2026, the dollar remains relatively strong, but off its 2022 peak, and PMI’s guidance for 2025 assumed a mid-single-digit drag from currency which may moderate going forwardpmi.compmi.com.

For a retiree, the key takeaway is: PMI’s underlying growth is what drives dividend increases; currency may mask or accentuate it in the short run but is less important over a 5+ year horizon especially as PMI diversifies currency mix. One could even view PMI as providing some international diversification in an income portfolio – if the dollar weakens, PMI’s reported earnings would get a boost.

6.3 Volatility and Beta Analysis

We have noted PMI’s low beta (around 0.4–0.5). Concretely, over the last five years PMI’s stock price movements have had very low correlation with the broad market. During sell-offs, tobacco stocks often fall less (or even rise if investors seek defensive sectors). For instance, in the sharp COVID crash of March 2020, PMI dropped but far less than the S&P, and it recovered faster thanks to steady earnings and dividend continuity.

PMI also generally has a lower standard deviation of returns day-to-day compared to the market. This can be attributed to its stable demand (people consume nicotine in good times and bad), its substantial dividend (investors hold it for income, which can dampen speculative trading), and its lack of extreme valuation swings (PMI never got caught up in bubble territory valuations).

For retirees, this means PMI can act as a stabilizer in a portfolio. It’s the classic defensive stock: when recession fears rise, PMI’s earnings might actually hold up or even improve (smokers tend not to quit en masse during recessions; some consumption patterns even increase stress-related consumption). Additionally, PMI’s share price, while not immune to downturns, tends to be resilient. Its five-year β of ~0.44 implies that if the market fell 10%, PMI might statistically fall only ~4.4% (actual performance will vary, but historically it has indeed been less volatile).

Of course, low volatility doesn’t mean no volatility. Tobacco stocks can react to industry news (regulation, litigation, etc.). We saw that in October 2023 when reports of potential menthol ban progress (later moot) caused a dip, or when interest rates rising made high-yield sectors temporarily less attractive. But over time, the combination of that hefty dividend and steady earnings tends to put a floor under PMI’s stock.

In practical terms, an investor relying on PMI for income can have a bit more confidence that their capital value will not gyrate wildly. This is important for retirees who might need to draw principal or just for peace of mind. One can “sleep at night” with PMI in the portfolio to a greater extent than with, say, a tech stock or even the broader index.

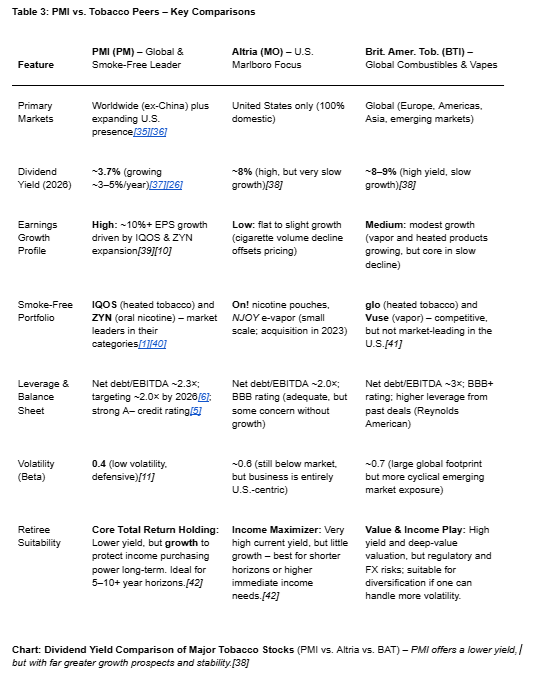

7. Peer Comparison: Why PMI Stands Out

To truly appreciate PMI’s position, it helps to compare it with its main peers – Altria Group (MO) and British American Tobacco (BTI). All three are popular income stocks, but their profiles differ:

Altria (MO): Yields about 8%, the highest of the group. It operates only in the U.S., selling Marlboro cigarettes and some other tobacco products (cigars, chew) and has a 10% stake in AB InBev. Altria’s growth is anemic; cigarette volumes decline ~5% yearly and it has struggled to develop a viable smoke-free product (its past investments in Juul e-cig and Cronos cannabis resulted in write-downs). It recently acquired NJOY (a small vape company) and sells On! pouches, but these have tiny market shares. Essentially, Altria is milking cigarettes for cash to pay its dividend and buy back shares, accepting volume decline. It’s a pure yield play, suitable for maximum current income, but the dividend growth is minimal (a penny per share per quarter increase recently, ~4% annual). There is also more regulatory risk directly for Altria (if FDA revisited menthol or nicotine caps). Altria’s payout ratio is about 75% of earnings, similar to PMI, but with declining earnings that’s more worrying longer-term. The market assigns Altria a ~9× forward P/E – a steep discount reflecting concerns over its terminal value.

Adam’s Note: MO yields 7.1% (AI appears to be VERY bad at real-time dividend yields).

British American Tobacco (BTI): Yields ~8–9%, and is globally diversified (strong in Europe, Africa, and U.S. via its Reynolds American subsidiary which sells Newport, Camel, and Vuse e-cigs). BAT’s advantage is geographic breadth and some successful new categories (Vuse is #1 in U.S. vaping, glo has ~20% share in Japan’s heated tobacco market). However, BAT is burdened by high debt from its 2017 Reynolds acquisition and has had to slow dividend growth to focus on deleveraging. Its earnings have grown modestly (helped by cost cuts and pricing), but not at PMI’s pace. Regulation-wise, BAT faces EU menthol bans (already in effect) and other international nuances. BAT’s new CEO (Tadeu Marroco) in 2023 refocused on efficiency and possibly separating its U.S. business. BAT is a bit of a hybrid: it has a foot in both worlds (combustibles and new products), but it isn’t leading in heated tobacco (IQOS eclipses glo) and its vape segment, while growing, isn’t as profitable yet. BAT’s dividend is high but in GBP terms it’s been flat (they target 65% payout). Many U.S. investors also face UK withholding tax on BAT’s dividend (though can often reclaim part via tax credit). BAT trades around ~7× forward earnings, another deep discount.

Adam’s Note: 5.4% yield.

In comparison, **PMI offers a middle-ground yield (about 3.7%) but with a much higher certainty of growth. It’s the only one of the three with rising cigarette alternatives’ revenue share (over 40% and climbinglinkedin.com). It’s also uniquely pursuing the U.S. market expansion with potentially huge payoffs.

Adam’s note: 3.55% yield

For a retiree, one might ask: why not just buy the 8% yield of MO or BTI? The answer is risk and growth. Altria’s dividend might be safe for now, but in 10 years, if U.S. smoking declines heavily without replacement, Altria could be a smaller company and might struggle to maintain the dividend (or at least it won’t grow much, possibly eroding purchasing power). BAT has growth avenues but also a heavy debt load and is subject to currency swings (its dividend in USD has fluctuated given GBP changes). PMI, yielding ~3.7%, perhaps 4% on any dip, provides strong forward earnings growth that should support 3–5% dividend growth annually. Over a decade, PMI’s dividend could be 50–60% higher than today if forecasts pan out, whereas Altria’s might be only ~20% higher (or worst-case, cut if trends worsen).

Adam’s note: Also because neither MO nor BTI yield 8%😉😂🤣

Thus, for a retiree looking at total return (income + capital preservation), PMI likely offers a better inflation hedge. The market clearly values PMI’s growth, as seen in its premium P/E (~19× vs single-digits for the others). That premium reflects sustainability – PMI’s earnings are expected to keep rising beyond 2030, while many see MO/BTI earnings flattening or declining in the long run.

In short, **PMI is the choice for those prioritizing long-term income reliability and growth, rather than just the highest initial yield. A balanced retirement portfolio might hold some of each for diversification (indeed some income funds do hold all three), but PMI can be viewed as the “core” holding you’re most confident will be thriving in 10+ years due to its smoke-free pivot.

(Refer back to Table 3 and the dividend yield chart above for a quick visual comparison of these points.)

8. Conclusion and Recommendation

Philip Morris International is arguably the gold standard of tobacco industry investments as we head into the late 2020s. By aggressively cannibalizing its own cigarette business in favor of reduced-risk products, PMI has tackled the industry’s existential challenge head-on. The results are evident in its financials (accelerating earnings, expanding margins) and its stock performance (market-beating returns in recent years). For a retiree seeking high-yield income, PMI offers an unusual combination of attributes:

Safety: The dividend is well-covered by cash flow and backed by an investment-grade balance sheet. PMI’s business is resilient even in economic downturns – nicotine demand is steady and pricing power is intact. Moreover, PMI’s geographic and product diversification, along with its prudent debt management, lower the risk of any interruption to its dividend. The company weathered the pandemic without cutting its payout and has now even reduced its exposure to extreme regulations via settlements and product mix shifts.

Growth: PMI is not resting on legacy laurels. It presents a credible growth story: IQOS expansion (especially in the U.S.) and ZYN’s continuing rise provide avenues for volume and earnings growth that can outpace inflation significantly. Double-digit EPS growth is forecast for the next 2–3 years, something almost unheard of in other consumer staple stocks of this size. This growth engine means the real income (inflation-adjusted) from PMI’s dividends can increase over time, preserving retirees’ purchasing power – a key concern for those on fixed income.

Stability: With a beta around 0.4 and a defensive business profile, PMI stock adds stability to a portfolio. It’s less sensitive to economic cycles – in fact, it can even benefit from some adverse scenarios (e.g., if economies slow and interest rates drop, PMI’s high yield becomes more attractive). The regulatory horizon is clearer now than it’s been in years, which also reduces headline volatility risk. Owning PMI is much like owning a consumer staple (like a Coca-Cola or P&G) but with a higher yield attached.

The bull case for PMI is straightforward: continued execution of the smoke-free pivot will lead to sustained earnings growth and possibly some valuation re-rating if the market gains more confidence in PMI’s long-term trajectory. There are also potential upsides like faster U.S. adoption of IQOS or a value-unlocking move (PMI could at some point spin off or list a stake in its faster-growing division, for example, to highlight value).

The bear case centers on a few uncertainties: currency could remain a headwind (if the dollar strengthens further) which might dampen reported growth; FDA approvals for IQOS ILUMA might take longer than expected, delaying U.S. revenue ramps; or perhaps competitor innovations (or a resurgence of vaping) could slow PMI’s momentum in heated tobacco. Additionally, if global macroeconomic issues hit emerging markets, there could be short-term volume or forex setbacks. However, none of these risks appear likely to derail the fundamental trajectory – they might cause bumps, not a collapse, in PMI’s progress.

Final Verdict: For a high-yield income investor with a medium to long-term horizon (5–10 years or more), PMI is a STRONG BUY. It earns a spot as a core holding in a retirement portfolio – one might consider a 3–5% allocation to PMI within an equity income sleeve. The stock offers a “best of both worlds” profile: a dividend yield comfortably above market averages and bonds, plus the prospect of dividend growth that can outpace inflation. By reinvesting dividends (if not needing the income immediately), an investor can compound their position as PMI’s smoke-free growth story unfolds.

We recommend PMI as a foundational “Sleep Well At Night” stock for retirees. It provides the income reliability of a utility stock but with the growth potential more akin to a healthcare or tech company (given IQOS and ZYN’s tech-driven growth) – a rare combination. As always, position sizing should consider one’s overall diversification and risk tolerance. But within the tobacco/high-yield space, PMI stands head and shoulders above in terms of long-term viability.

In conclusion, PMI’s transition and solid execution have fortified its dividend for decades to come, making it a compelling choice for those who need income now and in the future. Its lower volatility and reduced regulatory overhang further enhance its appeal for conservative investors. We expect PMI to continue delivering dividend increases and steady returns, rewarding shareholders who are patient and focus on the company’s big-picture transformation.

Disclosure: This report is for informational purposes and not personal financial advice. All investors should conduct their own due diligence and consider their individual objectives. The analyst does not own PMI stock at the time of writing.

Adam’s note: PM appears to be a VERY good fit for Ultra ZEUS 2026 (and probably 2027 when we don’t have to focus so much on minimizing downside capture).