Something unusual happened in the final days of January. While retail traders watched KLAC crater 15% and AMD drop 6% in a single session, a handful of boring telecom stocks staged their largest rally in nearly a year. VZ surged nearly 12% in three days. T jumped over 4%. The S&P Telecomm Services Index recovered nearly half of its entire decline from last fall in just 72 hours.

This is the market whispering something important: the rules are changing.

The Shot Across the Bow

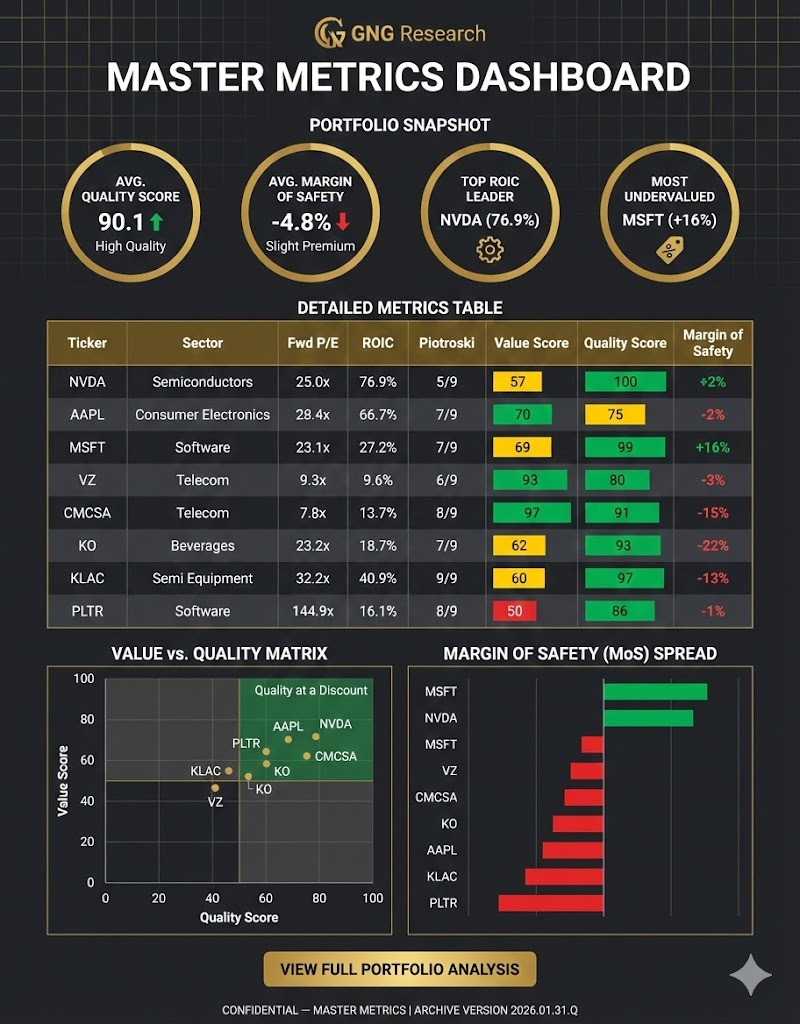

Friday's semiconductor bloodbath wasn't random. KLAC, AMD, LRCX, and AMAT all dropped more than 5% in a single session. To put this in context: these aren't speculative meme stocks. KLAC carries a Piotroski F-Score of 9, the highest possible reading for financial strength. LRCX posts a 40.8% return on invested capital (ROIC). AMAT sits near 52-week highs with a Quality Score of 97.

These are quality names getting sold hard. That's the warning sign.

The Vulcan database shows the divergence clearly. LRCX trades 80% above its 200-day moving average after nearly doubling from April lows. AMAT sits 53% above its 200-day. When names this extended start correcting violently, the rotation has begun.

Where the Money Is Going

While tech gets hammered, defensive sectors are quietly breaking out. KO just pushed to new all-time highs, trading 6% above its 52-week high. This isn't a company known for explosive growth. Coca-Cola posts 7.6% five-year sales growth and an 18.7% ROIC. But it carries a Piotroski score of 7, yields 2.7%, and sits in the 78th percentile for cash flow predictability.

The telecom story is even more striking. After eleven months of sideways action, VZ, T, TMUS, and CMCSA exploded higher in the final week of January. The Vulcan data reveals why institutions are accumulating:

VZ yields 6.1% with a forward P/E of just 9.3. That's less than half the S&P 500's multiple. Value Score: 93rd percentile. CMCSA trades at 7.8x forward earnings with a 97th percentile Value Score and a Piotroski of 8. T yields 4.2% at 10.3x forward earnings, scoring 89 on Value and 95 on Sentiment.

When quality tech is selling off and deep-value telecoms are breaking out simultaneously, the market is broadcasting a message about what comes next.

The Counterintuitive Setup

Here's what makes this rotation particularly interesting: the broad market isn't breaking down. The S&P 500 closed January with two straight days of late-day strength, recovering well off morning lows. NVDA and AAPL combined represent over 15% of the index, and both remain technically bullish.

GNG Research expects SPX to push above 7,000 in early February and potentially reach 7,150 to 7,200. This isn't a call to run for the hills. It's a call for vigilance about what's working and what isn't.

The math supports continued upside near-term. NVDA carries a 76.9% ROIC with an Altman Z-Score of 71.5, suggesting essentially zero bankruptcy risk. AAPL posts 66.7% ROIC with a 99th percentile Cash Flow Predictability score. These mega-caps can support the indexes even as rotation churns beneath the surface.

But the defensive shift that began in mid-2025 with Healthcare and Utilities has now spread to Consumer Staples and REITs. When Staples outperform Discretionary with equities near all-time highs, history suggests caution is warranted.

The Software Warning

The damage in software deserves special attention. PLTR pulled back to the $142 to $148 zone that coincides with both November 2025 and August 2025 lows. The Vulcan database shows PLTR trading at 144.9x forward earnings with a Margin of Safety of negative 1%, suggesting no valuation cushion at current prices.

The chart pattern is concerning. What may be forming is a massive head-and-shoulders formation. A bounce to $166 to $170 looks likely initially, but a push back to all-time highs appears increasingly unlikely given the technical deterioration.

MSFT presents a different picture. At 23.1x forward earnings with 27.2% ROIC, a Piotroski of 7, and Quality/Growth Scores of 99, Microsoft remains fundamentally superior. But even MSFT sits 22% below its July 2025 highs, suggesting the software selloff isn't discriminating.

The IGV Software ETF approaches intermediate-term support from 2022 lows. This may cushion the decline temporarily. But GNG Research is skeptical that software bounces for more than three to four weeks before weakening further from March into May.

Semiconductors: The Final Dance

The semiconductor story remains the most nuanced. The VanEck Semiconductor ETF (SMH) maintains bullish trends with MACD momentum at higher levels than last fall. GNG expects SMH to rally toward $420 to $425 in the near term.

But weekly DeMark signals suggest a possible TD Combo "13 Countdown" sell signal forming within two weeks. This coincides with monthly signals at the start of February. When multiple timeframes align on exhaustion signals, even bullish trends deserve respect.

The Vulcan data shows why selectivity matters:

NVDA trades at 25x forward earnings with 77% ROIC. That's expensive but justified by exceptional profitability.

AMD trades at 35.9x forward with just 5.3% ROIC. The valuation assumes significant improvement that hasn't materialized.

KLAC posts 40.9% ROIC with a perfect Piotroski of 9 but trades 13% below fair value despite the selloff.

Quality divergence within tech suggests a barbell approach: own the highest-quality names while trimming extended positions with weaker fundamentals.

The Playbook for February

For investors with three-to-five month time horizons, bounces in software and semiconductors over the next few weeks may provide opportunities to diversify away from these groups.

The defensive rotation into Healthcare, Utilities, Consumer Staples, REITs, and now Telecommunications represents institutional repositioning for a potential late February or early March equity peak. This doesn't mean selling everything. It means adjusting allocations.

Consider accumulating quality telecoms on any pullback from the current surge. VZ and CMCSA offer compelling yield with strong quality metrics. KO provides defensive exposure with proven dividend growth.

For tech exposure, favor NVDA, AAPL, and MSFT over speculative software. These mega-caps have the balance sheets and profitability to weather rotation.

Watch Financials, Industrials, and Consumer Discretionary for stabilization. If these groups fail to bounce while defensives continue leading, the rotation signal strengthens.

What Could Go Wrong

Five specific risks warrant monitoring:

First, if PLTR breaks below $142 support convincingly, software could cascade lower faster than expected.

Second, semiconductor earnings in the coming weeks could disappoint given supply chain constraints and AI capex deceleration concerns.

Third, the Dollar spike from Warsh's Fed Chair nomination, though likely short-lived, could pressure international earnings and commodity-sensitive sectors.

Fourth, if breadth fails to improve and only mega-cap tech supports the indexes, any weakness in NVDA or AAPL could trigger outsized index declines.

Fifth, the defensive outperformance could be a head-fake if growth data surprises to the upside, making current telecom accumulation poorly timed.

The Bottom Line

The market isn't crashing. But it is rotating. The carnage in metals, software, and parts of tech last week represents a warning, not a signal to panic. Trends remain bullish into February, with SPX likely to make new highs early in the month.

Yet the persistent strength in defensive sectors while growth sectors churn tells us institutional money is repositioning. When Consumer Staples outperform Consumer Discretionary at all-time highs, when telecoms rally 12% in three days after eleven months of nothing, when high-quality semiconductors drop 15% on no news, the smart money is preparing for something.

The question isn't whether to act. It's whether to act now or after the next bounce. For those with a three-to-five month horizon, using strength in February to trim extended positions and add defensive exposure seems prudent.

The rotation has begun. The only question is how far it runs.

Data sourced from Vulcan-MK5 Unified Database. Updated January 31, 2026.