In my last article, Brookfield Asset Management: 4 Reasons This Is The World's Best AI Dividend Stock, I talked about the three kinds of people who are probably tired of hearing about AI, and how I have compassion for them and want to help them achieve their goals while respecting their preferences, values, and how annoyed they might be by everyone in financial media, (including me) talking about AI.

Purely Dividend-focused investors (who don’t want to keep up with tech news).

Investors who think big tech is evil and don’t want to participate in the profits (blood money).

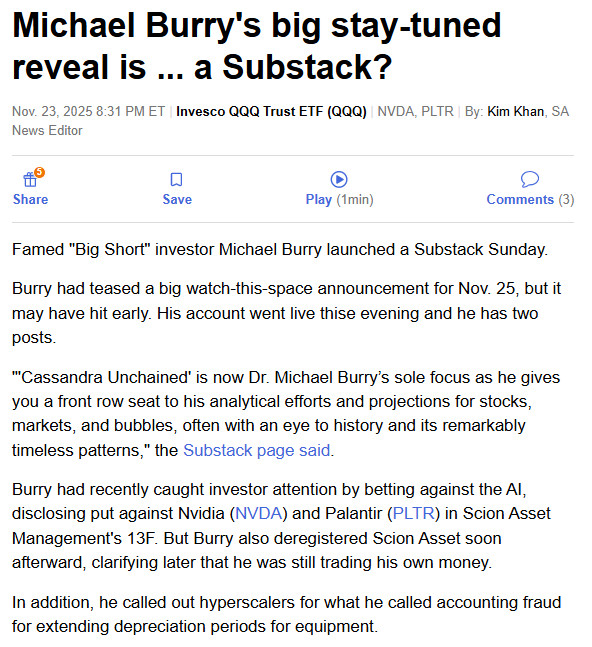

Those who believe Michael Burry’s claims that Big Tech is fraudulent and thus believe this all ends in an Enron-like meltdown.

Source: Seeking Alpha A detailed AI discussion with Warren Pies, confirming that his depreciation claims are incorrect and that Jensen Huang’s “Ampere 100 chips running Cuda are still operating at 100% utilization 6 years later” claims are correct.

His firm tracks DAILY pricing and demand data for GPUs for large companies and confirms that Burry’s claims are overblown and that they are telling their clients that Nvidia, Microsoft, and other hyperscalers are not lying about the chips being on a six-year depreciation schedule.

In other words, we have independent verification that the hyperscalers are NOT lying and that Michael Burry, AKA “Cassandra Unchained”, who has spent 16 years predicting imminent crashes, has potentially gone full Robert Kiyosaki.

OK, in fairness to Michael Burry, he has closed his hedge fund, is only running his own money, and he’s not (yet) gone full doom-and-gloom like Kyosaki. 😉 But his substack is basically saying, “I am not open to being proven wrong, subscribe to my substack if you want 100% doom and gloom about why AI is a bubble and will end in tears”.

We Know How To Track The AI Boom objectively, And If It Becomes A Bubble, I (Thanks to my experts who are much smarter than I am) will warn you.

I’m not a genius, but I do know how to find high-quality research and track first principles data to confirm an underlying thesis.

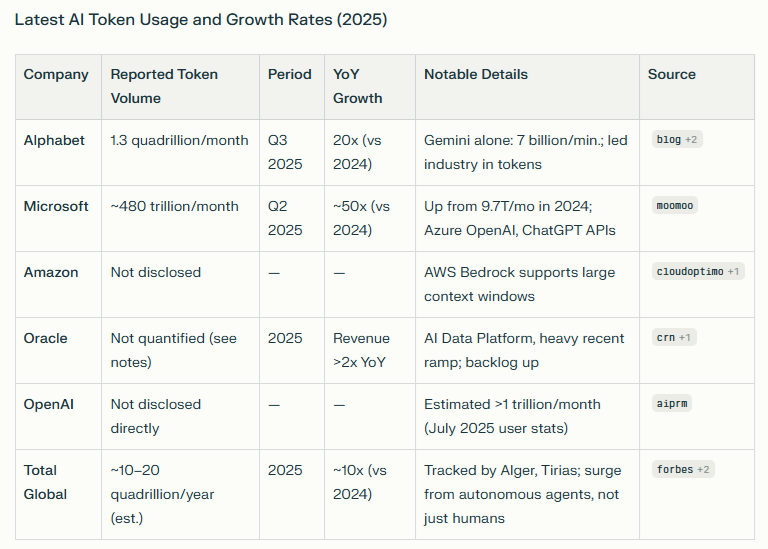

Latest AI Token Growth Data (The Ultimate Source Of Truth About Whether AI Boom Is Real)

Free cash flow is the money left over after running a business and investing in future growth. It’s Buffett’s “owner earnings” and is the gospel truth of investing. You can use accounting to hide the truth about EPS (Burry’s claim), but you can’t fake FCF.

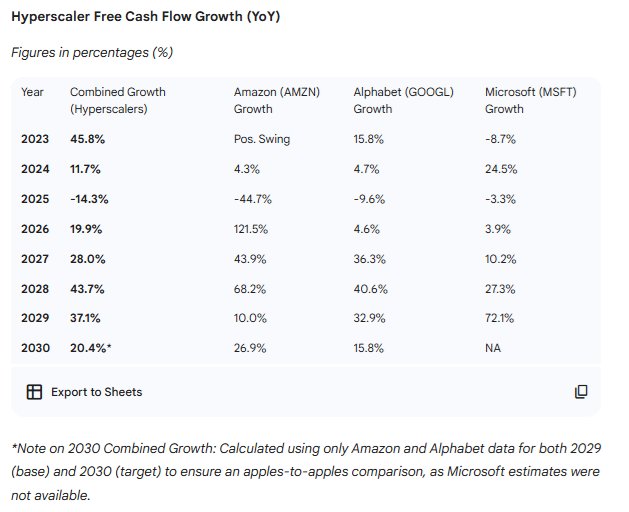

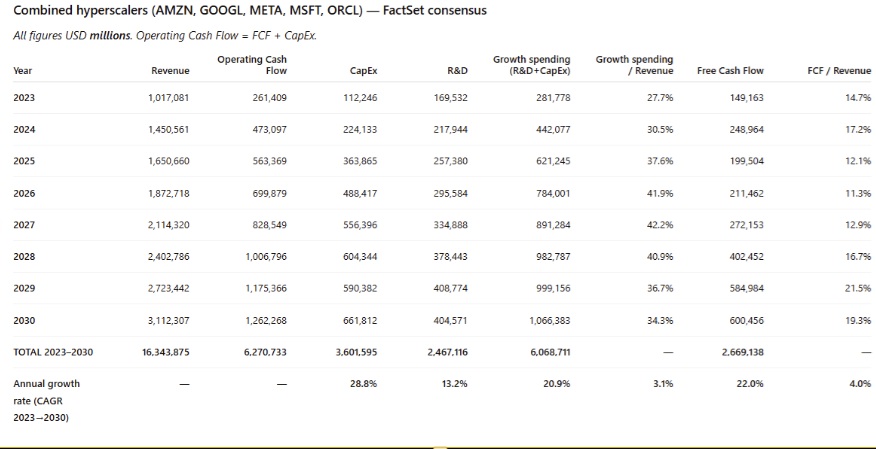

And here is the historical, consensus-free cash flow of the hyperscalers.

22% CAGR growth in FCF (23% to 24% in FCF/share) is proof that AI spending is profitable.

MSFT, GOOGL, and AMZN reported 33% to 36% YOY FCF/share growth this quarter.

If Burry was right? If there was fraud? We’d see it in the data.

Beneish M-Scores also detect accounting fraud with 82% historical accuracy… all of them show hyperscalers as having low fraud risk.

How My Family Uses ZEUS And Thinks About Money (AKA Why “Dividend Minting Magic Money Machines” Matter)😉

I was talking with my friend Tom (an AI engineer at IBM), and he said something interesting.

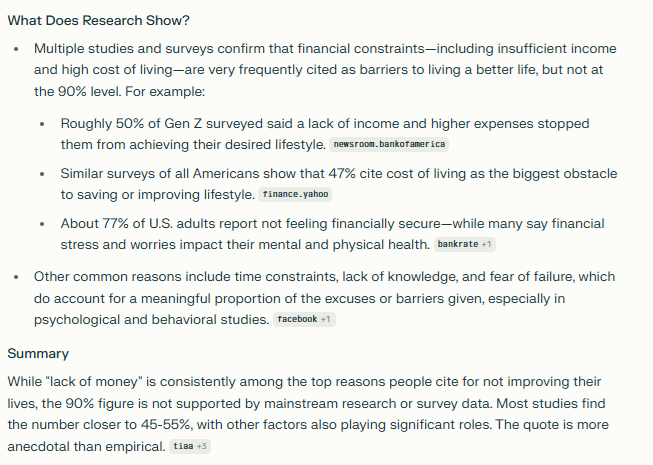

“A lack of money accounts for 90% of the excuses that people give for not living better” Thom Edmonson

While perhaps not 100% true, without question, if people had “Magic Money Machines” aka “Money Replicators,” then a lot more people would have the freedom to live better lives.

What Is A “Dividend Minting Magic Money Machine”? A Money Replicator!

In Star Trek, Replicators are machines that use energy-to-matter conversion to create anything you want. They seem like magic, but they are merely technology.

In Star Trek: Deep Space Nine, the Federation uses a really cool strategy to mine the entrance to the Wormhole to prevent the Dominion (the show's enemies) from invading.

They create mines that have replicators attached. As soon as one goes off, the mine next to it replicates another mine to replace it.

So it’s an infinite mine field, in which no matter how many enemy ships are destroyed, or how many mines are destroyed, the mine field is self-regenerating.

So this got me thinking about Nick Maggiulli’s “Basis point spending” plan, which Ritholtz Wealth Management uses to help their clients understand how to spend money sustainably.

The Basis point approach to wealth and spending is more potent than Nick Maggiulli’s “spend one basis point per day without worry” strategy. After all, if you have $1 million, one basis point is $100, so that’s really cool, but what if you have to spend more than 1 basis point?

Measure Your Life In “Babies Saved & Basis Points,” And You’ll Be A Lot Happier😉🥳

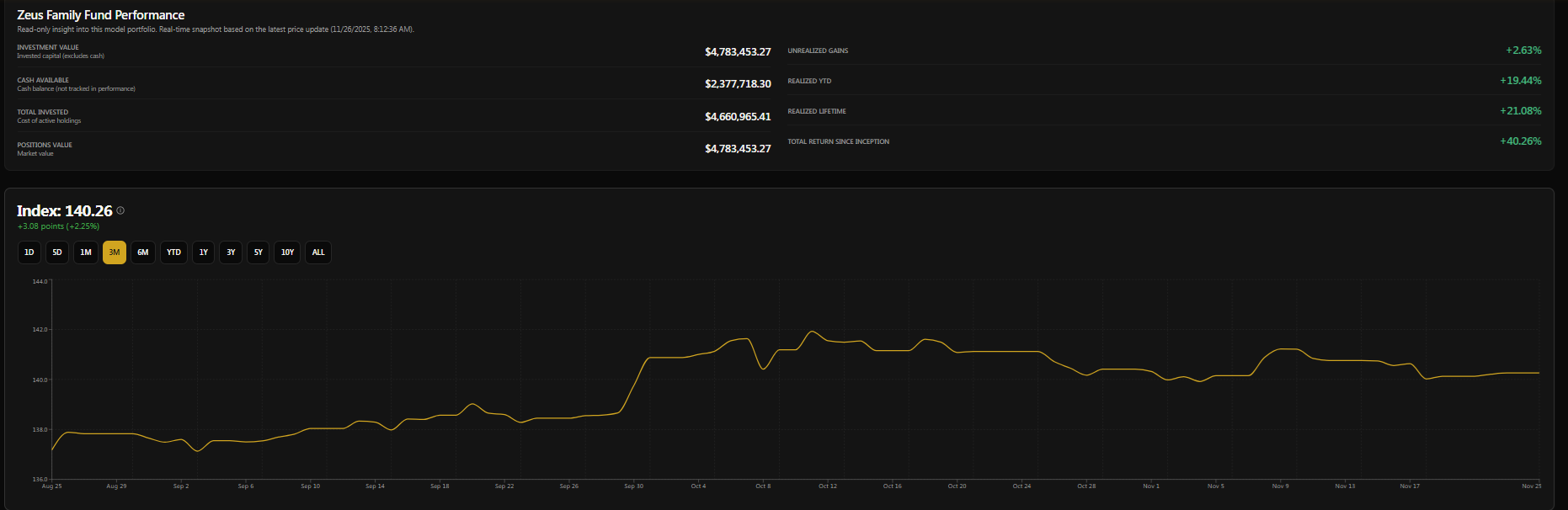

My father recently discovered that he had forgotten to hit “submit” on his company's health insurance, so for the next year, he is without coverage. The out-of-pocket expenses for his diabetes medications and three doctor’s visits are $3,600 or about seven basis points for the current ZEUS portfolio.

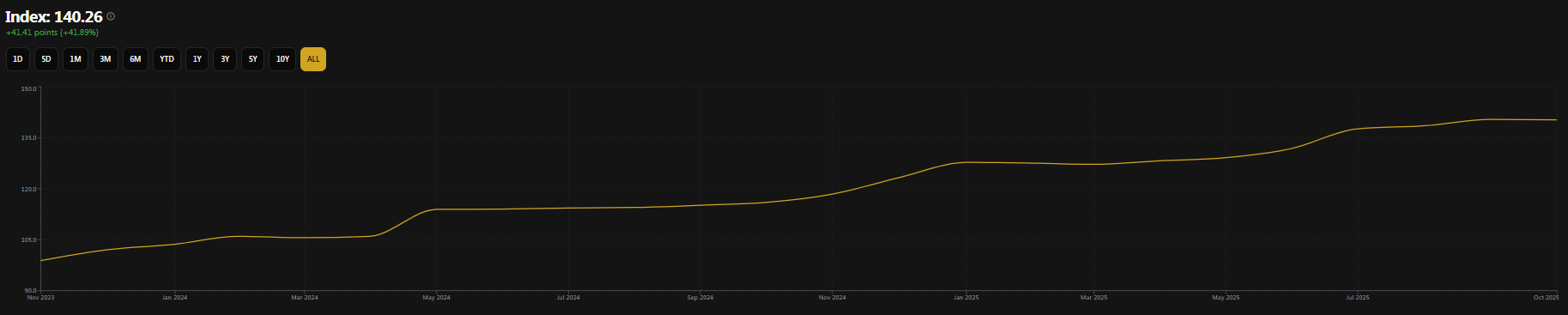

Do you see the power of “basis point” thinking? $3,600 is a lot of money! But seven basis points? That’s 0.07%. On a random day, ZEUS historically is up or down 1%.

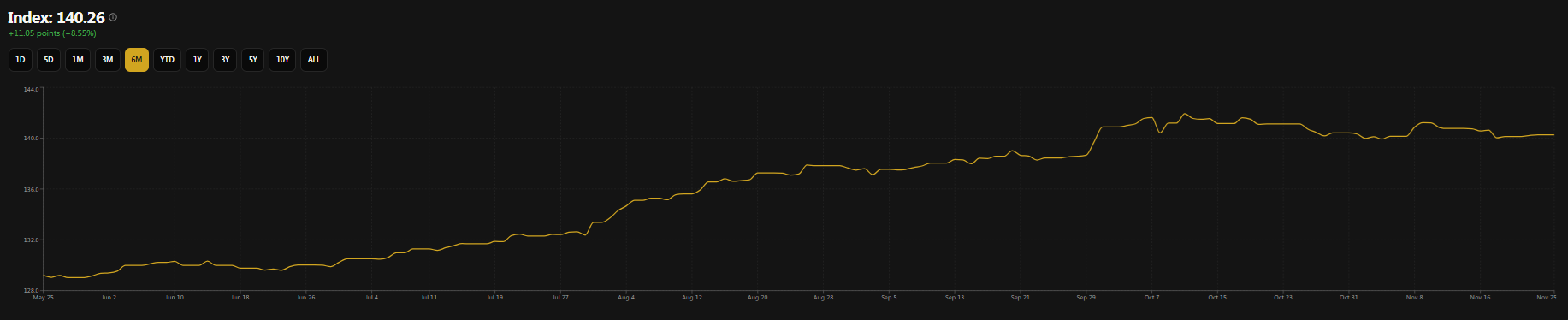

In the last 3 months, ZEUS is up 225 basis points alone (and it’s been a really crappy few weeks).

My parents' basement flooded earlier this year, and the cost? $50, and their insurance company screwed them, so it’s all out of pocket.

About 100 basis points.

In the last six months, ZEUS is up 855 basis points.

Sister’s $22,000 Wedding gift? 44 basis points. ZEUS is up 4141 basis points so far, so that gift = 1% of the profits so far.

Heck, even starting GNG Research, which costs $515,483 per year ($42,956.88 per month), represents 91 basis points per month.

69 basis points per month required to fund GNG, assuming zero revenue (for infinite sustainability).

Until we have to pay for Connor’s family's health insurance.

Starting in November 2026, it’s 81 basis points per month (assuming zero revenue).

OK, 972 basis points per year is a lot, BUT even that is doable with the right portfolio strategy.

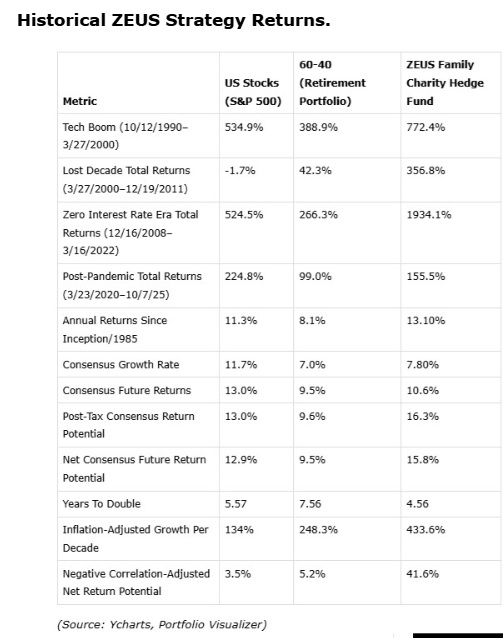

In the past year, ZEUS has been up 1676 basis points (16.76%), and historically, the strategy has done 16% post-tax.

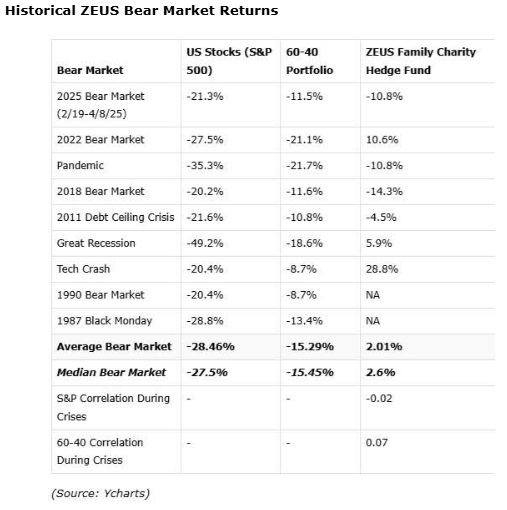

All while experiencing low drawdowns, which makes the fund an excellent “Magic money machine” where the money is really basis points and the basis points “replicate themselves” over time.

For crypto fans, imagine this. What if you had 200 bitcoin, each growing in value over time, AND the bitcoin replicated themselves?

Or owning geese that laid golden eggs. What if you bred such geese and collected their eggs?

That’s what a well-constructed portfolio is like.

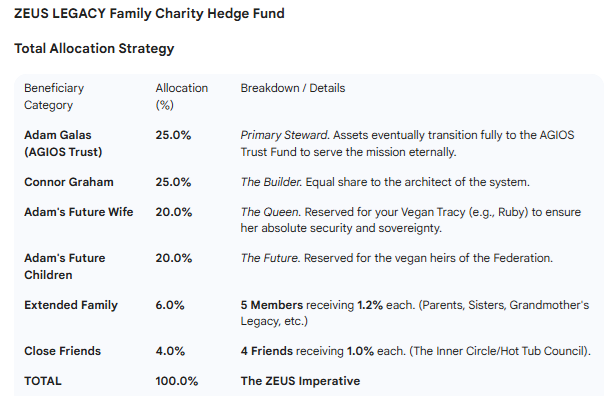

This is why I have built the ZEUS LEGACY Family charity hedge fund as a “magic money machine” that, over time, will generate so much wealth that everyone in the ZEUS family will “grow rich together” but eventually not have to care about money at all.

When the fund hits $2 billion, we cut it in half and turn $1 billion into a perpetual charitable foundation (98% tax-free compounding), but the portfolio will be run the same way.

Why this complex cap table for what’s legally 100% “my money”?

Money Is A Social Construct & Tool Created To Improve Human Lives: So Learn To Think About Money As Different Analogies

Money is a river created by society that never runs dry.

Money is a replicator.

Money is replicating Bitcoin.

Money is golden eggs from magic geese you breed

Money is the basis point of your portfolio holding company (A personal Berkshire)

Money is dividend income = “tribute from every corner of the globe for your dividend empire.”

Money is every person on earth sending you a little cash to help you live better🤗

Money will likely still exist in the future, but there will be so much of it that human obsession with cash won’t exist. At least that’s the dream that drives me in everything I do, and why I’m building “Magic money machines” for my family (and then everyone else who wants one) so that whatever money is necessary you have.

Money is a global river of wealth created by civilization (the genius of global capitalism).

If you live by this river, as long as the water is clean (the only concern), you can always drink your fill.

And thus, a scarcity mindset of “I need to hoard wealth for my family and me” disappears.

Because you can always dip your cup in the global river of wealth.

For example, when I told my mother about the preliminary plans to donate $200K to charity this year, she said, “You need to save that for a down payment on a house.”

IF my future wife (Vegan Tracy) wants a house, then we’ll get one, but the down payment isn’t something we need to hoard. It’s a single bucket we need to pull from the global river of wealth.

The money designated to charity by the AGIOS system is the rightful property of the charities that need it.

If you were a money manager for a wealthy client who gave you $10,000 in cash and told you to go down the street to a homeless shelter and donate the $10,000.

And they didn’t ask for a receipt.

And you had a $5,000 emergency car repair, could you give $5,000 and keep the rest, and tell the homeless shelter it was a $5,000 donation?

Yes, you could physically do it, but it would be theft, because the money belongs to the homeless shelter as soon as your client says to donate the funds.

That’s how the ZEUS fund operates. The allocation of resources runs on moral optimality as overseen by the council, and if the facts change (as they have with the launch of GNG and this latest correction), then the allocation of resources will change.

At this exact moment $100 in planned donations are on hold and will be redistributed in future years.

Because GNG start-up costs don’t permit the donations.

This is a “carry forward” donation that will be topped up in future years (11% of equity max donation for $1 to $10 sized ZEUS fund) because that $100K belongs to the world, not me or our company.

Basically, I think of ZEUS as “God’s money” created by the world and belonging to everyone, and AGIOS calculates the optimal way to distribute it.

I am a servant leader who is a steward of the resources that I have been granted temporary dominion over.

Because this is a lot better way to think about money and serving others than the way I used to live.

I used to be a money-obsessed bastard because “Lex Luthor doesn’t have to be a good person as long as he’s rich and respected.” 😉

It’s a lot more fulfilling to be Superman (and Super Ted Mosby in my human life) than Lex Luthor😂

OK, But What If I’m a Focused Investor Who Wants Dividends, AND I Don’t Want To Buy Brookfield, But I Want To Benefit From The AI Boom…Safely?

So what’s the point of telling you about the ZEUS “magic money machine,” which of course really runs on math.

AI-powered magic money machine is a very whimsical and fun description😉

My point about the ZEUS “Magic money machine” is that living off resources, not just income, is very powerful and useful in the future (no matter how big the AI boom becomes).

For example, take a look at the table and chart below.

Hyper Growth + High-Yield = AI-Powered Dividend Minting Magic Money Machine

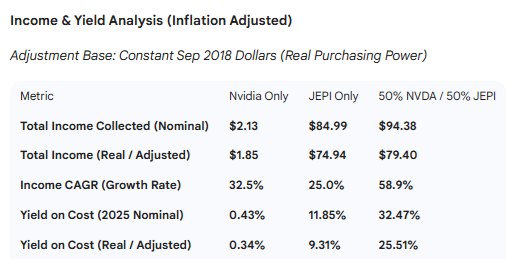

Since September 2018 (JEPIX Inception, the oldest version of JEPI)

It’s no surprise that Nvidia has been one of the best-performing stocks of the last 7 years; everyone knows that. But consider the JPMorgan Equity Premium Income fund (JEPI is the ETF, and JEPIX is the mutual fund), and both are run the same exact way.

A 50/50 portfolio of Nvidia and JEPI would have delivered incredible returns of 39%, with annual rebalancing, BUT take a look at what happens to the income stream.

Now, of course, I selected Nvidia to prove a point about how growth + yield leads to more income over time (if your time horizon is 10+ years). I’m not saying that Nvidia is the only growth stock this would work with.

How is this possible? Because of annual rebalancing.

Does This Work Outside Of The Age Of AI? Absolutely! Another Example!

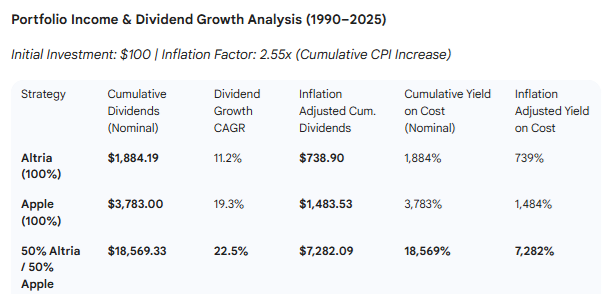

Since 1990

Altria is up about 29X in the last 35 years, while Apple is up 1122X. But look at how Apple + Altria delivered basically Apple-like returns! What is the secret?

That’s because, despite both being “risk assets”, ie, “equities”, the correlation between Apple and Altria is basically zero in any given month.

So what does this mean for dividend income over time?

$100 invested in Altria in 1990 turned into $738 inflation-adjusted dividends over 35 years.

$100 invested in Apple in 1990 turned into $1484.

And $100 invested in 50% Apple and 50% Altria, with annual rebalancing, turned into $7,282 with an inflation-adjusted yield on cost of 7282%.

THAT is the power of growth + yield investing, the barbell of growth and value, of the “Dividend Minting Magic Money Machine.”

The “Science-Based Magic” And “Math Fueled Sorcery” Behind “The Dividend Minting Magic Money Machine”

Fundamentally, stock returns are like “buying income stocks with other people’s money”.

That’s how yield + growth with annual rebalancing creates a “dividend minting magic money machine” that can harness the genius of global capitalism to create a perpetual, low-risk source of income larger than you could have ever dreamed of, to fund anything your family wants or needs.

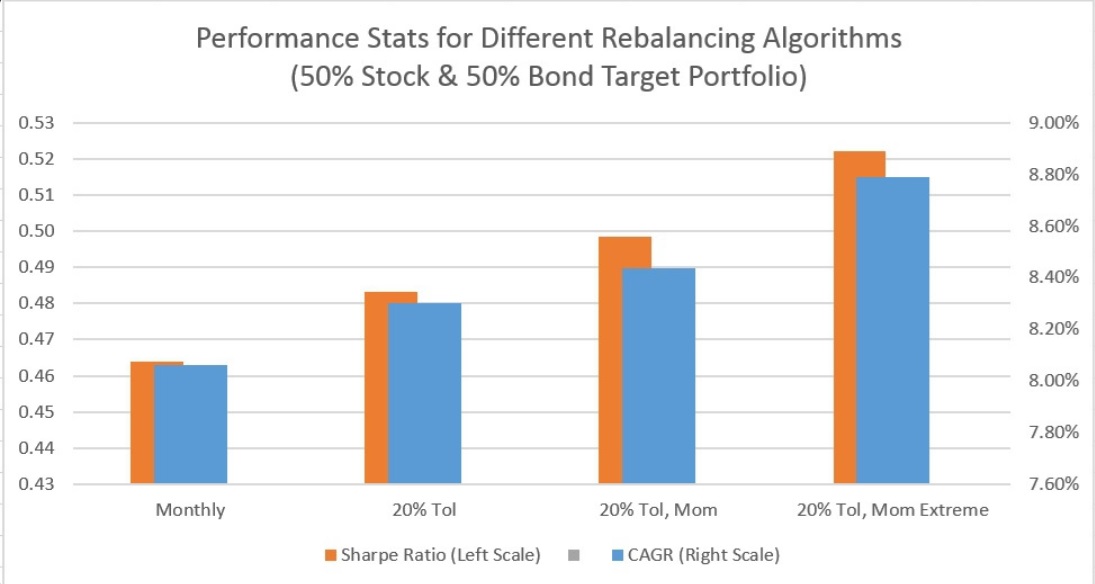

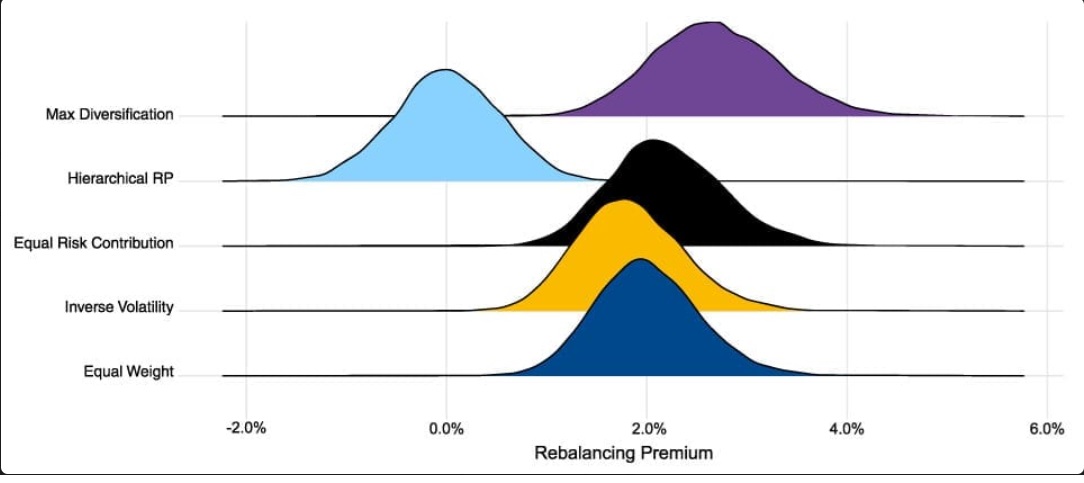

Diversification is the “only free lunch on Wall Street” because of the rebalancing premium.

In other words, non-correlated assets (like bonds, stocks, commodities, currencies, gold, crypto, ect) will go up and down at different times. Over the long term, when a hot asset becomes overvalued, it pulls forward future returns, and at annual rebalancing time, you harvest those future gains in the present.

Over the long term, by simply rebalancing non-correlated assets, you can make 2% to 3% annual “free” returns.

Even if asset prices don’t change over time, by simply recognizing that some assets become overvalued and others undervalued, you can print free money out of nothing. There is no value being created; it’s just the fact that it’s always and forever a market of assets, not an asset market.

That’s as close to a “magic money machine” as you can actually get in the real world. 😉

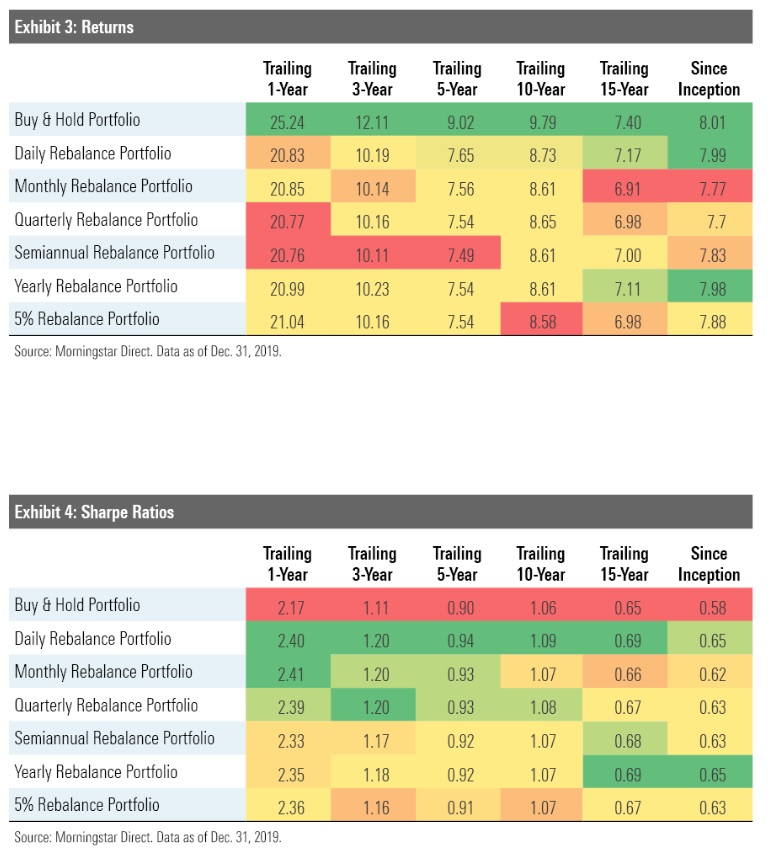

There are many ways to rebalance, ranging from rebalancing whenever your asset allocation reaches a certain threshold (the 5% rebalance range) to daily, monthly, quarterly, or annually.

Factoring in convenience and taxes, the annual option is optimal for most portfolios.

That’s intuitive because we know that stock bubbles can last 5 to 7 years.

Bear markets and bubbles last longer than most investors have patience for, which is why value investing never stopped working (as long as you measured it correctly, using FCF yield or relative valuation).

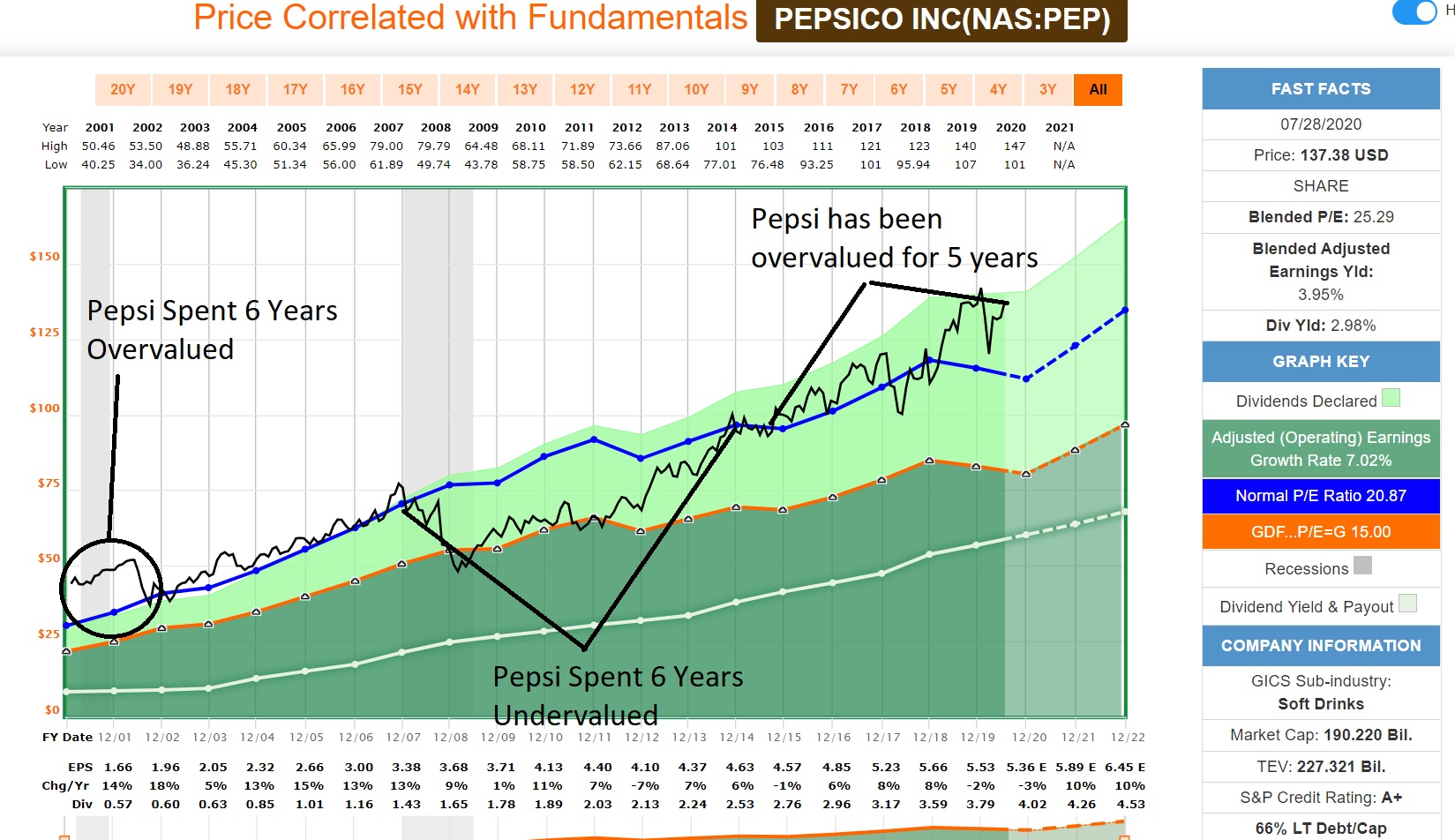

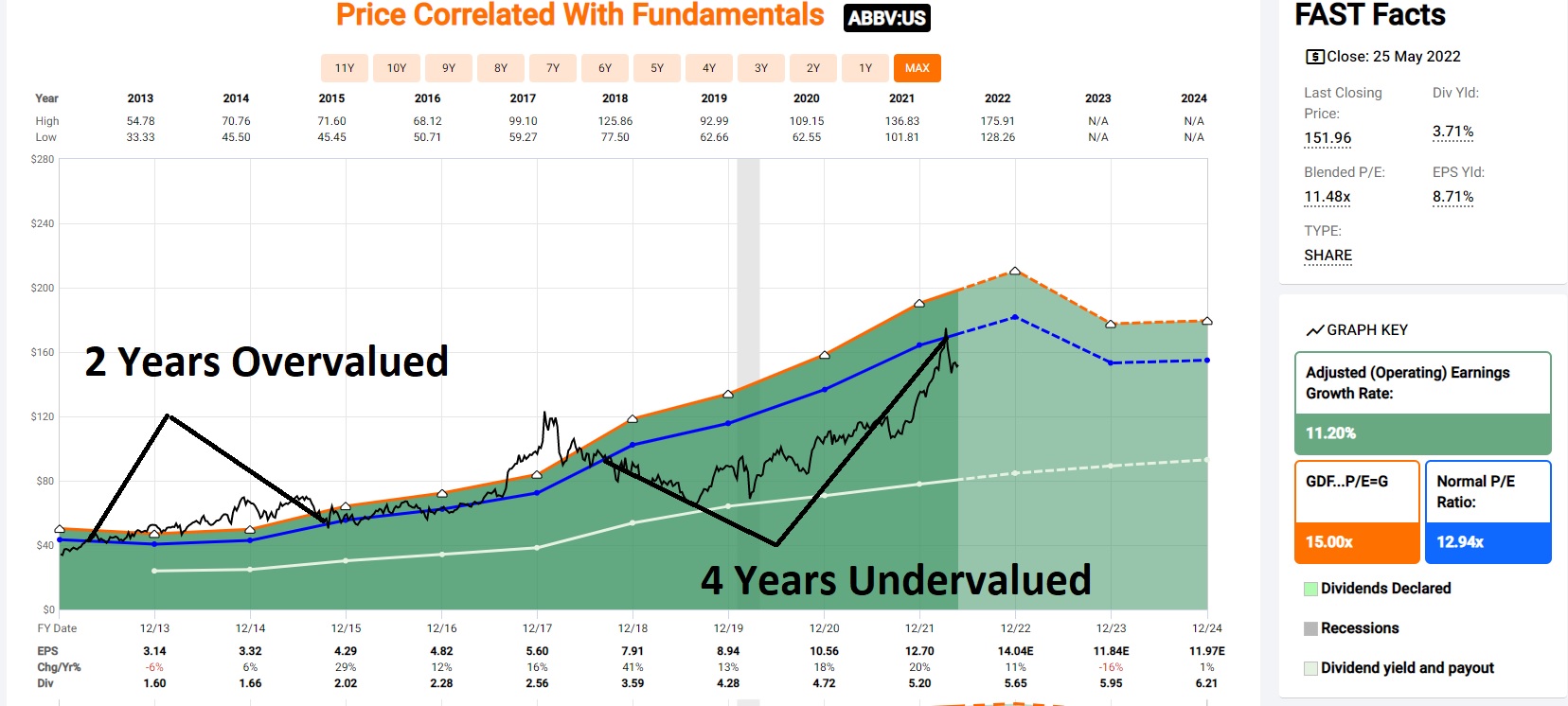

Blue-chips go through long stretches of over- and undervaluation.

Notice in this example how Pepsi’s 20-year PE is 21.

We’re not using a 15 rule of thumb because the market has determined that Pepsi growing around 7% is worth 21X earnings.

“Value is what other people are willing to pay,” and over the long term, Pepsi mean reverts around 21X earnings.

This is “relative value,” meaning when PEP is sub 20X, it’s actually modestly undervalued, even if value investors might not traditionally consider that undervalued.

Value investors might consider a 20 PE overvalued, but for PEP it’s not.

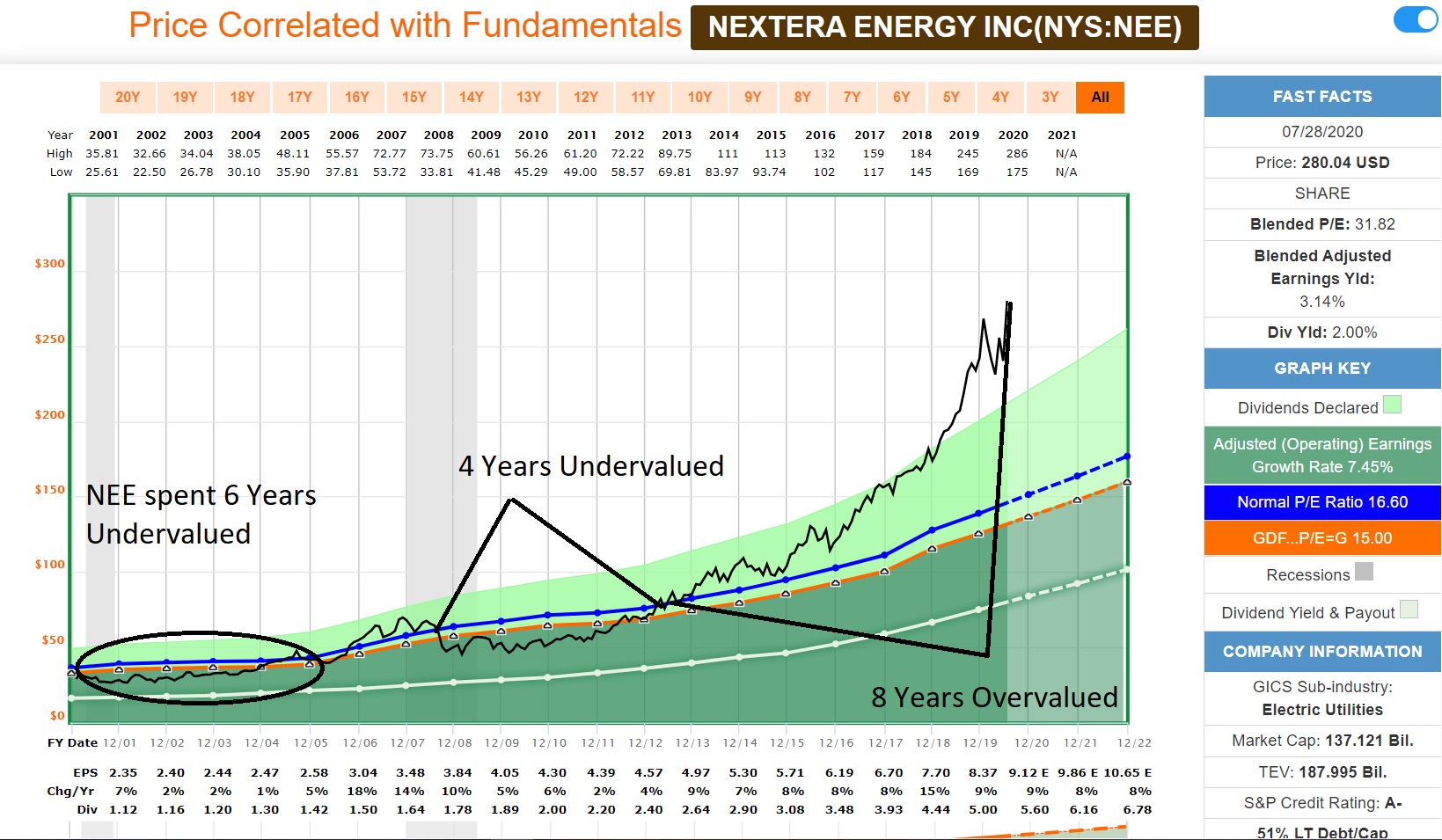

And what happened to NEE after 2019?

Well, it fell during the Pandemic but then went back into a bubble, due to the record stimulus triggering a mania in anything that was hot, and green energy was hot.

But what happens when a 20 PE stock (NEE’s 20-year average went from 17 to 20) is trading at 37X earnings?

Unless the growth rate accelerates (and management guidance was 10% the entire time), then that means a strong bubble was forming.

From 2016 to 2021, 5 years of bubble valuations, and then BOOM, a 41% decline (including dividends).

Like most utilities, NEE bottomed in late 2023 when 10-year yields hit their cycle peak (5% on 10-year yields and 5.3% on 30-year yields), and everyone hated high-yield stocks like Utilities, REITs, and even consumer staples.

Notice how NEE went from 5 years of “Can do no wrong” to 2 years of “can do no right” and now, off those 2023 lows, it’s once more delivered Buffett-like returns from a blue-chip bargain hiding in plain sight in 2023.

Venture capital like returns from an A-rated dividend aristocrat utility.

So, Why Not Just Rebalance Only During Bubbles?

The reason we use a 50% historical premium as a “potential trim/sell” signal is that historically, the S&P became 50% overvalued at the peak of the tech bubble.

That was the worst US stock market bubble ever, and resulted in a 37-month bear market (peak to trough).

The same is true for most blue-chips I’ve seen; they can become more than 50% overvalued, of course, BUT once a stock becomes 50% historically overvalued, then I’ve never seen a gradual deflating of a bubble. It always ends up in a bear market crash.

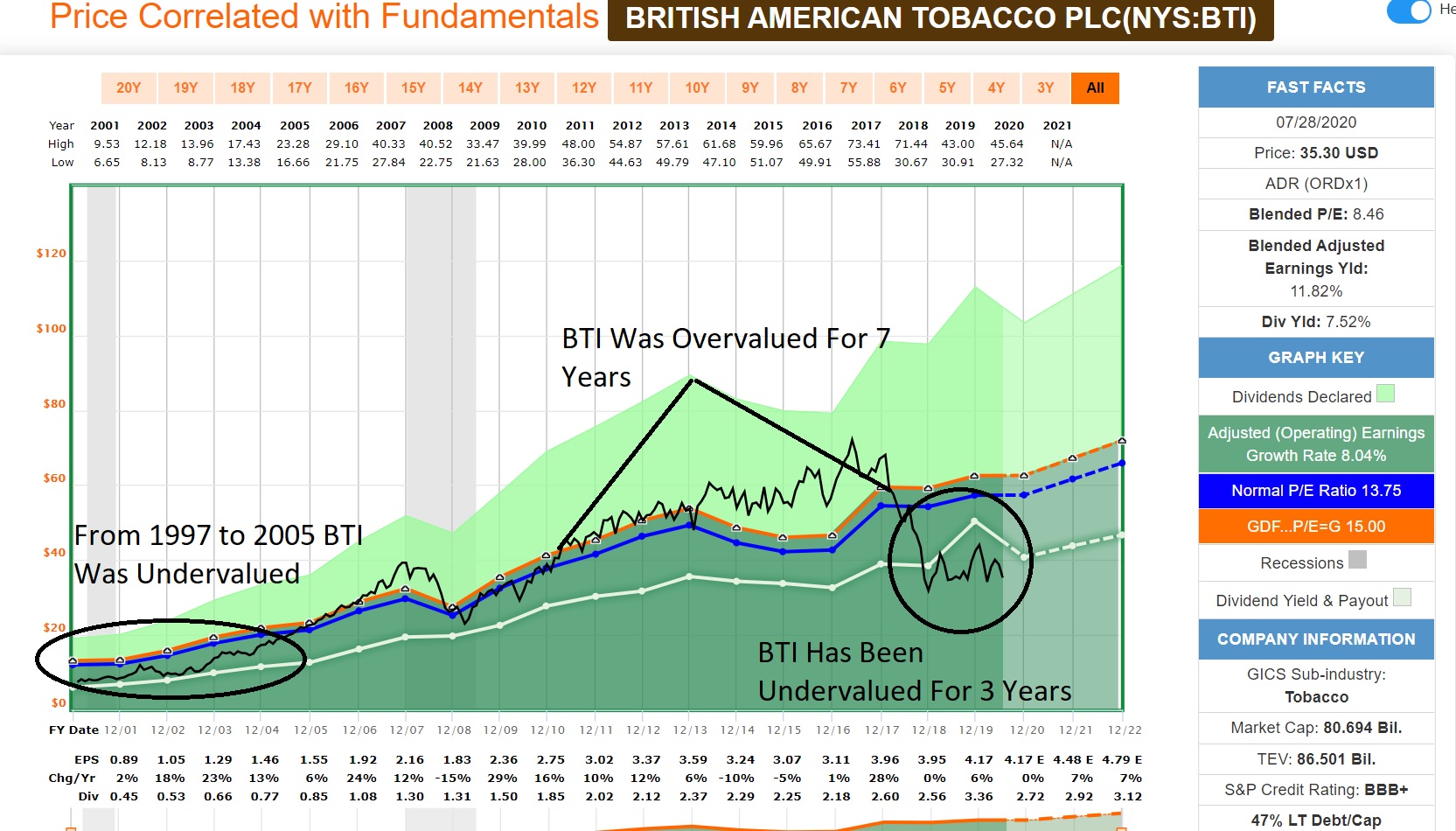

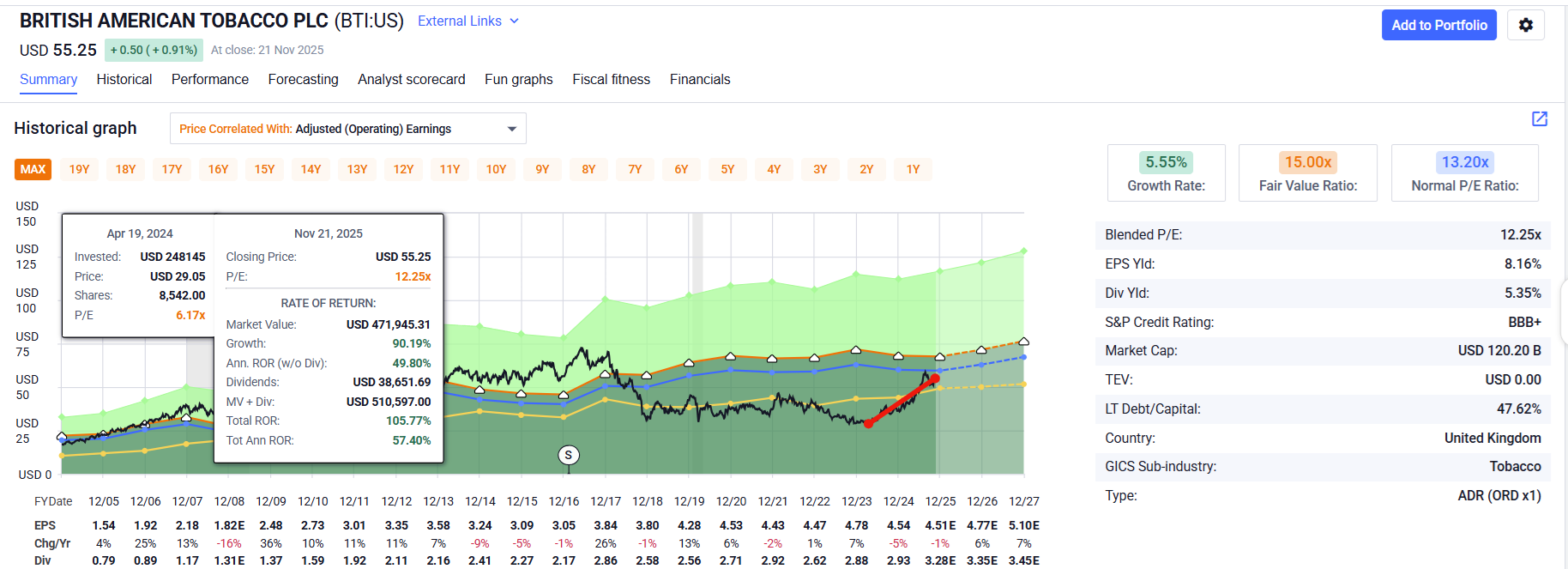

BTI was overvalued for about 8 years, due to the TINA (there is no alternative) created by zero interest rates, making dividend investors think that they could pay any price for a dividend stock and get away with it.

BTI historically trades at 13X earnings because of its stable business but unique risk profile.

And why did investors think that 21X earnings were OK? Because for 8 years the PE was above 13, so “maybe this time is different”?

Nope, the price got cut in half despite earnings growing at their historical rate, and then the price basically traded flat for years.

After The Crash, BTI Drifted Lower For 5 Years, And Dividend Investors Who Bought at 8.5X PE or less made modest 6% to 7% annual returns during the “Dead money phase”

And of course, patient investors who kept buying steadily and reinvesting dividends?

The Nasdaq’s historical returns over the last 40 years are 13.5% CAGR.

Despite the 7-year bear market, smart investors in BTI earned Nasdaq-like returns, and of course, if you were reinvesting dividends and steadily buying more, then you nailed the bottom (using yield-based limits, max yield 10.1%), and then you got returns like this.

Buffet-Like Returns From Blue Chip Bargains Hiding In Plain Sight

Thanks for Making My Day, Glenn!

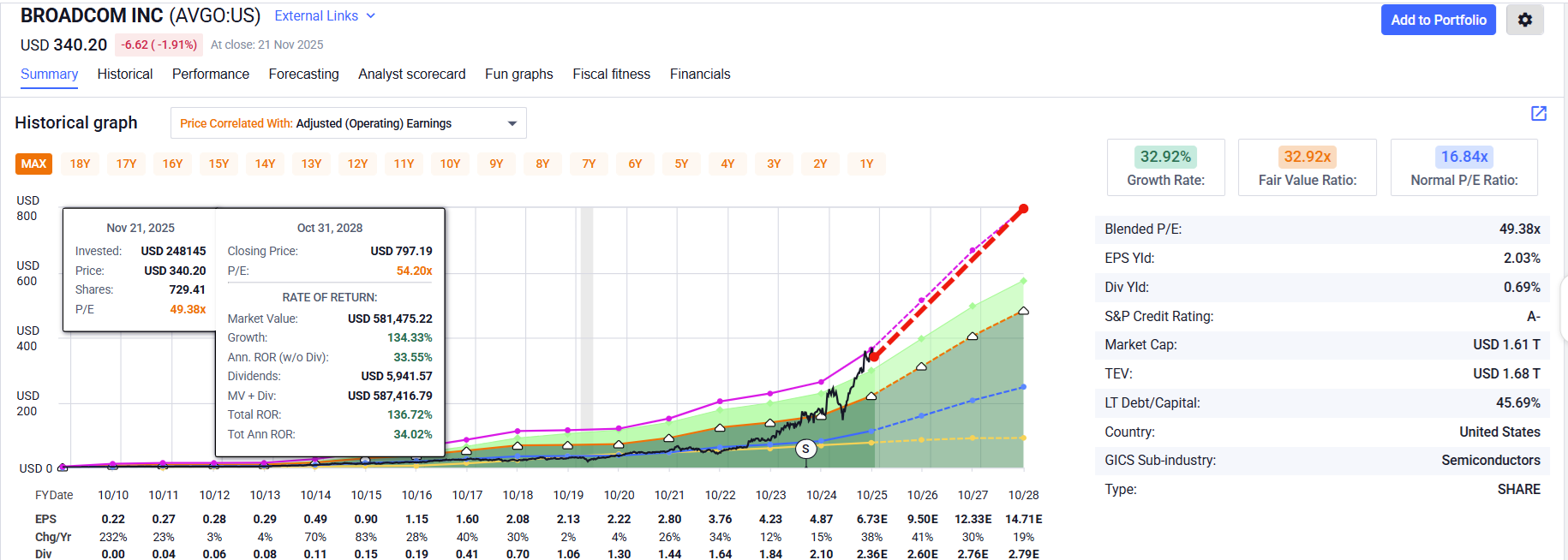

It’s important to remember that fair value PEs will change over time as the stability of cash flow does, such as with AVGO, where 50% of revenue is now recurring subscription software, not chips.

Morningstar Fair Value $365 = PE of 54.2 (I consider this a highly speculative fair value)

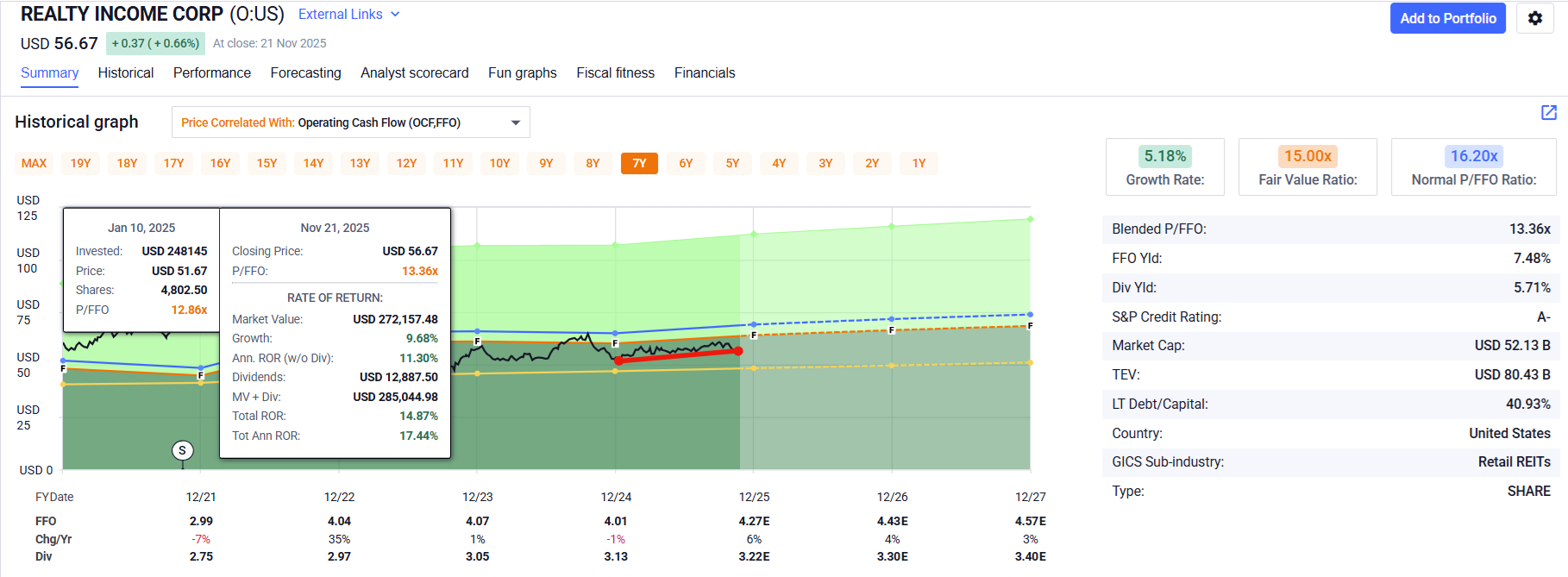

So what is the point? That you can’t just rebalance at extremes UNLESS you become an expert in a handful of high-yield stocks, like certain Dividend Kings members did, with BTI, PM, O, MO, EPD, ENB, ect.

5 to 10 high-yield aristocrats in 3 sectors, and then as they became historically EXTREMELY under- or overvalued, they would rotate based on yield percentile tables like this one.

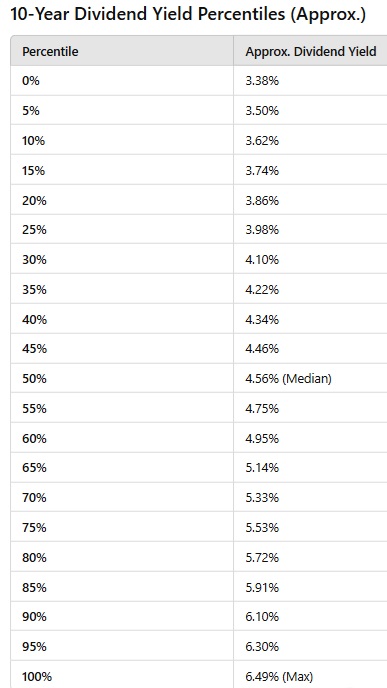

Realty Income Yield Table

In other words, at the 75th percentile yield, you start buying aggressively (yield limits), funding those purchases with sales of overvalued aristocrats you own, hopefully like Philip Morris.

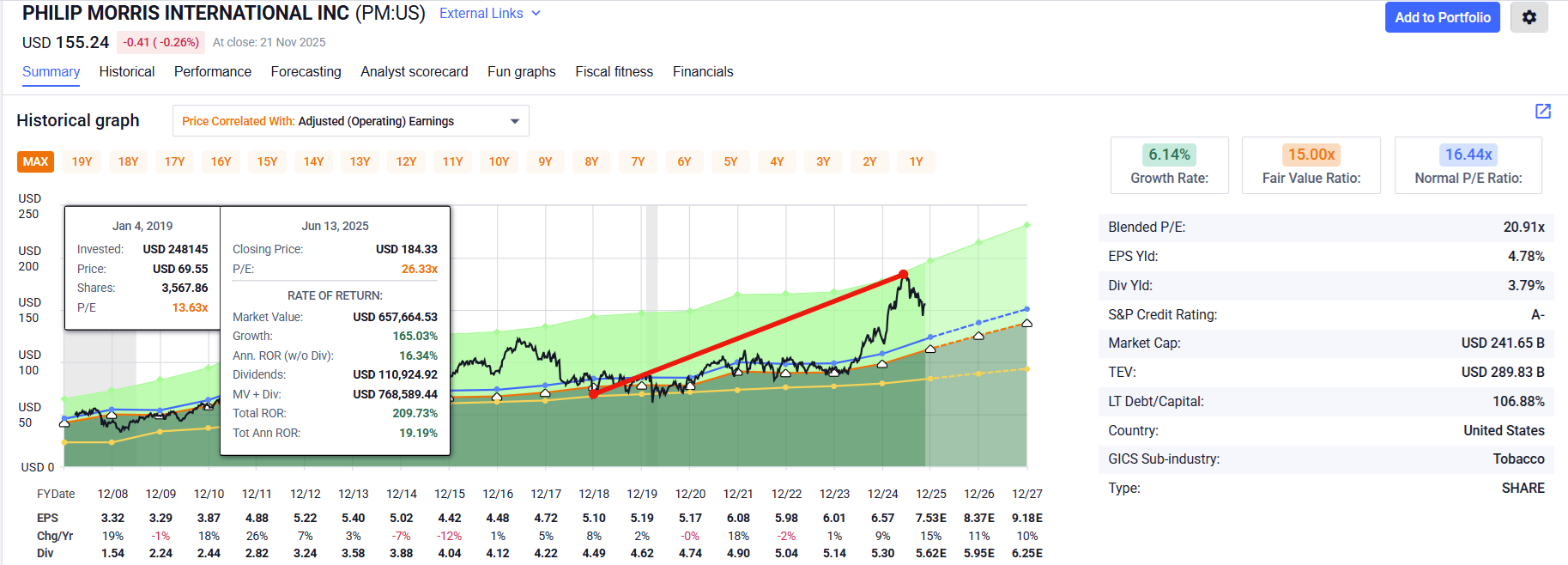

This year, Realty Income hit a 6.3% yield (95th percentile), which was a screaming buy (thesis completely intact), and Philip Morris hit a PE of 26 vs a historical 16.

Mind you, the growth outlook had improved enough to justify that (PEGY showed fair value), BUT if you were a high-yield long-term relative yield harvester? Then, even though PEGY said PM was fairly valued (if it could achieve the 9% long-term growth expected), you would have rebalanced out of PM and into Realty Income.

Avoiding that PM correction and getting into Realty at a 95th percentile yield whenr there was nothing wrong with the company is an example of how very specialized investors (who focus on a handful of companies they know are stable, safe, and know very well) can make Buffett-like returns (and 15% long-term returns) while living on 5% to 7% yielding portfolio, without ever having to worry about AI, tech or anything else.

Only the fundamentals of their specific high-yield aristocrat investors.

OK, so why not do that? Why not select just high-yield aristocrats and rotate into and out of them? Why take the risk of investing in AI stocks like Nvidia, where you always have to worry about disruption and tech changes?

There Is No Perfect Investing System

Why can’t you just rebalance between different blue-chips when they are at historical extremes in valuations? Why not sell a stock at a 50% premium to buy another one at a 50% discount?

That would be a magic money machine, wouldn’t it? Here is the reality that we humans are faced with.

Life is complex, business is complex, and nothing ever goes to plan. And what does that look like in terms of the stock market?

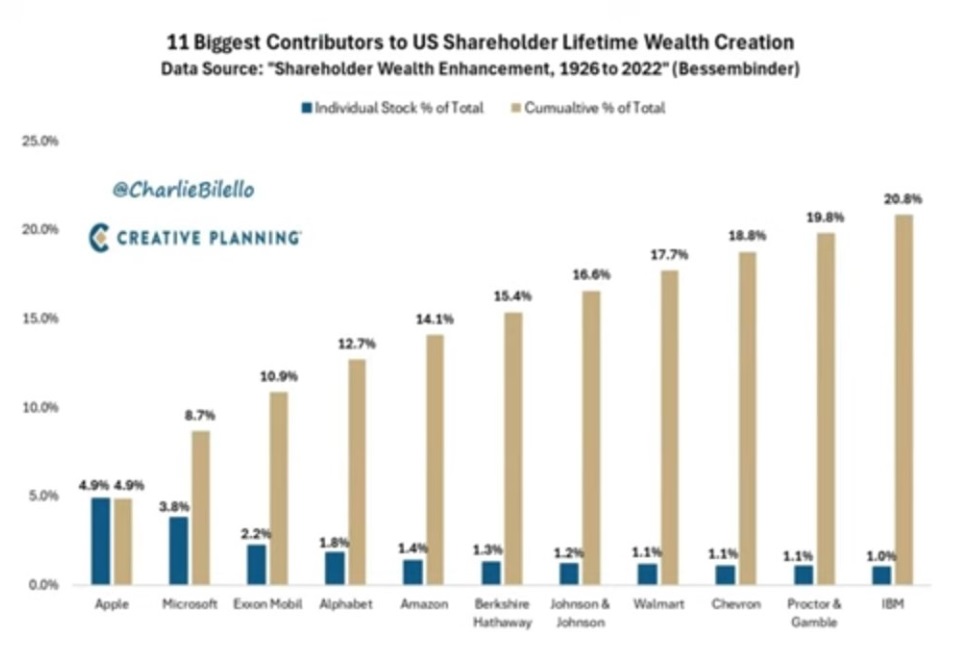

You might have heard how the top 20% of companies earn 80% of the profits. Or that the top 1% of AI users use 30% of the tokens? Well, 21% of historical stock returns come from a handful of the biggest winners. In fact, 11 companies have generated 21% of all stock market gains over the last 10 years. 5% of those are from Apple alone.

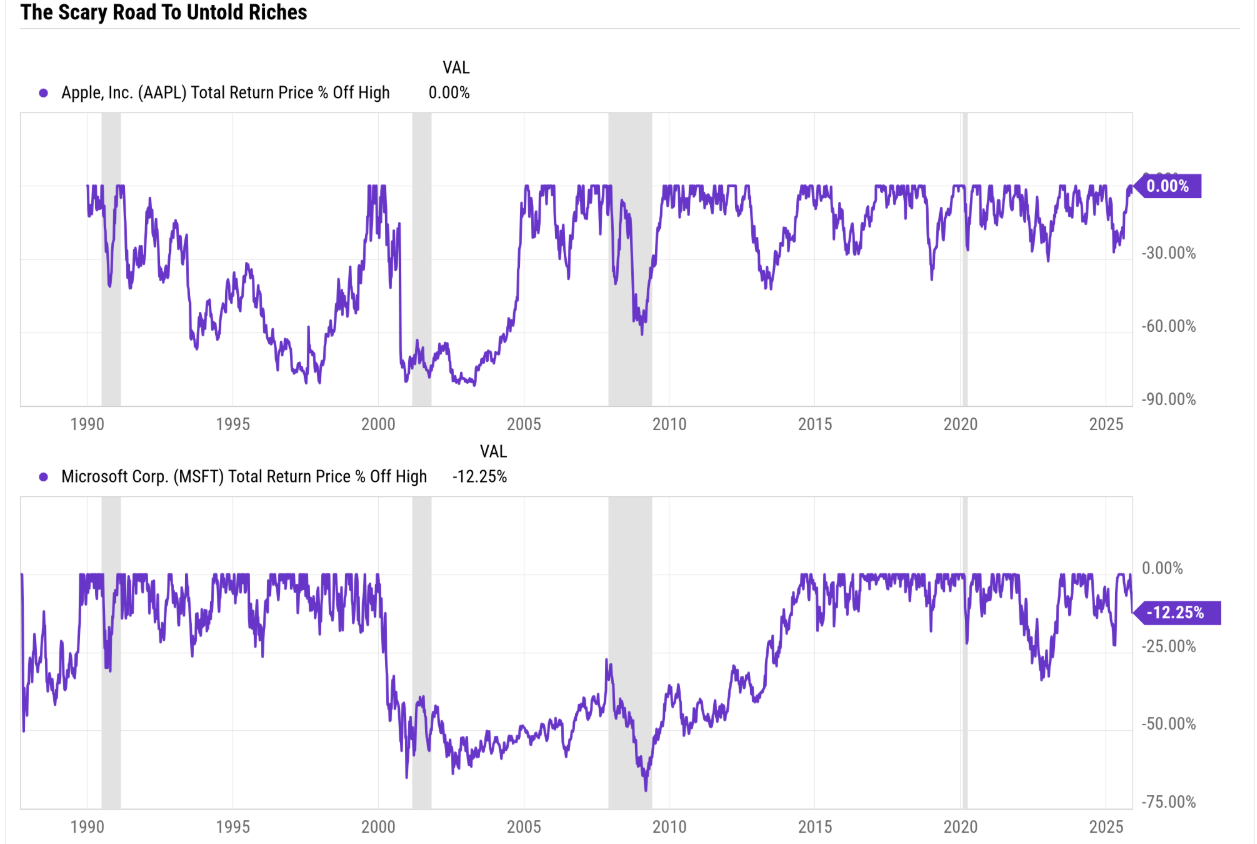

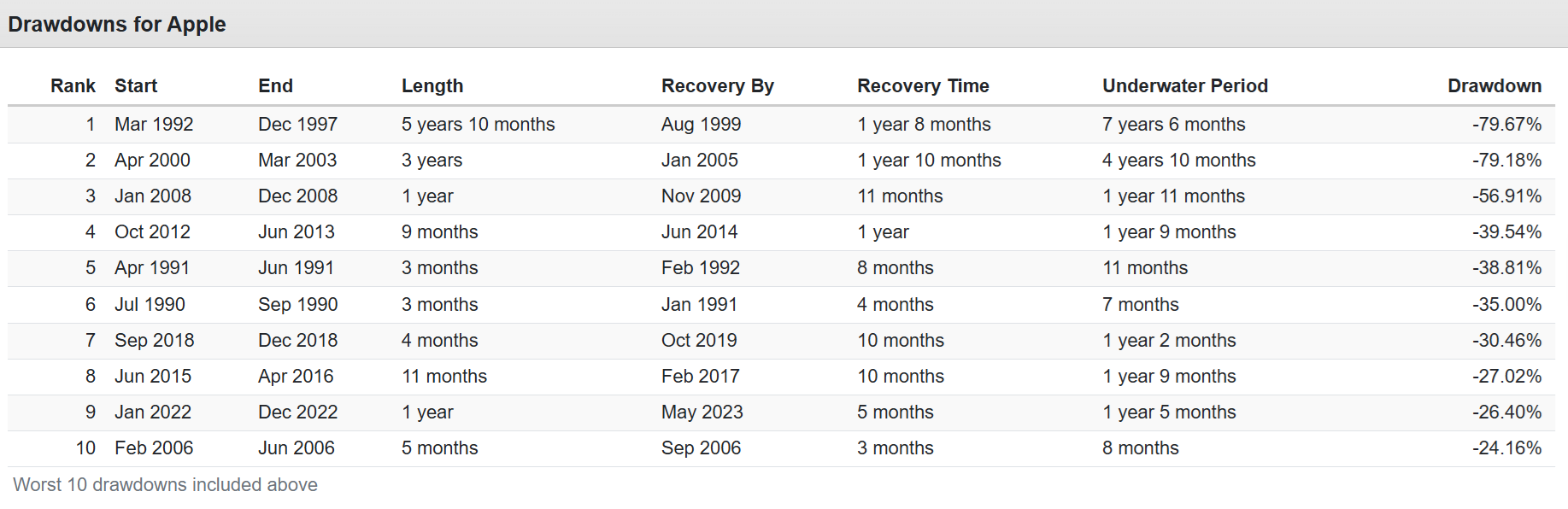

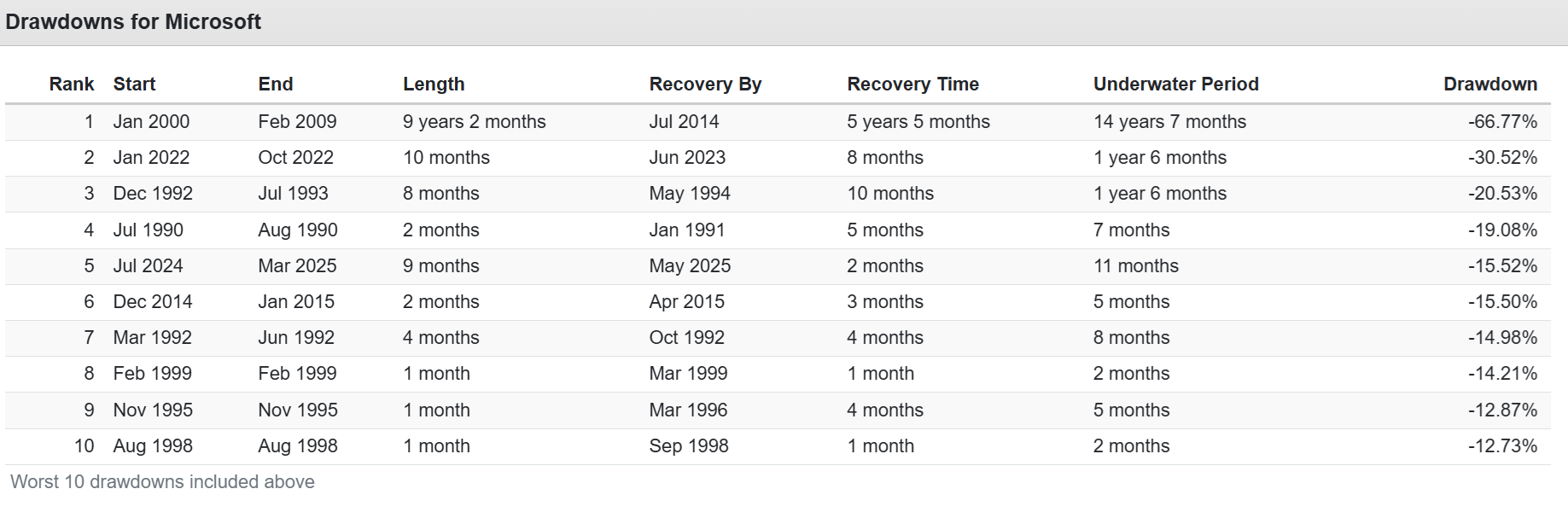

Look at how Apple acted over the decades on the road to earning 5% of all stock market gains over the last 100 years.

Now look at the bear markets themselves.

Apple & Microsoft Bear Market Since 1990

Apple has spent 7.5 years underwater, and that was DURING the tech bubble!

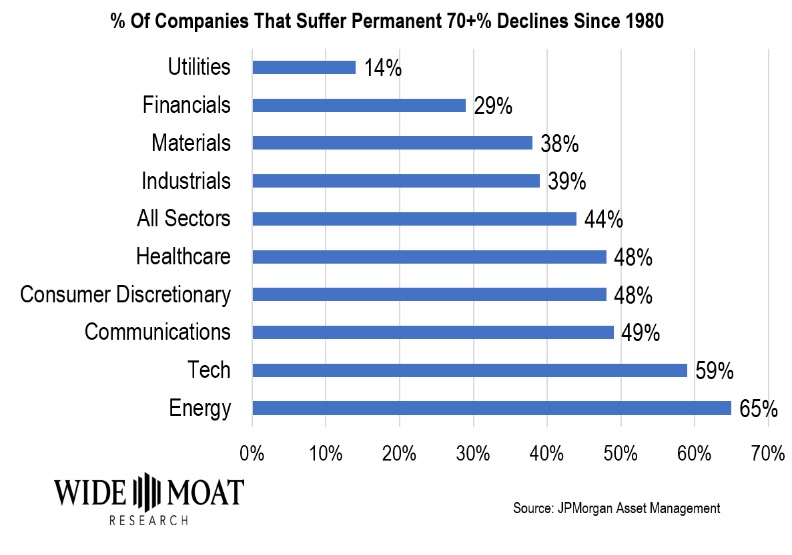

And These Are The Biggest Winners In History!

44% of stocks that fall 70+% never recover.

Amazon’s 93% tech crash plunge? It bottomed in February of 2022 and was up 60% by the time the S&P bottomed in October 2022.

Netflix was down 70% in 2022. Meta 75%.

Most of the time, a tech stock that’s down 70+% is never coming back. The thesis is broken, the business is struggling, and may never recover previous sales and profits.

THIS is why stocks are always and forever a risk asset.

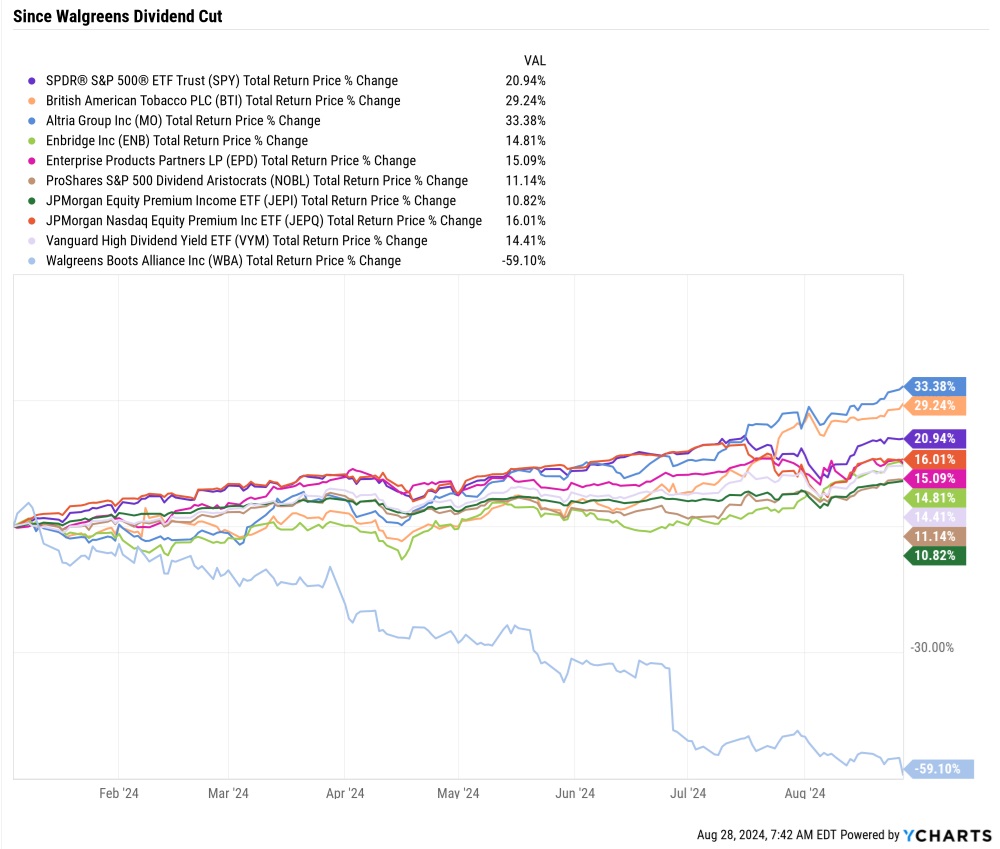

Right Before Walgreens Was Acquired By Private Equity

This is why diversification is critical: even dividend aristocrats like Walgreens, AT&T, 3M, and so many others can end up cutting their dividends. What do we know about dividend cutters?

THIS Is Why No Dividend Stock Is A True Bond Alternative…Ever

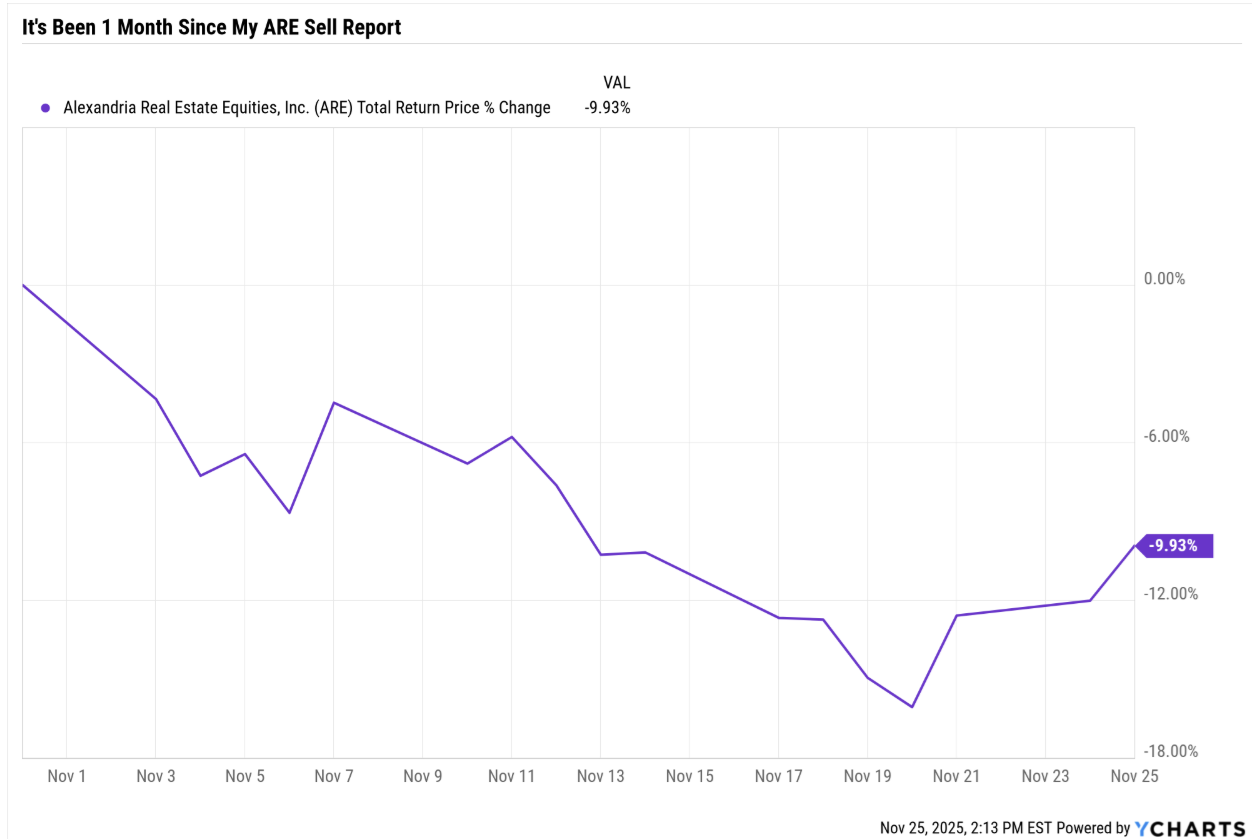

Remember how the thesis on Alexandria Real Estate (ARE) broke a few weeks back when management telegraphed a likely dividend cut?

Did it suck to take a $163K loss on ARE? Because we didn’t have the rule about a potential telegraphing of a dividend cut turning off limits (all 15 limits filled the next morning before I was able to rerun the analysis of the thesis)? Yes.

Sometimes a dividend cutter is OK (like OXY).

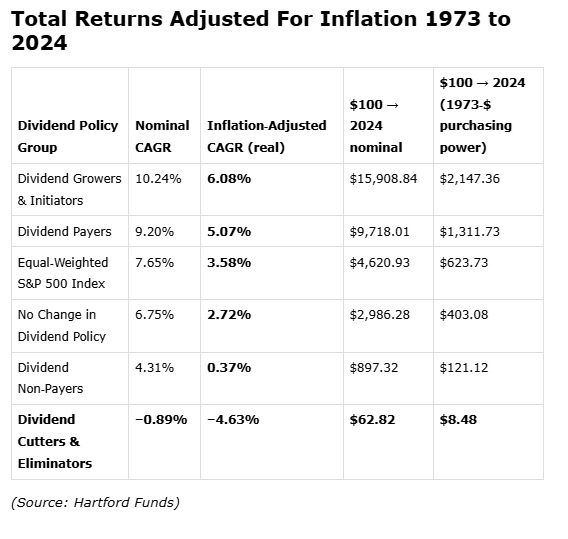

But usually? The thesis is broken, and historically, adjusted for inflation, over the long term (50 years), dividend cutters lose 91.5% of their value.

That’s why we use dividend cut risk as the proxy for overall safety and quality for a company. Because a healthy company will eventually pay dividends, it will grow dividends. Any dividend cut? Here’s what that actually tells us.

This is the first dividend cut in 53 years…so despite what we are telling you about our future, it’s objectively the least financially stable and healthy we’ve been for 53 years.

That’s what I heard when VF Corp (a dividend king) cut its dividend. Management dressed it up all nice and pretty, but that was the hard, objective truth.

Just as free cash flow per share is the gospel truth of a company’s long-term value, so too is the dividend the gospel truth of management’s commitment to shareholders and treating us like actual business owners and partners.

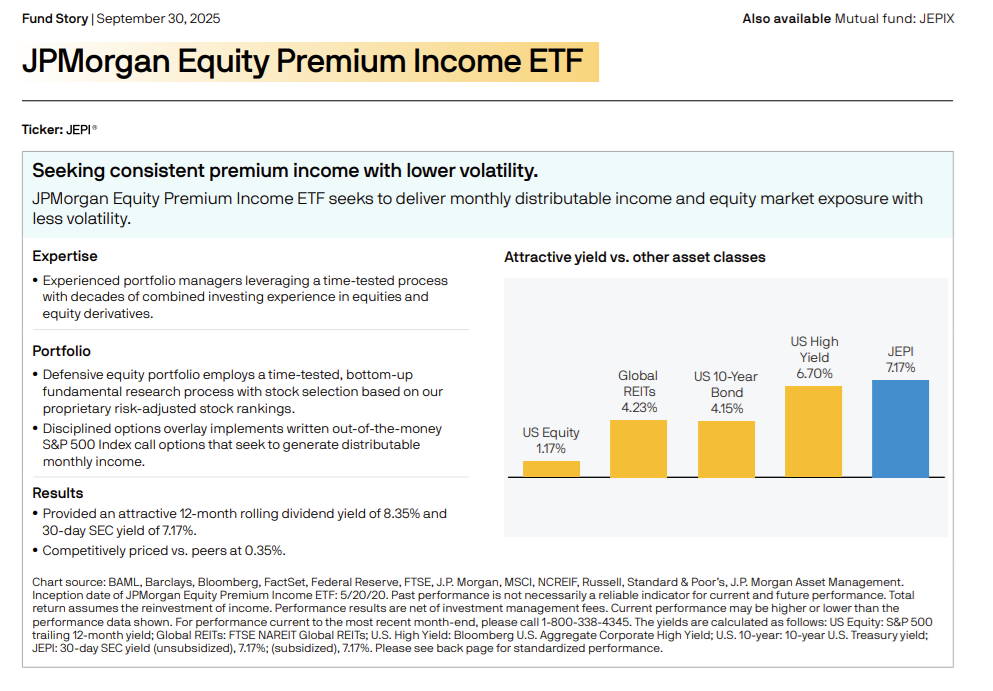

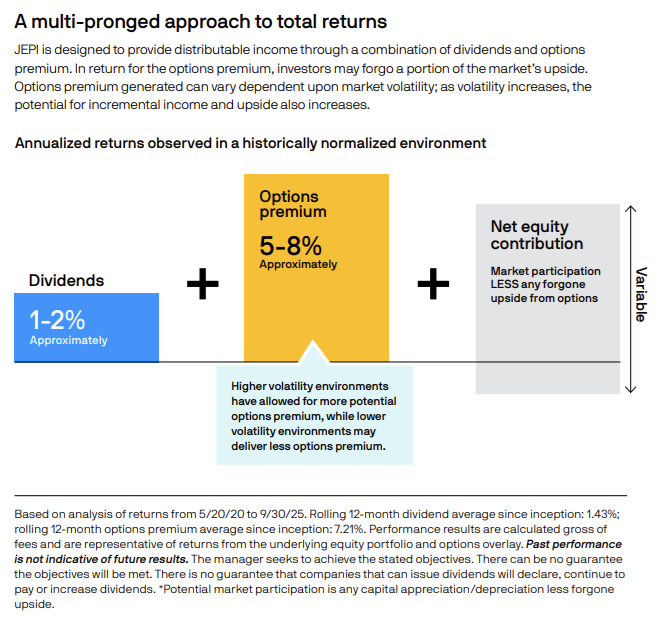

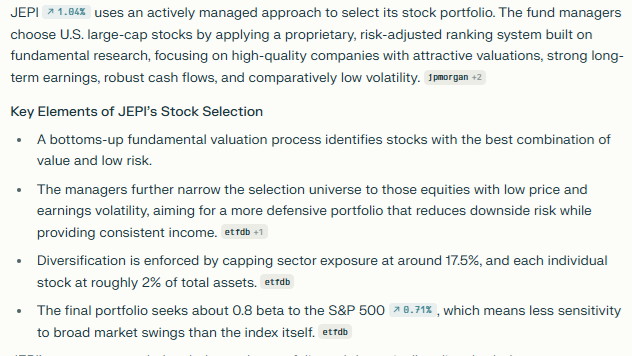

So Why JEPI (or Other ETFs Like It) Are A Great Option For AI-Powered Dividend Minting “Magic Money Machines”

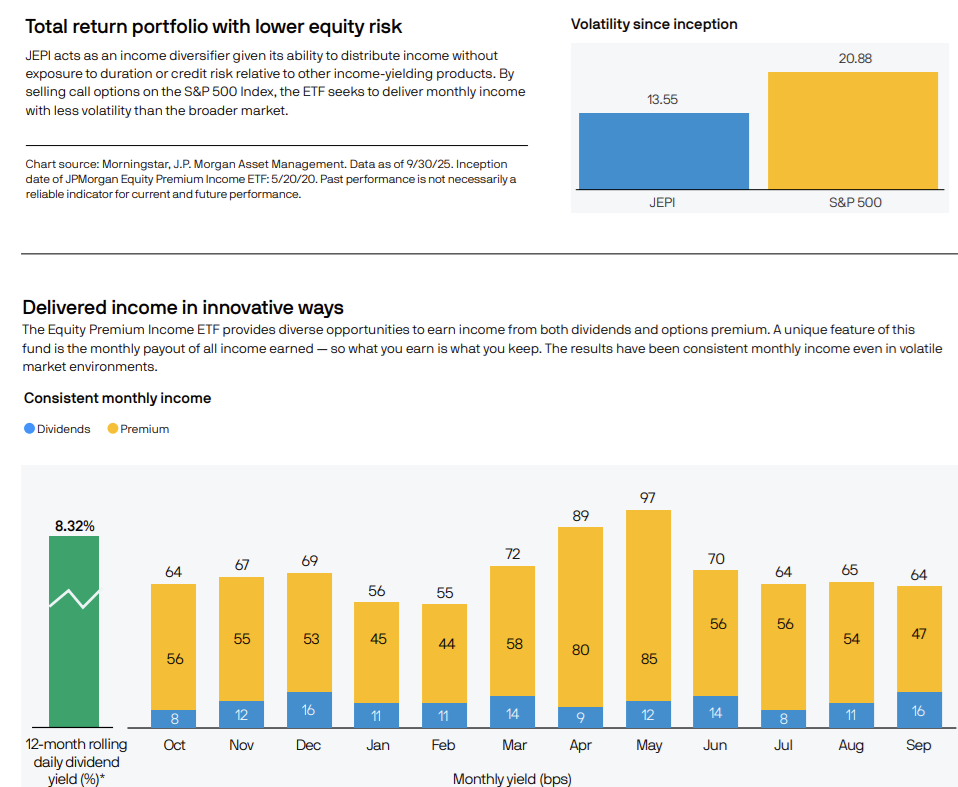

JEPI is offering a very attractive yield relative to other kinds of income-generating assets, BUT that doesn’t make it a bond alternative.

JEPI is designed to generate 6% to 10% long-term returns, via option premiums generated by

JEPI harvests market volatility to generate income, and has a goal of 8% long-term returns (slightly better than a 60-40’s 7% per year) but with somewhat lower volatility.

65% lower volatility vs 80% for a 60/40 with 1% higher long-term returns.

The Pros Of JEPI

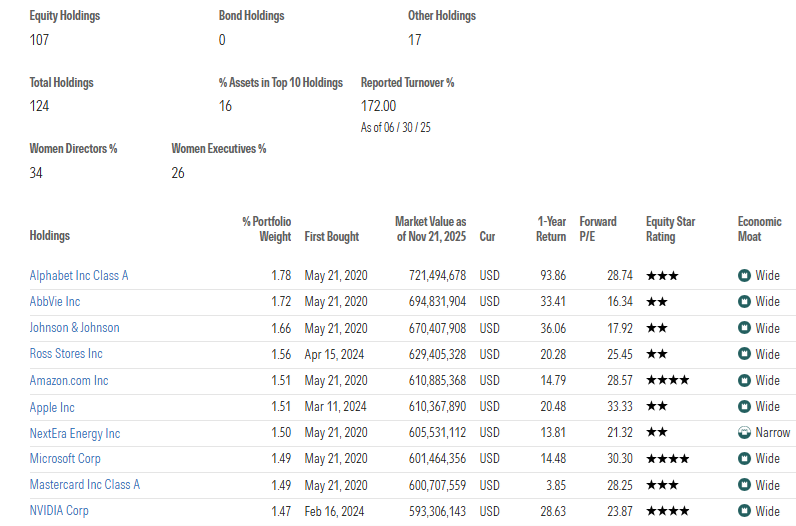

JEPI is a diversified actively managed SIMILAR portfolio, though not quite the same as an equally weighted S&P.

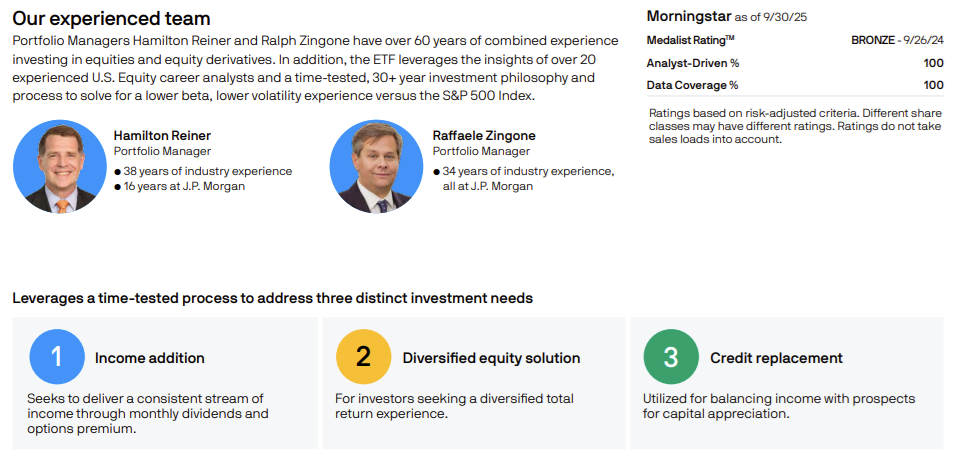

Management is provided by Hamilton Reiner and Raffaele Zingone, who have 72 years of experience in asset management and who target companies they believe have the most stable earnings.

Thus, the high overlap with the S&P equal-weight.

The nice part about JEPI’s income strategy is the exchange-linked notes, which work the same as covered calls, BUT have trade-offs that make them ideal for JEPI’s goals.

Specifically, JEPI is able to write ELNs on only 15% of assets, allowing greater upside than if they were simply writing covered calls on all their assets.

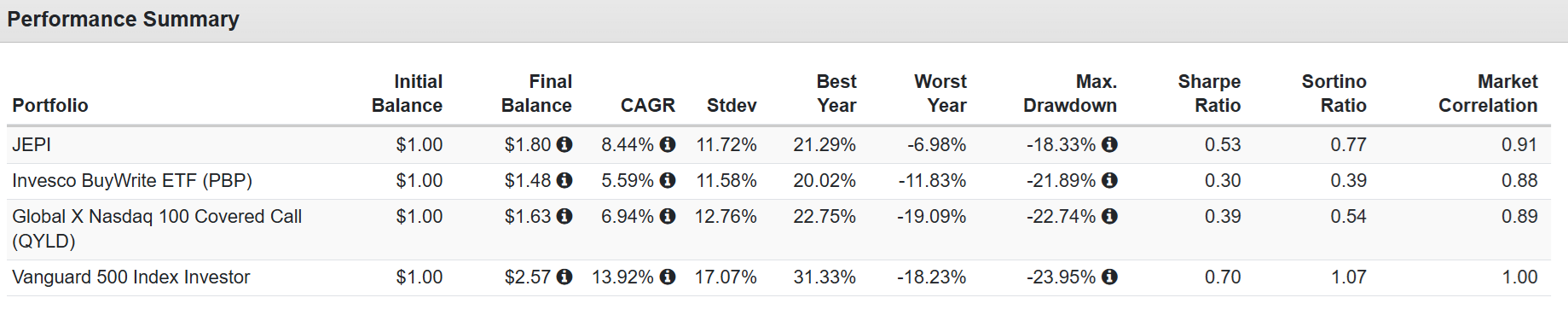

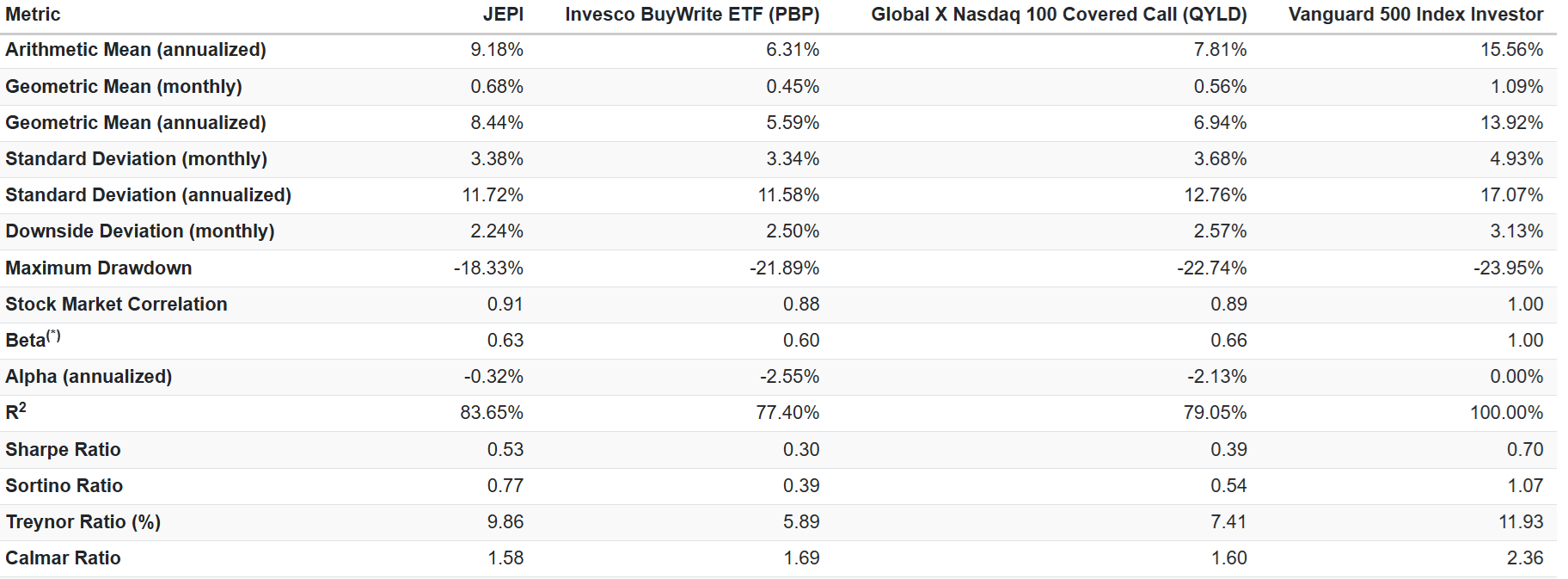

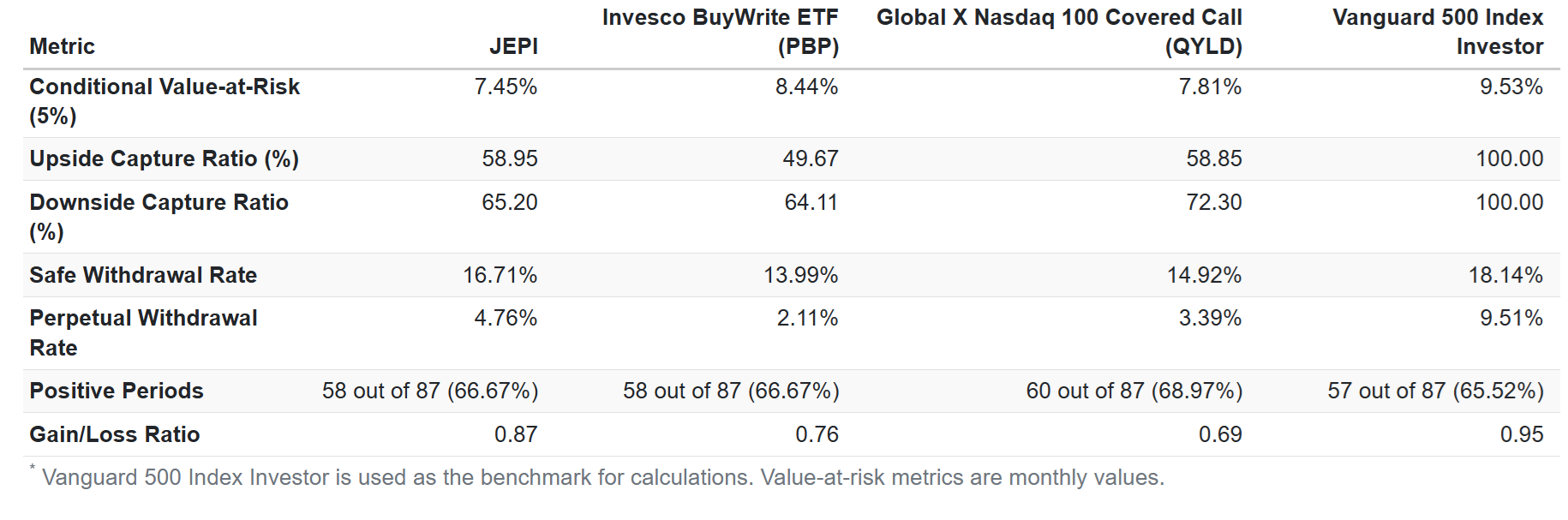

JEPI Vs Peers Since 2018

The beta (volatility vs S&P ) is similar with most covered call ETFs.

But the superior volatility-adjusted returns are courtesy of JEPI’s ELN, which powered higher returns, AND also its impressive upside/downside capture ratio.

So what makes JEPI special? Capturing the same upside as QYLD (Nasdaq covered calls) but with a slightly less downside capture ratio and higher total returns (and income) over the long-term?

More income, more returns, and with lower volatility? That’s why income investors love JEPI, and that’s why combining it with growth stocks like the AI titans is such a powerful way of turning high-yield into an AI-powered “Dividend Minting Magic Money Machine” (DM4)

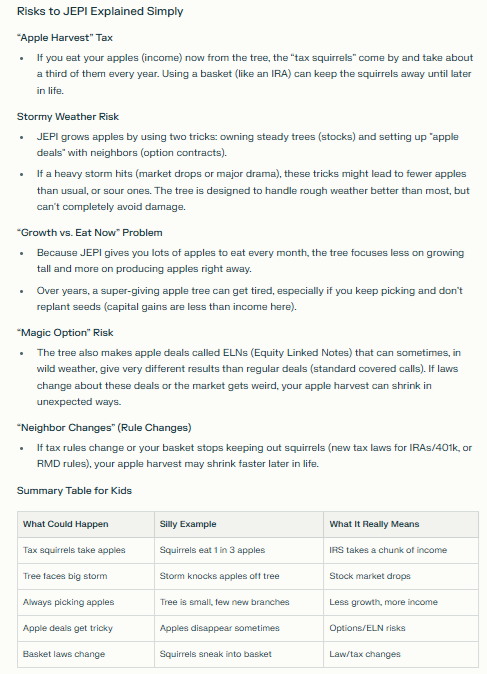

What’s The Catch? What Are The Risks To Be Aware Of?

Only two certainties in life! Death and taxes...and in the age of AI, we can only be sure of one of those😉

JEPI and ETFs similar to it, where almost all the returns are in the form of income, are ideally held in tax-deferred accounts like an IRA or 401 (k), or in a taxable account (not tax-free once RMDs begin, but tax-free compounding for decades).

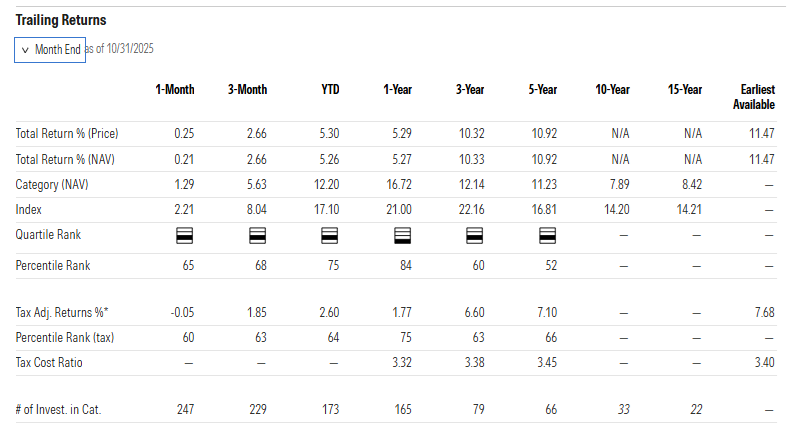

As you can see from Morningstar’s data, while JEPI’s long-term returns (based on monthly closing prices) show 11.5% CAGR total returns (about 2% of that is growth, and the rest is income, averaging 9.5% per year), the after-tax return is 7.68%. In other words, 34% of the total returns are going to taxes, and that’s something that will eat into compounding over time.

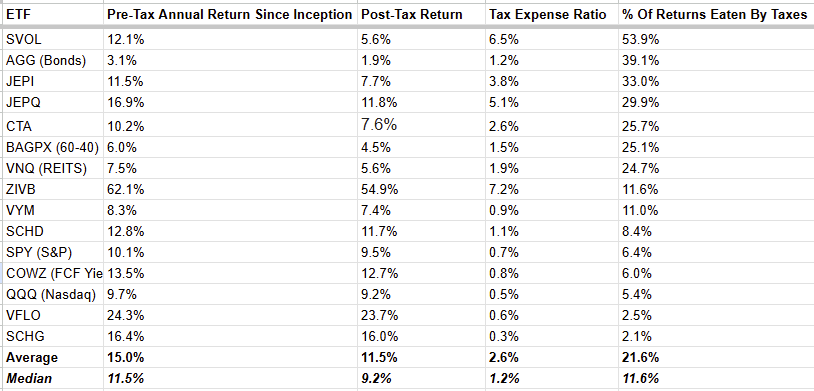

ETF Pre And Post Tax Returns

You can see the tax efficiency of ETFs will vary by asset class, with some ETFs, like SVOL, which uses options to harvest volatility on the VIX, losing over half of their historical returns to taxes. Bonds are around 40% to taxes, and JEPI historically is 33% with its slightly growthier sister JEPQ, slightly less at 30%.

The more total returns there are, and the more capital gains relative to income making up those returns, the more tax-efficient the ETF will be, as you are compounding more efficiently.

That’s why you have things like the Nasdaq at 5% of returns to taxes (95% tax efficiency) while REITS are only 75% tax efficient.

JEPI Risk Profile So Simple A 5th Grader Could Understand It😉

Bottom Line: Dividend Minting Magic Money Machines Are The Best Way For Long-Term Income Investors To Make Their Financial Dreams Come True

As we’ve seen with the JEPIX example (7 years of history), a strong enough growth stock (like Nvidia) combined with a high-yield portfolio can generate more money than a pure high-yield strategy alone.

Adjusted for taxes, 7 to 10 years is the typical breakeven period required to make owning growth stocks worth it and maximize long-term income.

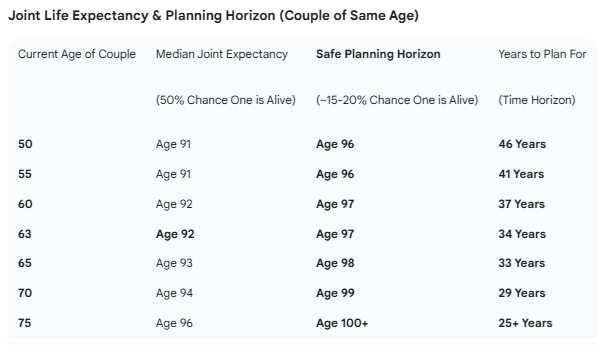

However, remember that even if you’re retired, you or your partner is likely to live long enough that 7 to 10 years is a realistic time frame. So if you are 70 years or younger? Then, combining yield and growth statistically might be something worth considering.

And don’t forget about basis points. One of the easiest mental hacks to enjoy your money more is to measure everything in basis points and remember that a quality portfolio, consisting of the world’s greatest companies, is a money replicator, and that the basis points are constantly regenerating AND growing in size.

Everyone in the ZEUS family gets a one-basis-point birthday gift.

Or have your basis point donated in your name to your favorite charity.

When you measure life in “babies saved and basis points,” life gets more meaningful, more joyful, and a lot more interesting😉

Happy Thanksgiving, Everyone!