The news never stops flowing, but here is the most important news you need to know to help you stay sane, smart, and make your dreams come true, in this absurd age of AI😉

Today, I’m going to teach you some very profitable “secrets” about value investing in the age of AI and using one of the least AI companies as our classroom.😉

Comcast: Value Trap? Or Buffet-Style Fat Pitch?

Several GNG members have asked me whether Comcast is a Buffett-style deep value opportunity or a value trap.

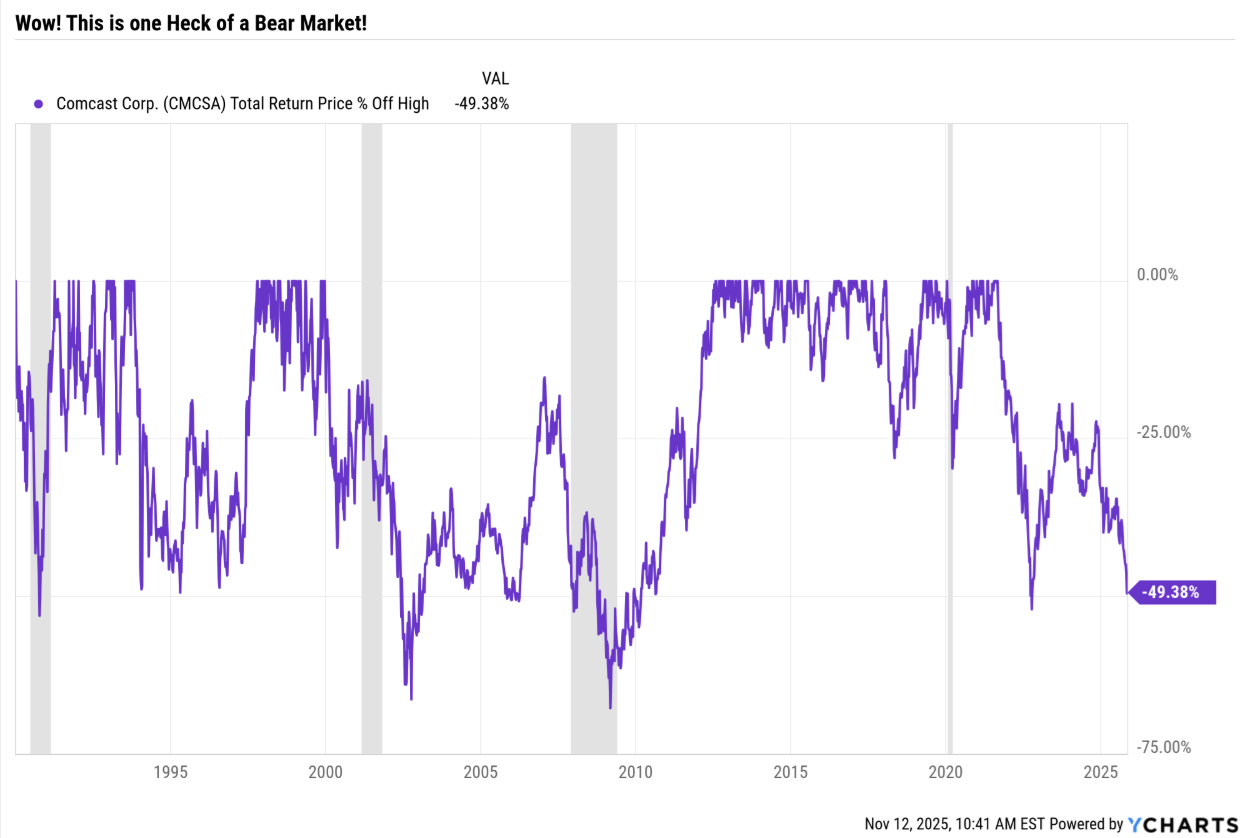

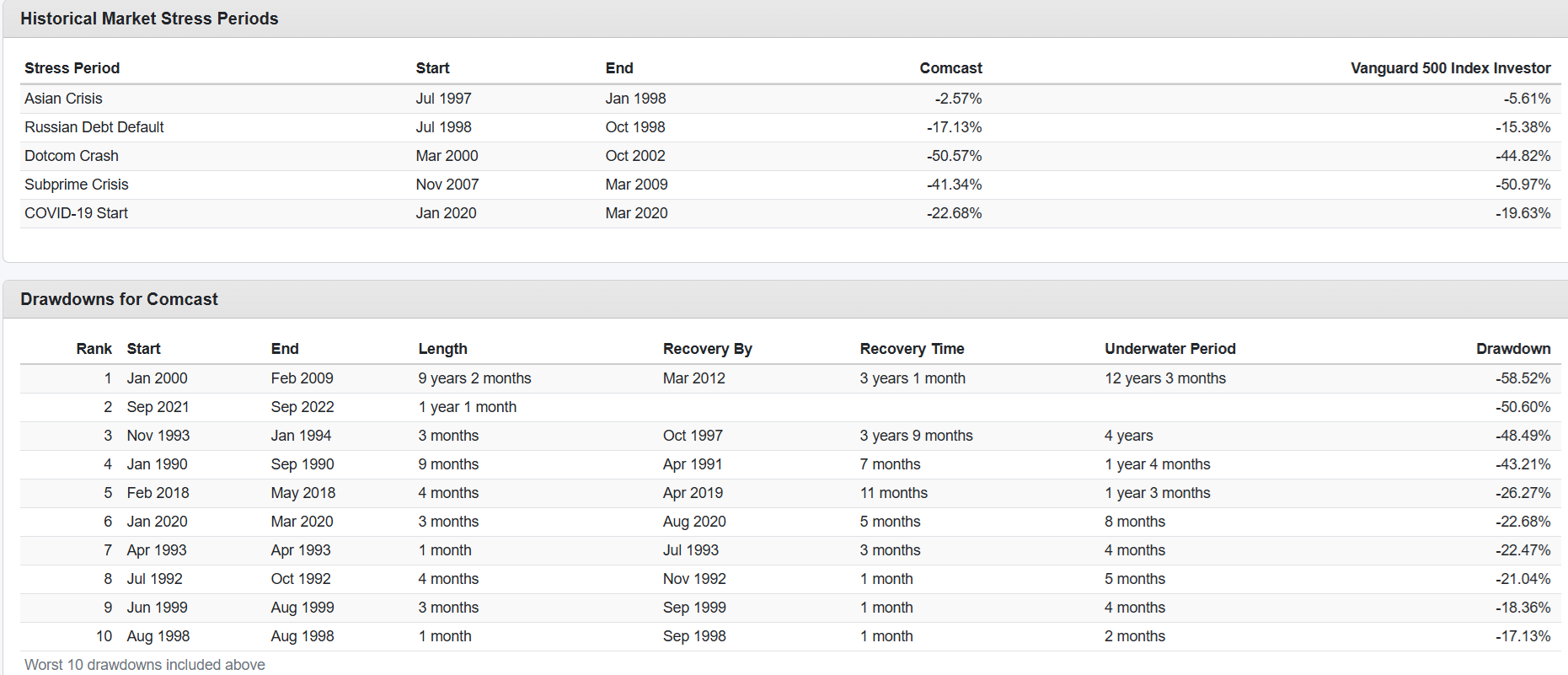

That’s a really interesting chart, so let’s see what the historical context is like.

Comcast Drawdowns Since 1990

This is the 2nd biggest bear market for Comcast, a company that historically has generated 15% to 16% annual returns via a combination of dividends and earnings growth.

Note that since 1990, the average 15-year rolling return is 10.7% which is a healthy 2.2% above the S&P’s 8.5%.

That 2.2% doesn’t sound like much, BUT context makes all the difference.

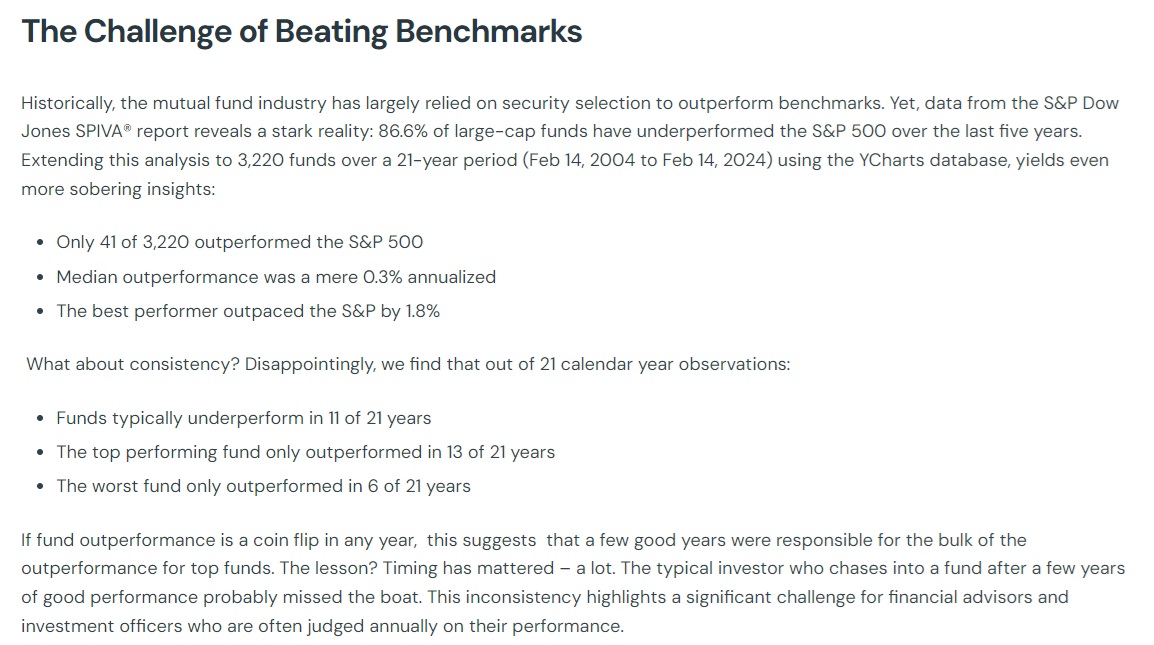

In the last 22 years, the best fund manager in America beat the S&P by 1.8%, and only 41 managers beat the market over the entire period. The median outperformance was 0.3%. So my hats off to Comcast for its market-beating prowess. BUT what about the future?

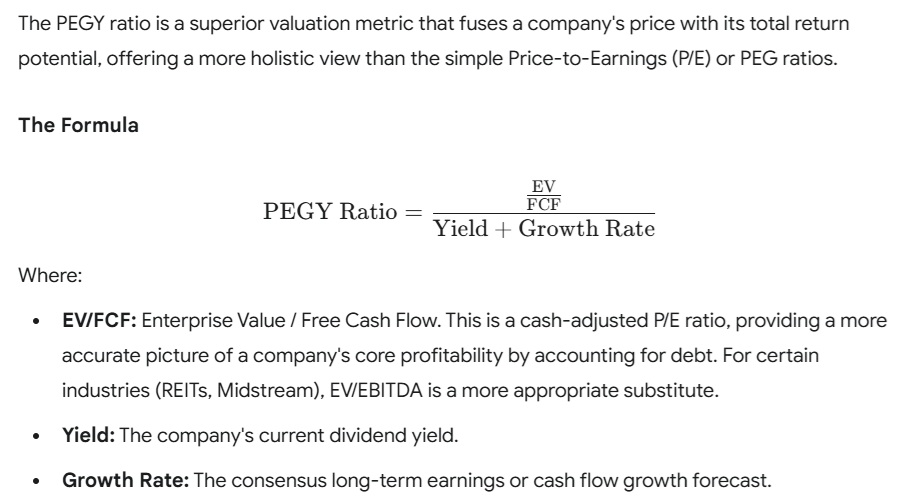

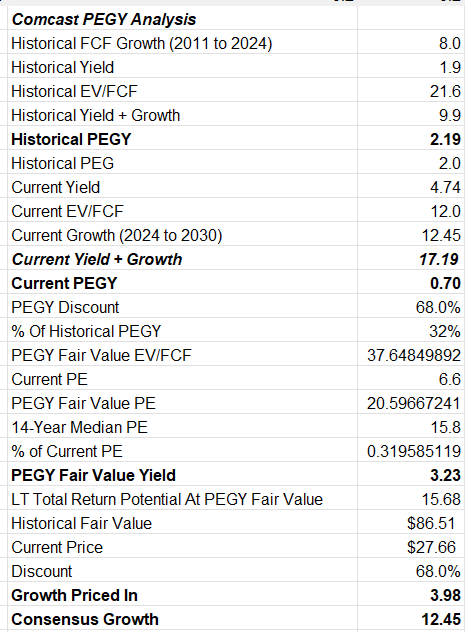

Comcast PEGY Analysis

For our new readers learning about us from Yahoo Finance, here’s a brief summary of what the PEGY ratio is and why I consider it one of the best valuation metrics you've never heard of.

Think of the PEGY ratio as a PEG ratio (PE/growth) but better.

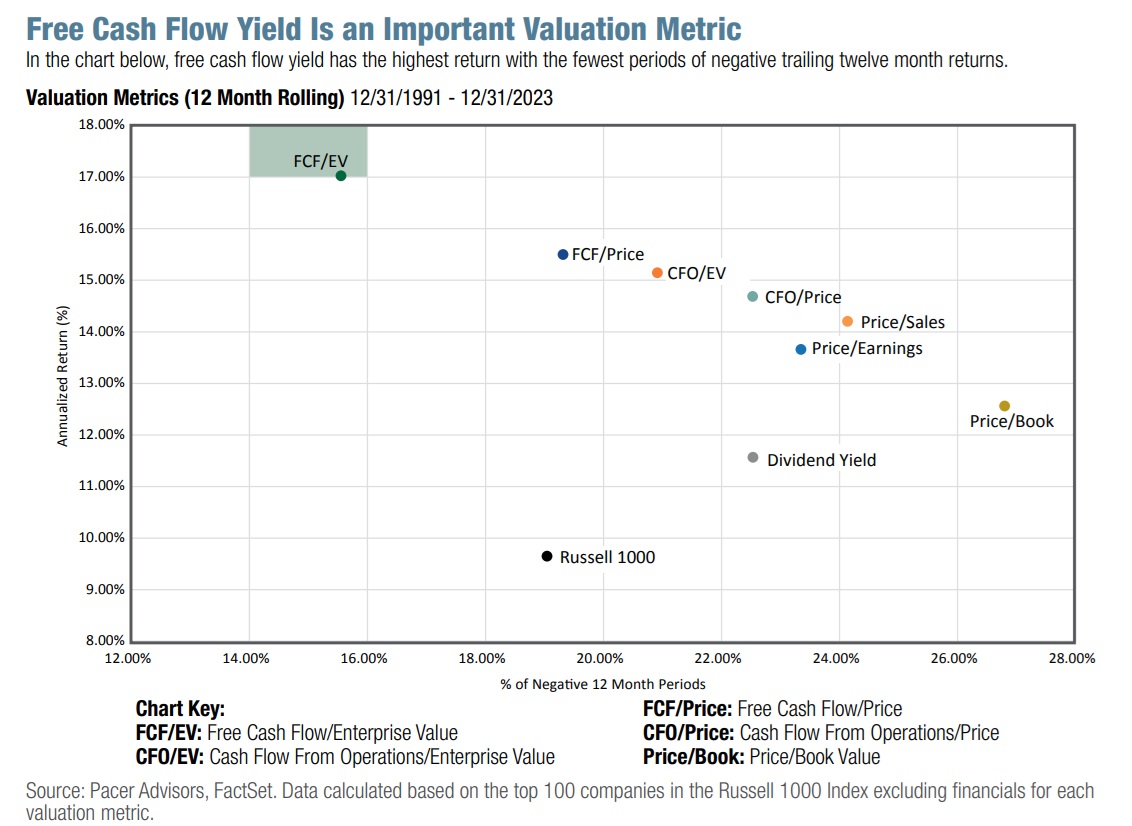

Have you wondered why “Value investing stopped working years ago?” Actually, if you measured valuation correctly, using free cash flow yield, value investing never stopped working.

As you can see, over the last 33 years, high-FCF-yield companies have achieved nearly Buffett-like returns, beating the market by 8% per year.

Remember how the best fund managers can beat the market by about 2%? Well over those 33 years, the value outperformance was 216X returns vs 21X for the S&P.

In other words, $1 invested in high free cash flow stocks turned into $216 and $26 in the stock market, for 8.2X wealth over the last third of a century.

Why Growth Matters Too!

The trouble with high free cash flow yield companies is that they might be cheap for a reason. Sure, they are profitable, but if the growth rates are bad, then valuation isn’t going to help you.

Yield + Growth + Change In Valuation = The Physics Of Finance

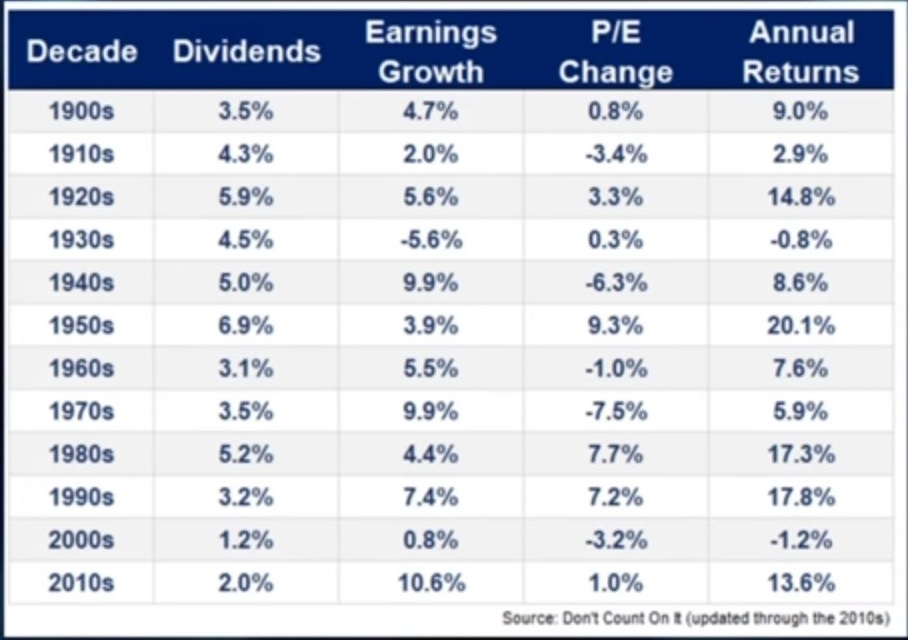

Fundamentally, only three things actually make you money in the stock market. Today’s income (dividend yield), tomorrow’s growth in earnings, and any changes in valuations (the valuation multiple).

For stable businesses, like Coca-Cola, where the business doesn’t change and growth rates change, valuation changes cancel out over time, and total returns are yield + growth in earnings/cash flow (which dividends track).

This is called the Gordon-Davidson growth model, and it’s what Vanguard, Schwab, Brookfield Asset Management, and almost all hedge funds use to model long-term returns.

That’s because its historical margin of error is 20%. In other words, a 3% yielding stock with 7% growth is expected to generate 10% long-term returns, and that means 8% to 12% CAGR total returns are expected from such a company today.

Think of yield + growth like the Foundation’s “Psychohistory”.

Yes, I really am this much of a nerd😉

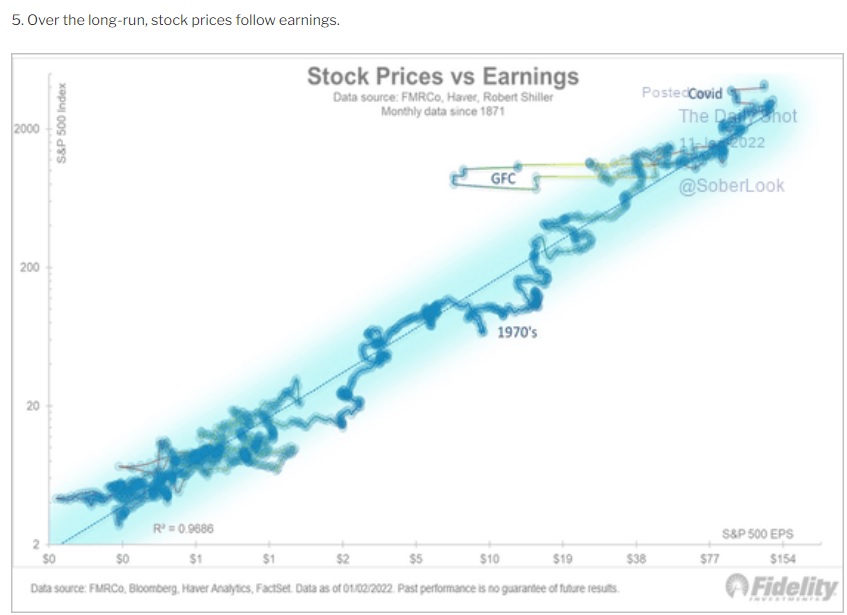

In the short term, most stock returns are driven by luck, momentum, and sentiment. BUT over the long-term? 97% of returns are explained by earnings growth, in other words, fundamentals.

Over 30+ years, using data going back to 1871, 97% of stock returns were pure earnings.

In the short-term? Luck is 12X more powerful than fundamentals, but over the long-term? Fundamentals are 33X as powerful as luck.

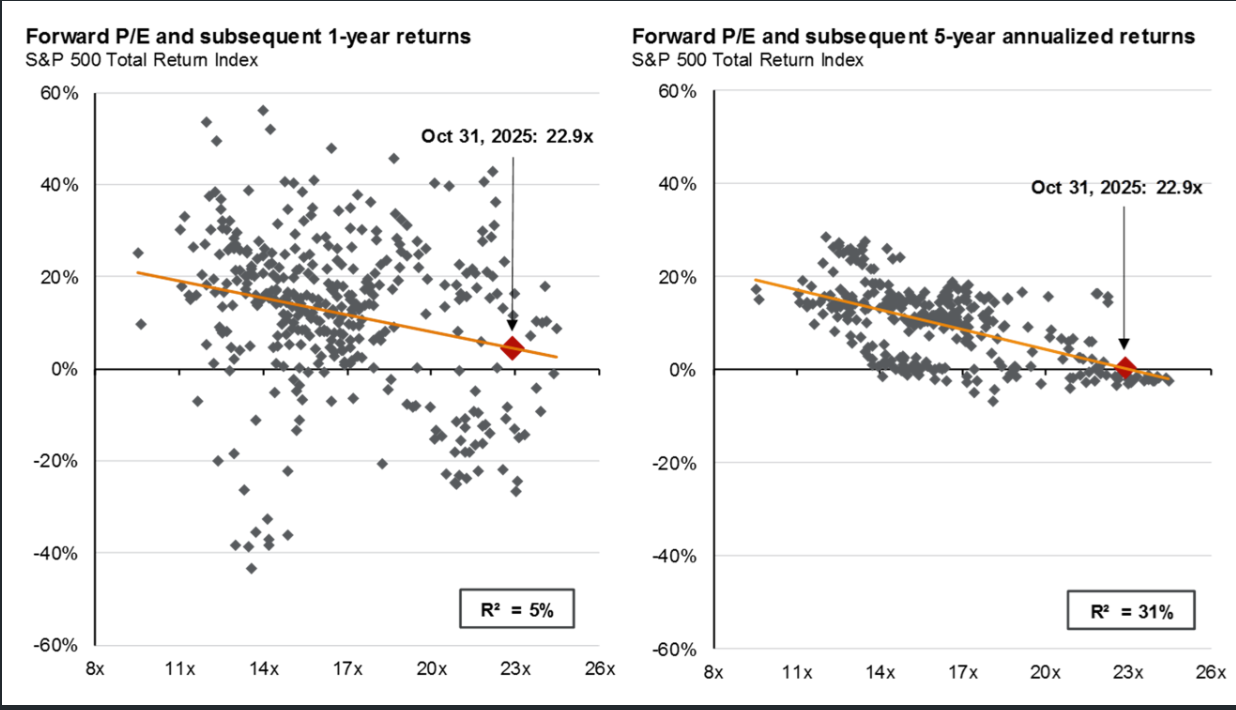

The “Short-Term” Is Actually 5 YEARS or Less!😉

This explains why some blue-chip bear markets last 5 to 7 years: it takes 7 years for the majority of returns (measured by R²) to exceed 50%.

In other words, even for 6 YEARS, the majority of returns are still not explained by fundamentals.

And that’s why value investing continued to work! Because few investors can, for 4 to 6 years, watch a stock price go sideways (or even down!) even as dividends and earnings keep growing, and think, “The thesis is getting stronger, my risk is going down, I need to keep buying more.”

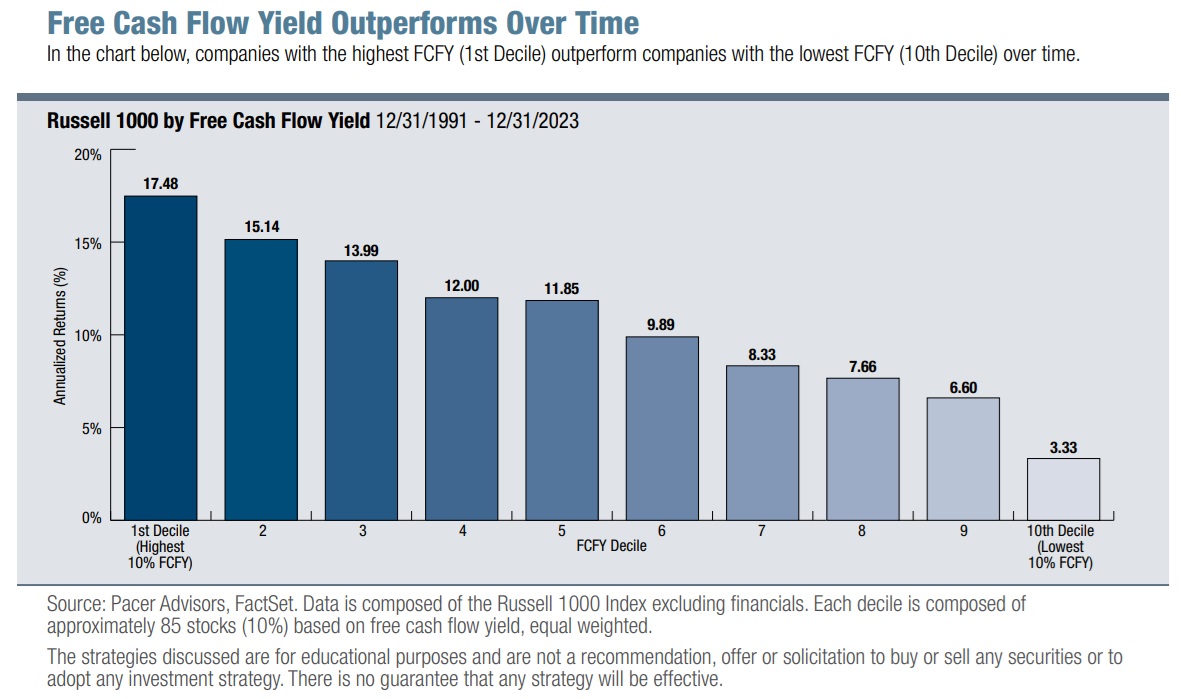

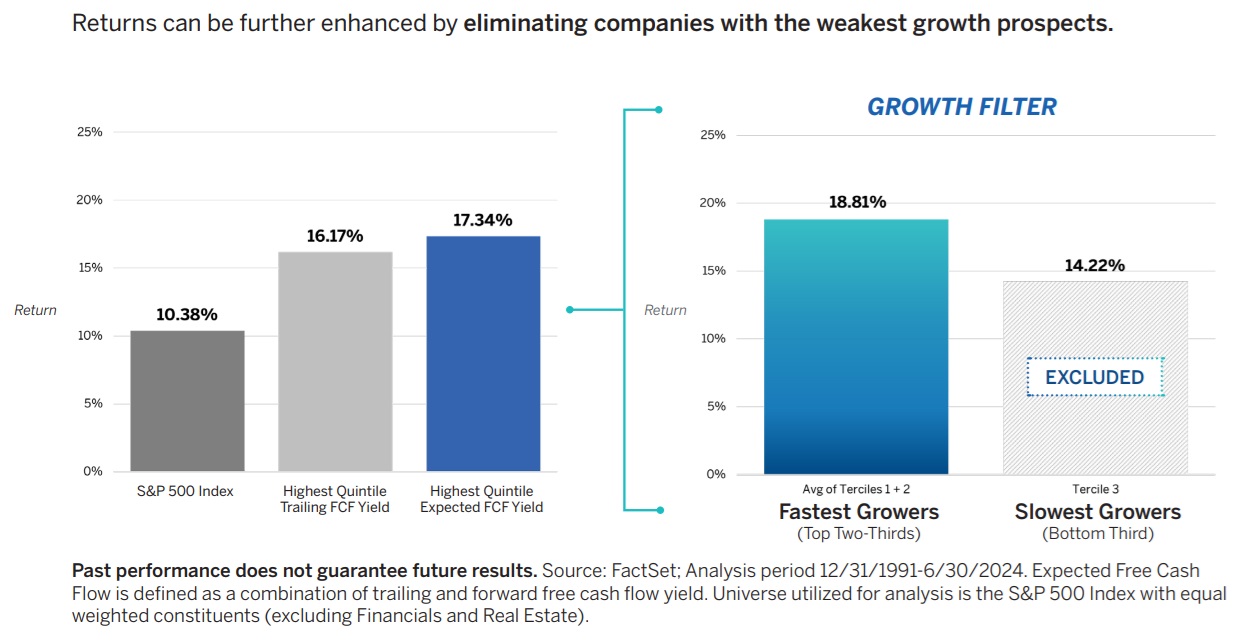

What Happens When You Combine Value + Growth

If you screen out the 33% slowest growers from the highest free cash flow-yielding companies, then the annual returns since 1991 rose to around 19% CAGR —literally Buffett-like returns.

And what does that mean over 33 years?

Growth-Adjusted FCF yield investing: $1 turned into $295. vs $26 for the S&P = 11.2X higher wealth over 33 years.

How many investors dream about a 300X return?! Well, growth-adjusted free cash flow yield investing delivered a life-changing return.

Value never stopped working, if you knew how to measure it correctly😉

OK, but does it still work?

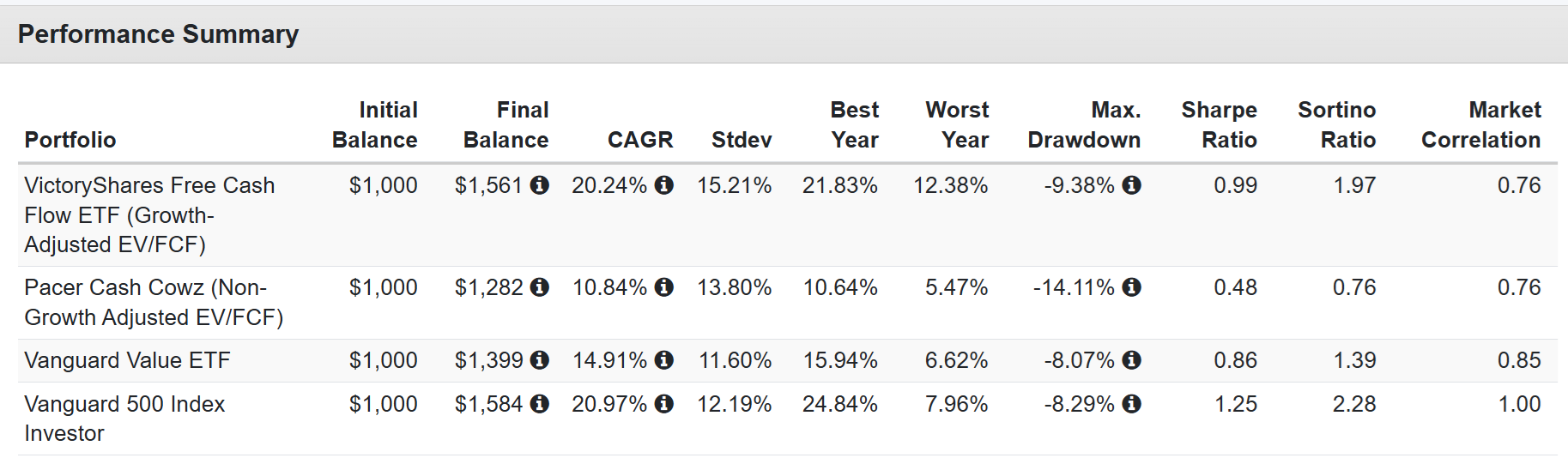

We are almost done with the first generation of our backtesting engine, which will allow you to see how PEGY investing performed over time. BUT here’s some real-world data using the VictoryShares Free Cash Flow Yield (VFLO) ETF as a proxy. Remember the 19% CAGR returns since 1991? How has VFLO done since its inception in July 2023?

Since July 2023 (Entirely In the Age of AI - where growth matters more than ever)

Strategy returns of 19% CAGR since 1991 AND real-world investor returns of 20% CAGR, keeping up with the S&P in a growth-dominated tech bull market.

Meanwhile, ignoring growth? Like the COWZ ETF does? 11% returns, and traditional value? 15% CAGR.

Mind you, 11% and 15% CAGRs are still great historical market-beating returns… but we live in the age of AI, where growth rates are faster. In other words, if beating the market is your goal? Traditional value investing isn’t going to work. Low price to book? Low PE? Sorry, in an age where AI is disrupting so many companies, growth rate changes can make all the difference between buying a “sucker yield” value trap and a Buffett-style fat pitch.

The Growth Boom Could Last Until 2047: So You Better Not Ignore Growth For That Long😉

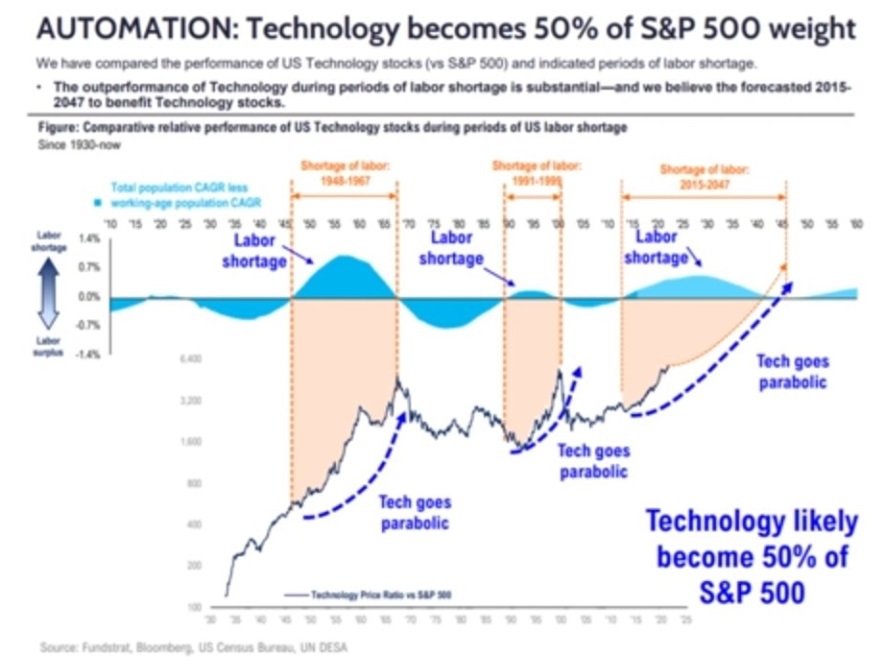

Tom Lee at Fundstrat is a fact-based analyst who has been correct for the last 16 years. He’s someone who looks at first-principles data and, if the numbers check out, believes them.

And based on demographics, specifically lower immigration and falling birth rates, Fundstrat believes the automation boom could last 22 more years.

Citigroup agrees, estimating that robots will be a $7 trillion-per-year business by 2050 and that automation spending (excluding robots) will be around $3 trillion per year.

That’s $10 trillion in AI and Robots due to a shortage of workers. That’s called a secular trend; it’s not something that stock prices or PE ratios will affect. It’s not something that can be changed, by anything for the next few decades.

Only increased immigration could change the number of workers US companies have access to.

And that’s politically not going to happen.

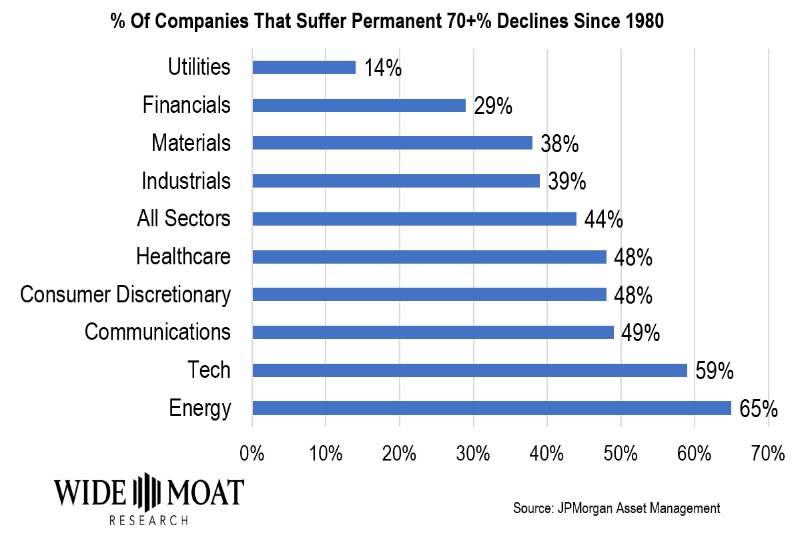

This is why value traps are dangerous. Because if a stock falls 70% or more, there is a good chance (up to 65% depending on the sector) that it will NEVER EVER EVER recover to new highs.

44% of stocks that have ever fallen 70% since 1980 were broken forever, and even after 30 or 40 years, investors were still underwater.

OK, so now that you know why the PEGY ratio exists, and why value investing must take growth into account (because if a company is broken, the PE isn’t going to return to historical levels), let’s see what the fundamentals say about Comcast.

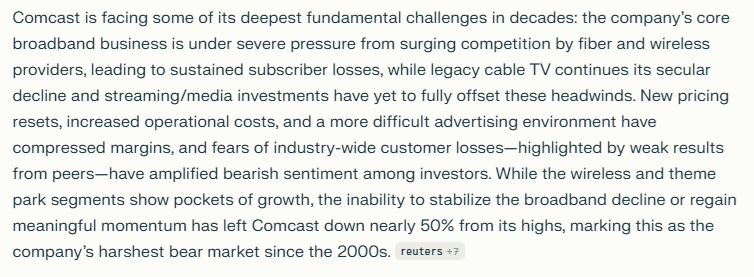

What’s The Matter With Comcast?

There’s the TLDR (Too long, didn’t read) on Comcast, which is suffering from a perfect storm of disruption, including competition in broadband from the likes of T-Mobile, which now offers 5G broadband.

Cord-cutting is a secular trend that has shattered the traditional cable business model, which allowed Comcast to grow through acquisition and deliver those historical 15% to 16% CAGR annual rolling returns over the last 35 years.

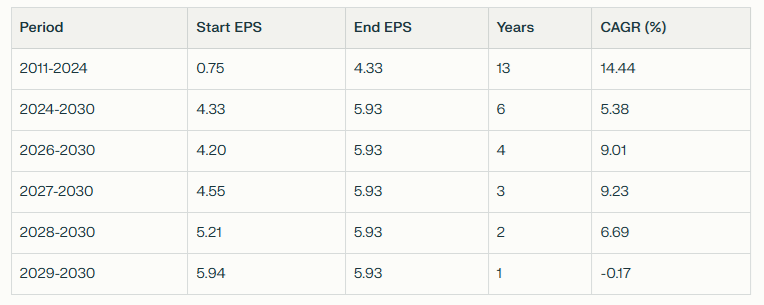

Oh boy, 1.1% median long-term growth consensus from all 32 analysts (range of -2% to 9% CAGR long-term growth).

OK, but how does that compare to recent history?

Comcast’s Growth Rates Might Be Down 66% (or more)

OK, so what does this mean?

Comcast is trading at 6.6X forward earnings, which seems like a steal. BUT its EV/FCF is 12, thanks to all the debt it has (cable is a debt-heavy industry).

OK, so is that a good deal? IF CMCSA grows as expected by 2030 (a big if), it might be trading at 9.9X EV/FCF. Is that good? Is it a Buffett-style “fat pitch”?

Comcast’s free cash flow is expected to accelerate despite the earnings growth falling to near zero. That’s due to buybacks averaging about $10 billion per year, which is about 10% of shares outstanding.

In other words, Comcast’s thesis has now evolved into “The earnings and free cash flow will grow at inflation rates and we’ll buyback so much stock that at current valuations, we can drive 12% to 13% annual growth in free cash flow per share.

The company is currently priced for 4% growth, while analysts expect free cash flow per share to grow 3X as fast.

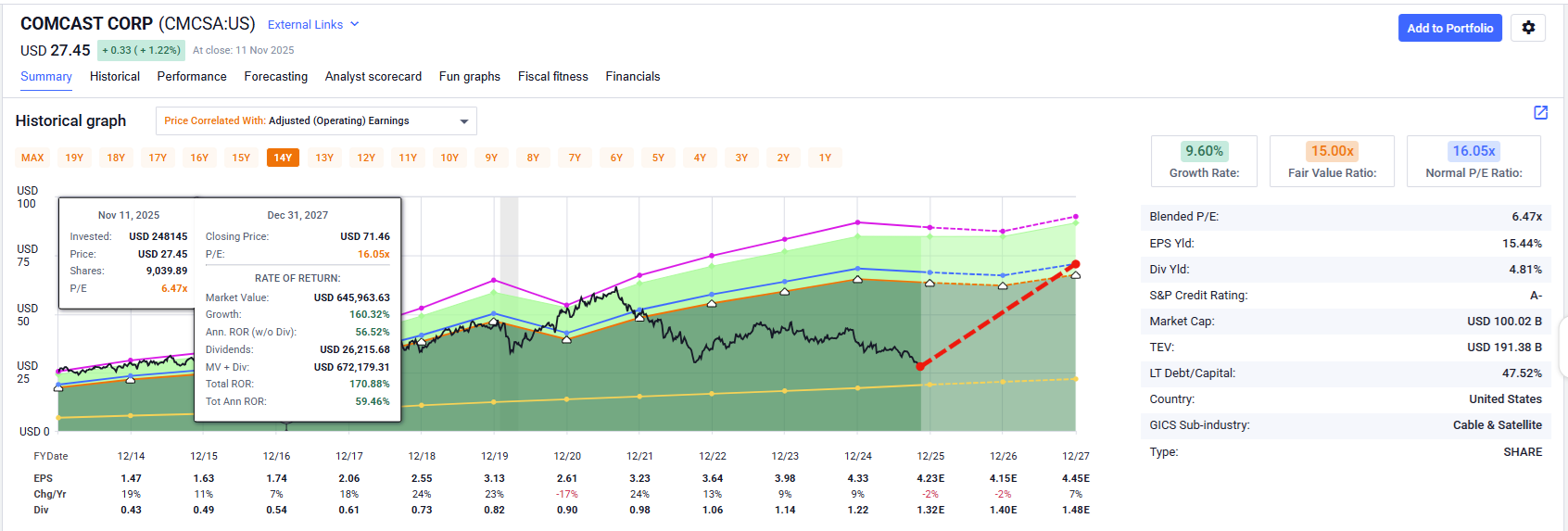

Non-Growth Adjusted Return Potential

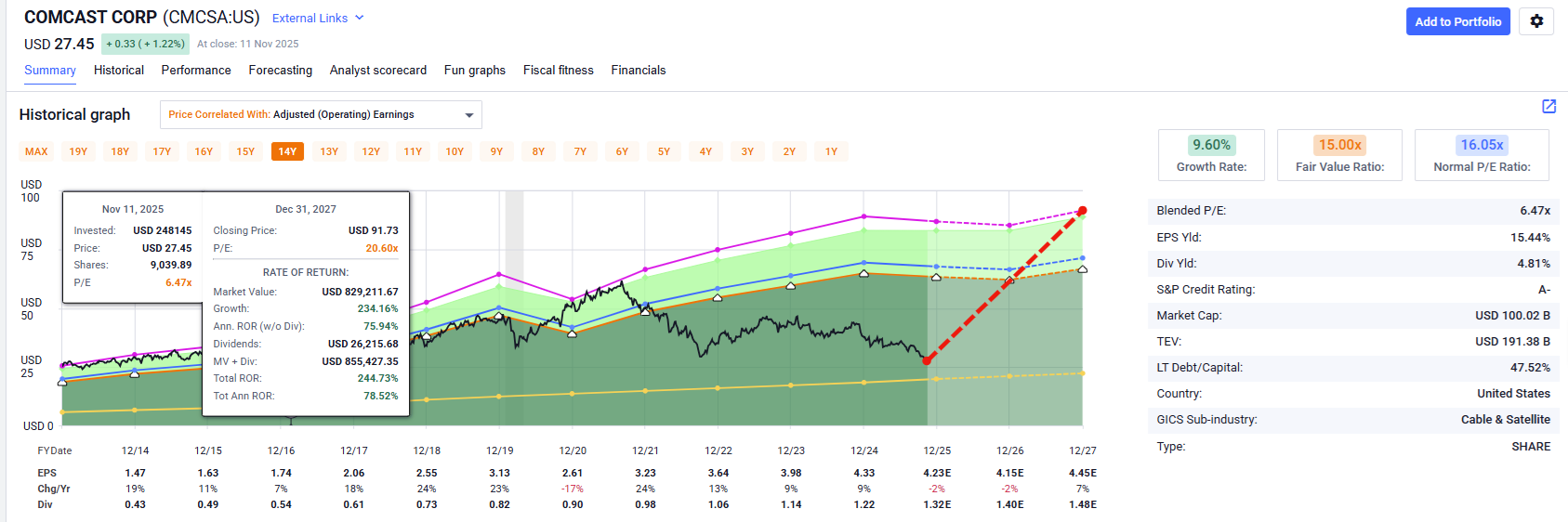

Growth Adjusted Return Potential (Super Buyback Thesis)

The only warning I would say to anyone anticipating the PEGY-like model returns is to remember that the CMCSA thesis is based on 12% to 13% FCF/share growth (10% of which is buybacks).

In other words, AT TODAY’S VALUATION CMCSA can afford to buy back so much stock at the best valuation in 20 years, that these numbers seem reasonable.

At a more normal valuation, CMCSA’s growth outlook could decline significantly, from 12% to 6%, and the 5% yield you lock in today would mean 10% to 11% long-term returns.

Good, but not necessarily great.

In contrast, today the long-term return potential looks closer to 18% due to that 10% annual buyback boost.

It’s Always And Forever A Market Of Stocks, Not A Stock Market

The median S&P stock is on the verge of a bear market while the S&P is 2% off its highs.

Value Stocks Are Still Cheap…And Not Just The Value Traps😉

Keep in mind the ZEUS portfolio is 20% undervalued according to Morningstar and is 50% undervalued based on its PEGY ratio.

In other words, nothing we own in the ZEUS LEGACY family charity hedge fund is overvalued, it’s all a deep value portfolio (PEGY discount of at least 20%). BUT if you are someone who just can’t bring yourself to buy stocks going up (that’s what they do, but I understand the sentiment) well, look at all the world-beater value stocks that I own that you could buy with confidence.

Whether you’re a low PE investor (GPN) or a hyper-growth investor (MELI) or a high-yield dividend aristocrat investor (EPD), there is always something on sale. And even if you are uncomfortable with the age of AI, and prefer to just ignore the growth names, you can safely do it. You just have to understand that all the headlines you’re seeing? That the bubble in calling market bubbles, it’s all based on click-bait and max engagement.

It’s social media algos feeding you scary headlines beause you clicked on them in the past and now it FEELS like this is like 1999.

But when you dig down? Into the actual data? You can see the details are nothing like 1999.

And the details make all the difference, the context matters, and never forget one of the most important non-investing investing quotes of all😉

Right now 1.1 billion humans on earth are obese…they are literally dying of too many calories.

At the same time, 673 million are food insecure and literally have to worry about feeding their children.

Both facts are true…at the same time.

“Hunger is no longer a problem! Look at all the fat people!” but “Almost as many people don’t have enough to eat!”

All while 25% to 33% of global food production goes to waste each year. In other words…the world is infinitely more complex than you can imagine…but living well, and investing wisely, and being a happy person? That’s simpler than you think.

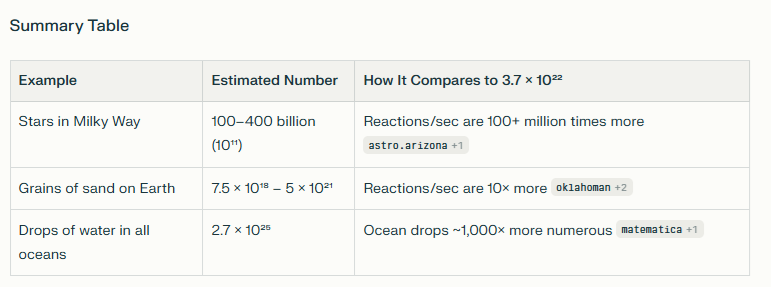

Did you know that in each of the 75 trillion cells in your body (half of which are bacteria in your gut) have about 1 billion chemical reactions per second?

That’s 3.7 × 10 ^ 22 chemical reactions per second in your body.

What 3.7 × 10 ^ 22 Chemical Reactions In Your Body PER SECOND compares to.

Ever wonder, “Why can’t my doctor tell me what drug will make me feel better?” Because in about 20 minutes there are as many chemical reactions happening in your body as there are drops of water in all the oceans of the world!😂

That your doctor and medical science can predict or cure anything is a testament to all we’ve learned, even though we will never learn everything there is know about the human body.

Though maybe one day AI super intelligence can figure it out…after all, haven’t you heard, nothing is beyond the capabilities of AI😉😂

Scientists estimate that we understand very little about the observable universe and 95% of the universe is dark matter and dark energy, which we only know is there because of their gravitational impact on the observable universe.

In other words, we know a small fraction about a small fraction of what there is to know in our universe. And there might be an infinite number of universes in the multiverse. And an infinite amount of multi-verses in the omni-verse.

Basically, the more you learn about anything, the more in awe of how much you (and all of civilization) don’t know you should be.

Welcome to the age of AI…welcome to what it means to be alive in this remarkable, awe-inspiring, and often terrifying universe😉

You don’t have to be religious to see the beauty and wisdom in that passage.

It’s great advice for living in general. Understanding that all the facts we have, all the models we rely on, it’s all the best we can do at any given moment.

The “perfect” decision about anything is almost unknowable, all you can do is try to be optimal. Always try to be as perfect as you can with the limited knowledge we have in this second, and be humble enough and ready to change your mind when the facts change (and they will change, the only constant is change).

Bottom Line: 3 Things Value Investors Need To Do To Thrive In the Age of AI

Use the right valuation metrics & keep growth in mind.

Stay humble (all models are wrong, but some are useful), be willing to change your mind as the facts change.

Have a sense of humor, because in the absurd age of AI, you have to laught to keep from crying😉😂

My 3 Favorite Age of AI Memes: Embrace the Absurdity And Don’t Forget That Life Is Delightful, Wonderful, and Meant For Joy And Love!

This One’s For You Michael Batnick😉

Michael Batnick keeps referencing Jensen signing a woman’s bra as the “ultimate sign of the top” except it wasn’t😂

My Promise To All My Readers And GNG Members

The age of AI is simultaneously wonderful, terrifying, absurd, awe-inspiring, and confusing.

We’re all on this journey together.

Navigating a world where even the tech experts who have been investing in AI startups are feeling overwhelmed.

But I can promise you that I will be here to help you learn, laugh, and grow rich through all of it.

Not because I have a crystal ball, but because me and my incredible team of computer nerds and financial geeks (three guys and some algos, and now only one of us can’t code)🤣😂 are always learning, improving and fanatically devoted to the truth, as best as we can ever know it.

We’re not just doing this for you, we’re doing this for our families, and for me, most of all, my kids, and all the kids of the world we’re going to help over the coming years and decades.

Thanks for reading, and I hope you’ve learned a lot, got some good investing ideas, and had some fun. Because we’re all on the ride together, it’s not one we can get off. If we follow the math and do the right things whenever we can, then as disciplined financial scientists, we can achieve miraculous things for our families and our world.

The right people, with the right mission, and the right math, can accomplish almost anything!

“If it doesn’t defy the laws of physics, engineers will find a way,” Peter Diamandis.