The Two-Screen Setup: How We Found These Five

I run thousands of stocks through systematic filters every month. Most get eliminated quickly. But when two independent screens flag the same thesis, that's when I pay attention.

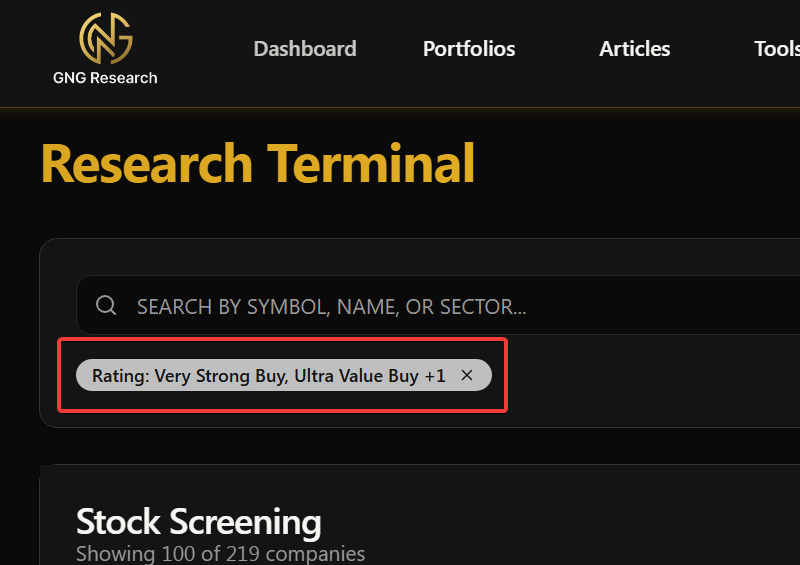

Here's what happened this time. Screen one: I ran our entire 5,500+ stock universe through the GNG Research Terminal's Buy ranking filter. The terminal crunches 170+ metrics across quality, value, growth, momentum, and safety. Only a 219 stockssurvive with a Strong Buy or better Filter. To do this yourself go to research terminal , then click Filters, Select “GNG Scoring” category and then the Rating metric select the ratings you wish to filter for.

Screen two: I overlaid Vulcan's five-pillar quant model on stocks hitting 52-week lows recently, looking for names where the market overreacted to short-term noise.

The intersection? Five companies that passed both tests. Four came directly from the Strong Buy+ screen (ADBE, LRN, DDI, NVO). These also surfaced from the 52-week low contrarian scan with strong Vulcan scores plus PFE.

What does Vulcan actually measure? Five pillars: Quality (profitability, moat durability, and management execution), Value (P/E, FCF yield, margin of safety to fair value), Growth (revenue trajectory, earnings expansion, Rule of 40), Safety (balance sheet strength, interest coverage, Altman Z-Score), and Momentum (relative price performance versus sector and index). A stock needs to score well across multiple pillars to qualify. Missing one isn't fatal, but missing two usually is.

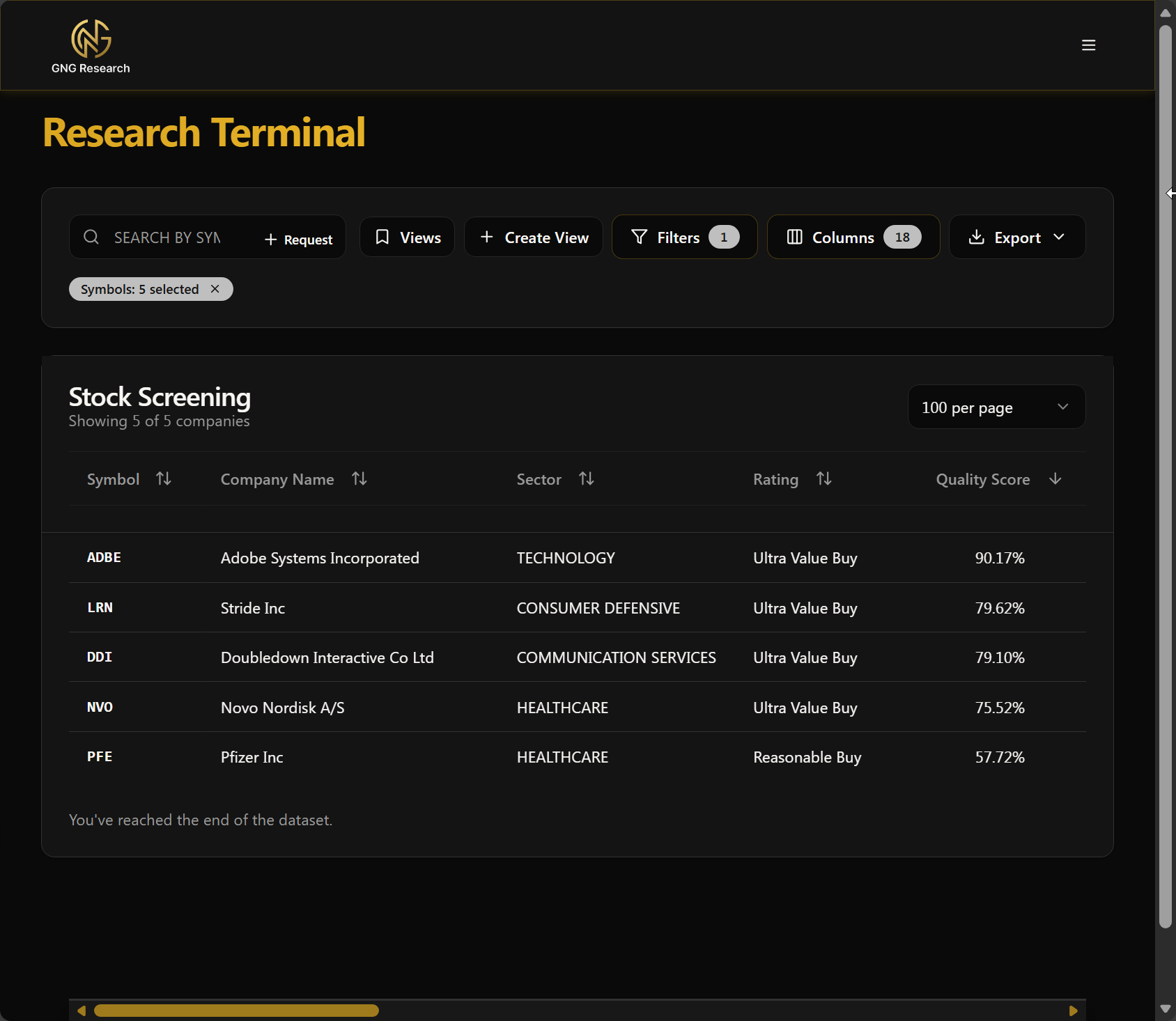

These five made the cut. Let me walk through each one. See the 2nd image here showing me filtering under Filters | Basic Info | Symbols where I added these 5 tickers.

Stride, Inc. (LRN): The Online Education Play Trading at 8x Earnings

What the Business Does

Stride operates virtual K-12 schools and career training programs across the United States. If you've heard of online charter schools, Stride runs them. They provide curriculum, technology platforms, and support services to students learning from home. The company also runs a fast-growing career learning segment teaching vocational skills to adults looking to reskill.

Why It Made the List

LRN surfaced from the GNG Ultra Value Buy screen. An 8.7x trailing P/E on a company growing revenue 18% annually caught our attention. The stock dropped 54% in a single day after disclosing 10,000-15,000 fewer enrollments than expected, platform implementation issues, and higher withdrawal rates. A federal securities lawsuit followed, alleging more serious issues including inflated enrollment via "ghost students" and compliance violations. The valuation reflects real risk now, not just post-COVID skepticism. Whether current prices adequately discount a worst-case outcome depends on how the lawsuit and any regulatory response unfold.

The Core Thesis

Stride represents a mean-reversion opportunity hiding in plain sight. Online education wasn't a pandemic fad. It was an acceleration of an existing trend. Families discovered flexibility. School districts discovered cost savings. Stride's enrollment keeps climbing because the value proposition works.

Here's what most investors miss: Stride's Career Learning segment grew over 60% recently. That's not K-12 enrollment fluctuations. That's adults paying for workforce reskilling as AI reshapes job requirements. This business has a decade-long runway.

The recent platform glitch that tanked the stock? Fixed. Management announced a $500M share buyback with the cash pile they've accumulated. When insiders buy aggressively after a selloff, pay attention.

Valuation Context

At roughly $68 per share, LRN trades at 8.7x trailing earnings and 1.3x sales. The forward P/E jumps to around 17x due to a temporary earnings dip, but that's still cheap for this growth profile. Price to free cash flow sits near 10x, implying a 10% FCF yield. One analysis pegged the stock at nearly 80% below intrinsic value. The average analyst target exceeds $130, with Morgan Stanley's recent cut to $95 still representing 40% upside from current levels.

Quality and Moat

Stride's moat comes from switching costs and scale. Once a school district partners with Stride and teachers learn the platform, switching mid-year creates chaos. The curriculum integration takes time. That stickiness creates recurring revenue.

The Career Learning segment adds another dimension. Corporate partnerships for workforce training represent multi-year contracts with enterprise customers. This isn't a one-off tutoring transaction.

Piotroski F-Score runs high, indicating improving fundamentals. The Altman Z-Score sits comfortably above distress levels. Gross margins hold around 36%, with operating margins in the mid-single digits leaving room for expansion as the platform scales.

Financial Health and Cash Flow

The balance sheet provides some cushion here. Net debt to EBITDA runs at 0.13x, essentially net cash. The company generated over $370M in free cash flow in 2025 and holds over $1B in cash, more than total debt. That financial flexibility matters now - potential settlement costs, regulatory fines, or revenue hits from lost state contracts would draw on this buffer. The $500M buyback announced before the October collapse signals management confidence, though executing buybacks while facing securities litigation raises capital allocation questions.

That cash hoard enabled the $500M buyback. Interest coverage is extremely high. Current ratio exceeds 2x. There's virtually no financial stress here, which matters because education funding can be politically volatile.

Growth Drivers

Near-term: Career Learning expansion continues with 60%+ growth rates. Enrollment in K-12 programs grows at double digits as more families choose virtual options.

Two to three years out: Management expects high-single to double-digit revenue growth with operating leverage improving margins. The workforce reskilling tailwind from AI disruption hasn't even peaked yet.

Key Risks and What Would Change My Mind

Regulatory risk tops the list. Virtual charter schools depend on state approvals and funding formulas that politicians can change. A major state pulling funding would hurt.

Competition from non-profits and established players like Pearson could intensify. If Stride loses market share despite favorable tailwinds, the thesis weakens.

Another platform outage would damage credibility with school districts. Technology execution matters here.

If career learning growth decelerates below 30% for two consecutive quarters, I'd reassess the growth runway assumptions.

Action Framing

LRN moves to a "watch and wait" stance given the pending securities lawsuit and compliance allegations. The 8x P/E reflects real uncertainty, not just market overreaction. Before initiating a position, I'd want to see: (1) Q2 retention data showing the enrollment issues are contained, (2) clarity on how state regulators respond to the alleged compliance violations, and (3) any settlement framework emerging from the lawsuit. If those clear favorably, the risk/reward improves significantly at current prices. If compliance issues prove systemic or state contracts get pulled, the thesis breaks regardless of valuation. Position sizing would be 0.5-1% max for risk-tolerant investors, not a core holding.

DoubleDown Interactive (DDI): The Cash-Rich Casino Stock Trading Below Net Cash

What the Business Does

DoubleDown develops social casino games, the free-to-play mobile apps where users play slots and poker for virtual chips. Players pay real money for more chips when they run out. The company also acquired SuprNation, a real-money online casino operator in Europe, expanding beyond social gaming.

Why It Made the List

DDI hit the Ultra Value Buy screen because the numbers are almost absurd. The stock trades at roughly 3.9x earnings. Net cash on the balance sheet equals approximately $9 per share, while the stock trades around $8.90. You're essentially getting the operating business for free.

The Core Thesis

DoubleDown is a classic "cigar butt" deep value play, but with actual catalysts. The social casino business is mature but prints cash like a government mint, generating nearly 40% operating margins. The recent acquisitions in European iGaming inject growth optionality.

The market prices DDI for terminal decline. But Q3 2025 revenue grew 15.5% year-over-year. SuprNation's revenue surged 108% in Q3. These aren't the numbers of a dying business.

Here's the key insight: management has $404M in net cash sitting on the balance sheet. They can acquire more studios, buy back shares, or simply wait while cash accumulates faster than the market cap. The risk-reward skews dramatically positive.

Valuation Context

The numbers border on unprecedented for a profitable company. P/E sits at 3.9x. EV/EBITDA runs around 0.58x, meaning enterprise value is essentially zero relative to earnings power. Price to free cash flow clocks in at 3.1x, representing a 32% FCF yield.

One analysis found DDI offers roughly $26 of value for every $1 invested, calling it one of the widest margins of safety in their entire database. A DCF model from SimplyWall.St suggests 77% undervaluation with fair value around $38.

For context, similar gaming companies trade at mid-teens P/E ratios and EV/EBITDA multiples 20-40x higher than DDI.

Quality and Moat

The social casino business operates with excellent unit economics: 70% gross margins, 39% operating margins, 32% net margins. DDI's legacy games like DoubleDown Casino have long lifespans with loyal user bases who've invested time and progression in the apps.

The moat isn't wide, but the installed user base creates retention. Average revenue per daily active user runs around $1.39 with 7.8% payer conversion, healthy metrics for the category.

ROIC runs approximately 10%, which actually understates profitability given the massive cash drag on the balance sheet diluting returns.

Financial Health and Cash Flow

DDI's balance sheet is a fortress. Net cash stands at $404M against a $440M market cap. Net debt to EBITDA runs at negative 2.1x, meaning cash exceeds twice annual EBITDA.

Operating cash flow for the first nine months of 2025 hit $94M, up 6.9% year-over-year. Capital expenditures are negligible, so FCF conversion runs at 99%. They generate roughly $120M+ in annual free cash flow that simply piles onto the already bloated cash position.

The Altman Z-Score indicates zero distress risk. Cash flow predictability ranks in the 82nd percentile.

Growth Drivers

Near-term: European iGaming expansion through SuprNation provides actual growth. They're entering new markets like Sweden, UK, and Germany. Revenue there grew 108% last quarter.

Management targets increasing direct-to-consumer payments above 20% of social casino revenue to bypass Apple and Google's 30% platform fees. That margin improvement flows straight to the bottom line.

Longer-term: Management has "appetite" for more acquisitions. With $400M+ in cash, they can buy growth if organic doesn't materialize.

Key Risks and What Would Change My Mind

Structural decline in social casino remains the primary risk. If core revenue falls more than 10% annually for multiple quarters, the cheap valuation becomes a value trap.

The $415M class-action settlement resolved in 2023 highlighted legal risk in social gaming. Regulatory challenges could resurface in other jurisdictions.

DoubleU Games, a South Korean firm, holds majority ownership. Their strategic priorities might not align with minority shareholders. Capital allocation could favor acquisitions over shareholder returns.

Competition from newer mobile games could steal market share. User engagement metrics need monitoring.

If management doesn't deploy the cash productively within 24 months, whether through buybacks, dividends, or accretive acquisitions, I'd question capital allocation.

Action Framing

DDI is a speculative deep value position, not a core holding. At current prices, you're essentially buying the European iGaming optionality for free while getting paid to wait via the cash-generating social casino business.

I'd limit position size to 0.5-1% given small-cap volatility and liquidity constraints. Buy in thirds at current prices, below $8, and below $7. Below $6 with no fundamental deterioration would warrant backing up the truck. No stop-loss on this one since the downside is already priced in, but set a 36-month patience window for the thesis to play out.

Pfizer Inc. (PFE): The Pharma Giant Trading Like It's Dying

What the Business Does

Pfizer needs no introduction. It's one of the world's largest pharmaceutical companies, known for everything from the COVID-19 vaccine to blood thinners like Eliquis, vaccines like Prevnar, and a deep oncology portfolio. They employ massive R&D resources and have global manufacturing and distribution at scale.

Why It Made the List

PFE hit the Vulcan screen because the market is treating Pfizer like a company in permanent decline. The stock yields 6.75% currently, trades at roughly 13x forward earnings, and sits more than 40% below 2021 highs. That's not what a dying company looks like on fundamentals. That's what fear looks like on a price chart.

The Core Thesis

Pfizer faces a transition year in 2024-2025 as COVID revenue evaporates. That's real and priced in. What's not priced in: Pfizer spent $70B on strategic acquisitions including Seagen for oncology and Arena for immunology. The pipeline includes oral obesity drugs, next-generation cancer therapies, RSV vaccines, and gene therapies.

The company isn't sitting still. They're aggressively rebuilding for the next growth phase. By 2026-2027, new product launches should replace lost COVID revenue and then some. Management targets $25B in revenue from new products by 2030.

Meanwhile, shareholders collect a 5.5-6% dividend yield from a company with investment-grade credit and strong free cash flow. You're paid to wait.

Valuation Context

Pfizer's forward P/E sits around 13-14x, well below its historical 15-20x range and the pharma industry median. The dividend yield at roughly 6.75% is near multi-decade highs for the company.

Morningstar's fair value estimate is $38, implying substantial discount to intrinsic worth. DCF analyses suggest 58-63% undervaluation. Analysts' consensus target in the mid-$30s implies 20-30% upside from current levels around $26.

Price to sales runs about 2.2x forward revenue, cheap for a pharma with Pfizer's margins and scale. EV/EBITDA of 8-9x undercuts peers like Merck and J&J.

Quality and Moat

Pfizer's moat comes from patents, scale, and trust. The IP portfolio protects products for years. The global manufacturing footprint and regulatory expertise create barriers that smaller companies can't match. The brand reputation matters in healthcare.

Operating margins historically run 25-30%+ on core pharma. The current dip reflects COVID normalization, not structural impairment. ROE and ROIC remain strong when adjusted for the transition period.

The Seagen acquisition brings cutting-edge ADC (antibody-drug conjugate) cancer therapies. These are the next generation of targeted oncology treatments. If even a portion of the pipeline succeeds, Pfizer's quality story improves materially.

Financial Health and Cash Flow

Pfizer took on debt for acquisitions, with long-term debt around $60B. But cash stands at $20B+, and net debt to EBITDA remains very manageable. Interest coverage stays high, and credit ratings remain investment-grade.

Even in a down year, FCF should exceed $10B. The dividend is well-covered by cash flow. The payout ratio will temporarily elevate as earnings trough, but it should normalize below 50% by 2026.

Management stated the dividend is a priority. They've paid and grown it for decades. The balance sheet supports continued shareholder returns even through the transition.

Growth Drivers

Near-term: Cost cuts of $3.5B should improve margins. New launches including RSV vaccines provide revenue. Pipeline milestones create potential catalysts.

Medium-term: Oncology growth from Seagen acquisition products like Padcev and Tukysa combos. Oral GLP-1 obesity drugs (danuglipron, lotiglipron) could tap the enormous weight-loss market if trials succeed. Gene therapies and rare disease drugs from various acquisitions add optionality.

Management's $25B new product revenue target by 2030 represents significant growth versus current levels.

Key Risks and What Would Change My Mind

Pipeline execution is the critical risk. Big pharma pipelines have high attrition rates. If multiple programs fail trials or face unexpected safety issues, growth targets become unrealistic.

Competition intensifies in key areas. Eli Lilly leads in obesity with Mounjaro. Moderna competes in vaccines. Numerous biotechs target the same oncology indications. Pfizer might not win its share.

The Inflation Reduction Act enables Medicare price negotiations on top-selling drugs. Some Pfizer products will qualify later this decade, potentially shrinking US revenue.

If 2025 EPS misses estimates by more than 15%, or if two major pipeline candidates fail in the next 18 months, the turnaround thesis needs reassessment.

Action Framing

PFE suits income-oriented investors willing to hold through a transition period. Current prices offer attractive entry for a 2-3% allocation.

I'd buy half now and add below $24 if the market provides opportunity. Collect the 5.5%+ dividend while waiting for pipeline execution to validate the thesis. Review thesis after each major pipeline readout. Below $22 with no change in fundamentals becomes aggressive accumulation territory.

Adobe Inc. (ADBE): The Creative Software Monopoly Trading at Decade-Low Multiples

What the Business Does

Adobe makes the software that creative professionals live inside: Photoshop, Illustrator, Premiere, InDesign, Acrobat. If you've ever created visual content professionally, you've probably used Adobe. They also run Document Cloud (PDF and e-signatures) and Experience Cloud (enterprise marketing analytics).

Why It Made the List

ADBE surfaced from the 52-week low screen with strong Vulcan overlay scores. The stock dropped roughly 30% from 2023 highs amid fears about Figma, Canva, and AI disruption. But the financials tell a different story: record revenues, double-digit growth, and margins that most software companies dream about.

The Core Thesis

Adobe represents a world-class business trading at average-company prices. The fears are overblown. Competition from Canva targets casual users who weren't paying for Photoshop anyway. Figma targets collaborative design, a market Adobe is addressing through acquisition or internal development. And AI? Adobe is monetizing it through Firefly rather than being disrupted by it.

At roughly $335, you're buying a 14x forward earnings multiple on a company growing 11% with 36% operating margins and 41% FCF margins. That's not a premium multiple. That's a value multiple on a growth company.

Valuation Context

Adobe's current 14x forward P/E represents its lowest valuation since the early 2010s. The company traded at 30-50x earnings regularly over the past five years. EV/Sales of 5.8x is nearly half historical averages around 10x.

Free cash flow yield runs approximately 7%. PEG ratio sits around 1.0, attractive for a company of this quality. The margin of safety in our Vulcan data shows 43%, implying fair value around $590 versus the current $335.

Even conservative scenarios assuming no multiple expansion suggest 15%+ annual returns from earnings growth alone. If multiples normalize even partially, returns amplify significantly.

Quality and Moat

Adobe's moat is among the widest in software. Switching costs are enormous because the learning curve is steep, files use proprietary formats, and workflows integrate across the suite. PDF is literally the standard for digital documents, and Adobe controls it.

The subscription model transformed revenue from lumpy license sales to predictable recurring streams. Retention rates are exceptional because professionals can't easily switch mid-project.

Operating margins of 36% and net margins of 27% reflect pricing power and efficient operations. ROIC historically exceeds 20%. Piotroski F-Score indicates strong fundamentals with no accounting red flags.

Adobe's integration of generative AI through Firefly represents defensive innovation. They're adding AI features to existing products and charging for premium capabilities rather than being displaced by them.

Financial Health and Cash Flow

Adobe's balance sheet is clean. Debt/Equity runs around 0.6 with net debt to EBITDA slightly negative (net cash). They generate roughly $7B+ in annual free cash flow.

FCF as a percentage of sales exceeds 40%, extraordinary for any business. Capital requirements are minimal. That cash flow funds aggressive share buybacks that enhance EPS growth.

Altman Z-Score indicates negligible bankruptcy risk. Volatility runs moderate for a tech stock with beta around 1.0.

Growth Drivers

Core growth continues at 10-15% annually from Creative Cloud subscriber additions (especially international) and Document Cloud expansion as businesses digitize.

AI represents upside through Firefly premium features and increased engagement driving upsells. Early adoption signals suggest users embrace rather than fear Adobe's AI tools.

Experience Cloud growth provides enterprise diversification beyond creative tools.

Key Risks and What Would Change My Mind

Competition from Figma, Canva, and cheaper alternatives remains the market's primary concern. If Adobe loses measurable market share among professional users (not just casual creators), the thesis weakens.

Macro sensitivity exists since creative software subscriptions can be discretionary for freelancers during recessions.

If revenue growth falls below 8% for two consecutive quarters, or if operating margins compress below 30%, I'd reassess the quality thesis.

Action Framing

ADBE represents a high-conviction position for quality-focused portfolios. Current prices offer rare entry into a franchise at reasonable valuations.

I'd establish a full 2-3% position at current prices given the quality and valuation combination. Add on any weakness below $300. The investment thesis remains intact unless fundamentals deteriorate. This is a 3-5 year compounder at minimum.

Novo Nordisk (NVO): The Obesity Drug Leader After a 45% Haircut

What the Business Does

Novo Nordisk is a Danish pharmaceutical company dominating diabetes care and pioneering the obesity drug revolution. Their GLP-1 therapies include Ozempic for diabetes and Wegovy for weight loss, products that have become cultural phenomena beyond their medical applications.

Why It Made the List

NVO appeared on the 52-week low screen after dropping approximately 45% from peak levels. The market panicked over a profit warning and competition concerns. But the underlying business continues posting exceptional growth while now trading at reasonable multiples.

The Core Thesis

Novo Nordisk just experienced a stock correction that feels like a crisis but isn't. The profit warning came because demand so dramatically exceeds supply that Novo must invest heavily in manufacturing capacity. That's a good problem.

The obesity drug market is potentially the largest pharmaceutical opportunity in decades. Hundreds of millions of people worldwide qualify for treatment. Novo leads this market with Wegovy while maintaining diabetes dominance with Ozempic. The selloff creates an entry point into a secular growth story.

Valuation Context

At current prices around $56, NVO trades at roughly 16x trailing earnings and 14x forward. For a company that just grew earnings over 30% and maintains 40%+ operating margins, that's remarkably cheap.

During the run-up, NVO traded above 25-30x earnings. The correction brings multiples down to levels typically reserved for slow-growth pharma, not category leaders in a multi-decade growth market.

Dividend yield sits at 2.86% currently, attractive for a growth company. DCF models suggest 60-69% undervaluation at current prices. Forbes recently published analysis suggesting fair value near $100.

Quality and Moat

Novo's moat in diabetes is wide and deep. They've manufactured insulin for nearly a century, building expertise and scale that competitors struggle to match. Brand trust among patients and physicians creates retention.

In obesity, Novo essentially created the medical treatment market for weight loss. Wegovy's first-mover advantage built brand recognition beyond typical pharma awareness. Patients ask for it by name.

Operating margins exceed 42%, among the highest in pharma. Net margins top 30%. ROE often exceeds 70% due to efficient capital use. These are exceptional quality metrics.

The pipeline includes next-generation products like CagriSema (combination therapy) and oral semaglutide formulations that could expand the addressable market further.

Financial Health and Cash Flow

Novo's balance sheet is pristine. Net debt to EBITDA runs approximately 0.4x, minimal leverage for a company this profitable. They fund expansion from cash flow without straining the balance sheet.

Free cash flow generation is strong even while investing heavily in manufacturing capacity. The company returns roughly 50%+ of net income to shareholders through dividends and buybacks.

The Altman Z-Score indicates zero distress risk. Vulcan's Safety Score for NVO hit 100, as good as it gets.

Growth Drivers

Near-term: Wegovy geographic expansion continues with recent UK approval and additional markets forthcoming. Supply capacity increases enable fuller marketing efforts.

Medium-term: Oral formulations could dramatically expand the patient population to those uncomfortable with injections. Next-generation combination therapies may offer even better efficacy.

Longer-term: Obesity prevalence continues rising globally while penetration of medical treatment remains in single digits. The addressable market grows faster than Novo can serve it currently.

Key Risks and What Would Change My Mind

Competition from Eli Lilly's tirzepatide (Mounjaro/Zepbound) represents the primary threat. Lilly's drug showed even greater weight loss in trials. If Lilly captures dominant share in obesity, Novo's growth trajectory slows.

Manufacturing execution matters enormously. Delays in capacity expansion mean lost revenue and market share to competitors who can supply.

Pricing pressure could emerge as governments and insurers grapple with covering expensive obesity drugs for mass populations.

If obesity revenue growth decelerates below 30% while Lilly accelerates beyond 50%, the competitive dynamics would concern me. Any serious safety signals discovered in ongoing studies would also trigger reassessment.

Action Framing

NVO offers a rare combination: growth leadership at value pricing with fortress financials.

Current prices warrant initiating a 2% position. Add on any weakness below $50. The stock remains volatile given recent selloff momentum, so scaling in makes sense. Time horizon should be 3+ years to capture the full obesity drug cycle.

Closing Synthesis: How to Think About These Five

These five stocks share one characteristic: the market mispriced quality businesses due to short-term concerns. But each plays a different role in a portfolio.

Deep Value Turnaround: DDI represents the most speculative play, essentially a free option on European iGaming success backed by cash that exceeds market cap. It's for investors comfortable with small-cap volatility and patient capital.

Value with Uncertainty Overhang: LRN trades at 8x earnings with genuine growth from career learning, but the federal securities lawsuit and compliance allegations create binary risk. It's a "show me" story now - if issues prove contained, the valuation is compelling. If they're systemic, the cheap multiple is justified.

Income While You Wait: PFE provides the highest yield with blue-chip stability. The thesis requires patience through the pipeline transition, but you collect 5.5%+ while waiting.

Quality at Rare Prices: ADBE represents the highest-quality business on this list trading at its lowest multiple in over a decade. It's the lowest-risk proposition for investors seeking exposure to a proven franchise.

Growth Leadership Discounted: NVO combines the strongest growth profile with exceptional margins and safety. The 45% selloff created an unusual entry into a secular winner.

If You Only Pick One or Two

For most portfolios, ADBE and PFE provide the best combination of quality, income, and risk-adjusted upside. ADBE offers compounding returns from a dominant franchise. PFE offers income plus optionality from pipeline execution.

For more aggressive allocations, pair NVO (growth leadership) with DDI (deep value asymmetry). They represent opposite ends of the risk spectrum but both offer compelling risk-reward.

LRN fits portfolios seeking underfollowed small-caps with strong fundamentals, but the pending securities lawsuit and compliance allegations warrant a "watch and wait" stance until Q2 retention data and regulatory responses clarify the risk.

All five passed rigorous systematic screening. The market will eventually recognize what the numbers already show.

This analysis reflects my research through the GNG Research Terminal. For access to the full screening methodology and 170+ metrics across 5,500+ stocks, visit the GNG Research Terminal at https://gngresearch.com/research-terminal.