Today is a hectic day for me (5 meetings!), so I’m using Gemini 3 Pro Deep Research to help create a similar article to the Salesforce summary article.

The feedback from this article was very positive, so I’m trying it again on the most requested company at the moment.

As always I’ll begin with the human part of the analysis, and the full research report, based on the entire FactSet Research database on a company (all analyst consensus estimates) and Morningstar’s Dan Romanov’s expert insight, and the dozens of sources located by Gemini 3 Pro (world’s #1 AI model) creates a highly useful “Best available data we have today” look at a company (including the risk profile).

PEGY Analysis

A Primer On What PEGY Is And Why It’s Useful

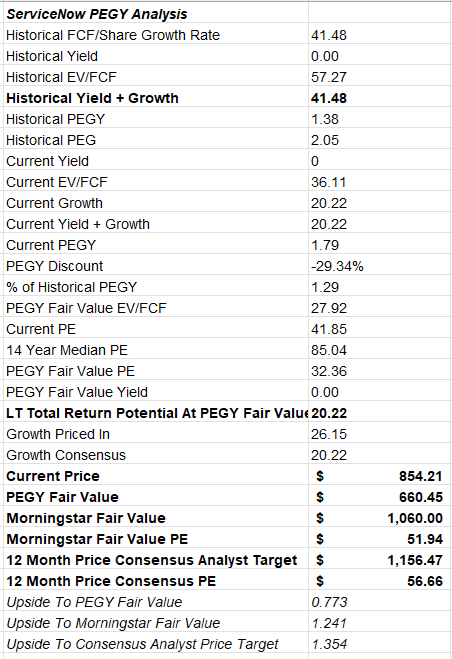

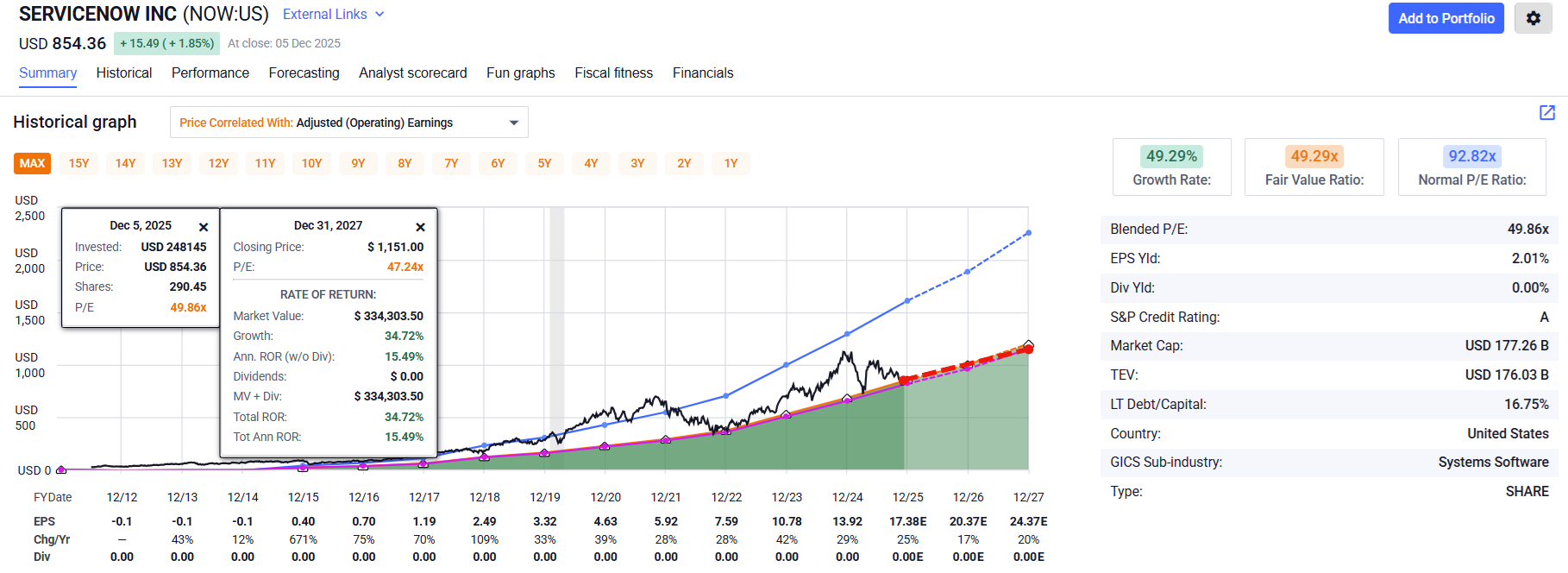

What the PEGY report is telling us is that while NOW is trading at a relatively low 41 PE compared to its historical 85, that decrease MIGHT be fully explained (and then some) by the roughly 50% decline in FCF/share.

Analysts and Morningstar think it’s still worth 52 to 57X earnings, WHICH might not be as crazy as it sounds. After all, the historical long-term average PE for Costco is 35, and that’s growing at 10% over time.

With a subscription Software as a service (SAAS) business model that’s roughly as stable as Costco’s subscription revenues, but with growth that’s 2x higher, you could potentially argue that NOW at 41X earnings is a reasonable buy.

FAST Graphs Analysis

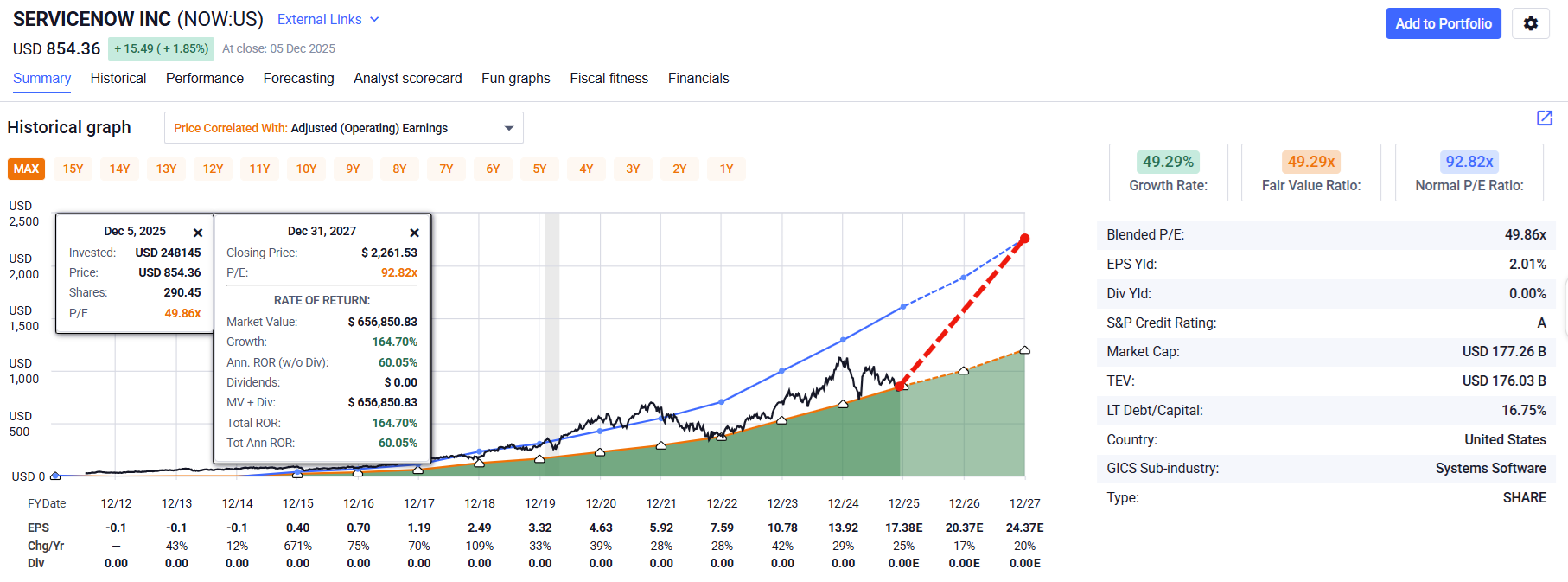

Non-Growth Historical PE Vs Current PE

165% return potential through 2027 = 60% CAGR

Here is why PEGY is useful: if you look at a company’s historical PEs and ignore the slowdown in growth, you might think that NOW has Medallion Fund-like return potential (3X Buffett’s historical returns). Obviously, that’s not likely to be true since the last time NOW traded at its historical average PE was back in 2021.

That was during the Post-Pandemic stimulus-driven speculative mania (SPACs & Meme Stock era).

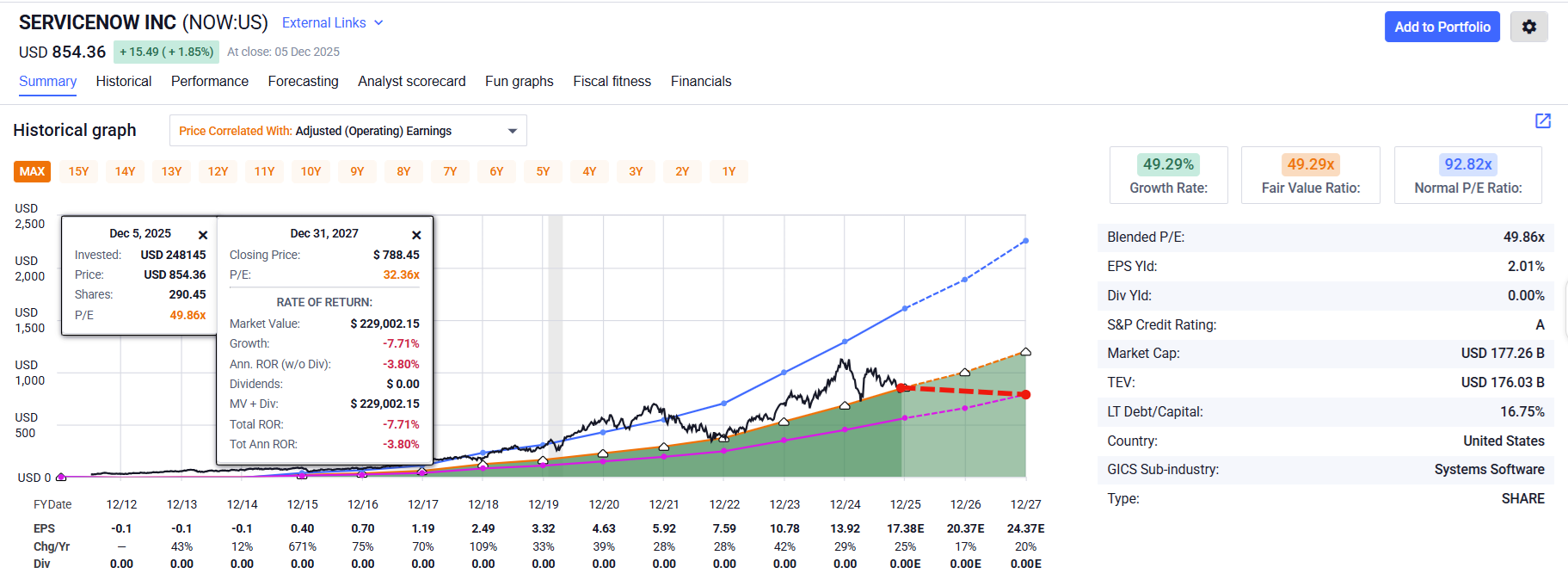

PEGY (Growth Adjusted)

-8% total return potential through 2027 = -4% CAGR.

With a growth rate that has fallen significantly from its long-term average, NOW appears to be speculative, with Morningstar estimates based on discounted cash flow models (where the discount rate is an educated guess) and analysts largely basing their forecasts on momentum.

Morningstar Fair Value

48% total return through 2027 = 21% CAGR

Morningstar is implying a 21% CAGR in Buffett-like returns over the next two years, but again, that’s assuming 52X earnings is the new long-term normal for a slower-growing NOW.

PEGY analysis indicates that 33X earnings are the fair value.

15% to 20% CAGR growth rates for Mag 7 generated an average PE of 25 over the last decade.

Morningstar now expects 17% to 20% CAGR growth on Mag 7 to generate a 35 long-term fair value PE.

In other words, the Morningstar and analyst consensus, while not impossible, is speculative and based on sector PEs rather than NOW’s own historical growth-adjusted objective and market-determined fair value.

Analyst Consensus 47 PE Fair Value

35% total return through 2027 = 15% CAGR

When analysts put out a $1,156.47 median 12-month price target, it implies that a year from now, NOW will be trading at a forward PE of 47X, which is still above the PEGY fair value of 33.

However, if NOW ends up trading flat for 2 years? Or is it down 8% 2 years from now? If it grows as currently expected, AND the growth outlook (20% CAGR) remains the same as today? Then that would be 100% justified by fundamentals.

In other words, if NOW is down 8% 2 years from now, and someone asks, “Is NOW a good buy today”? The answer will be that fundamentals justified the 3-year bear market, and at a 33 PE, it’s merely fairly valued, with about a 20% CAGR and long-term return potential.

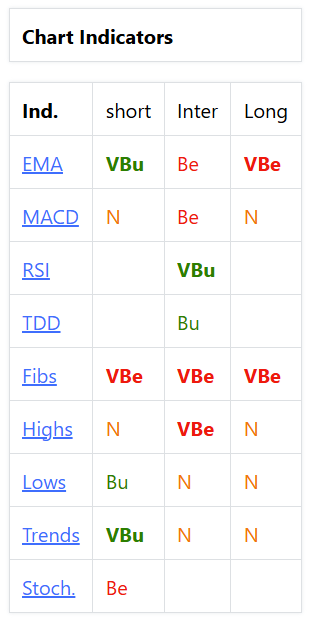

Technical Indicators: What Do The Trading Algos Think?

The technicals on NOW indicate it likely bottomed a few months back around $800, BUT the rally is likely running out of steam in the short term.

There is a lot of tough resistance around $864 to $893 for NOW to break through, and as it approaches those levels, there will be algo selling pressure.

So, from a purely fundamental perspective, NOW is a great company that MIGHT potentially make 15% to 20% CAGR returns in the next 2 years, BUT there is a lot of short-term to potential medium-term headwind because there is no historical evidence that NOW growing at 20% CAGR is worth more than 33X earnings.

Full Report Courtesy of Gemini 3 Pro Deep Research + FactSet + Morningstar

ServiceNow (NOW): The Operating System for the Intelligent Enterprise – Comprehensive Investment Report (2025-2030)

One Sentence Summary ServiceNow is transitioning from a dominant IT service management vendor into the central "AI Operating System" for the Global 2000, leveraging its "Platform of Platforms" architecture to capture a $275 billion total addressable market by orchestrating autonomous agents, modernizing legacy ERP cores, and sustaining a "Rule of 50" financial profile through 2030.

TL;DR Summary

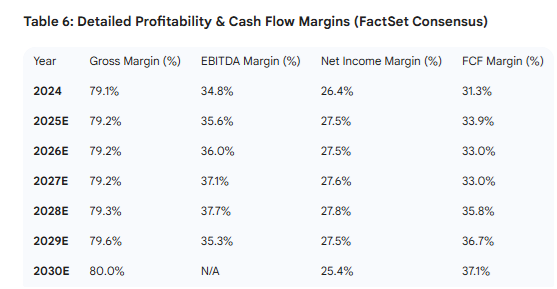

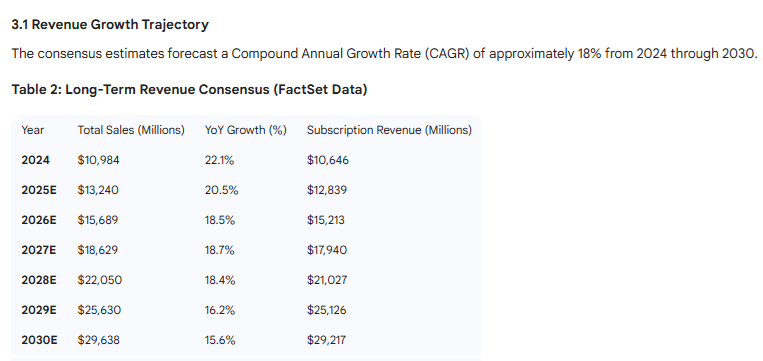

Financial Consensus: FactSet data projects ServiceNow to nearly triple revenue from ~$11 billion in 2024 to $29.6 billion by 2030, maintaining an 18% CAGR while expanding Free Cash Flow margins to 37%, confirming its status as a rare "Rule of 50" compounder at scale.

AI Monetization: Unlike peers struggling to monetize Generative AI, ServiceNow’s "Pro Plus" SKU—commanding a 30-60% price uplift—is rapidly gaining traction because the platform's single data model allows "Now Assist" to execute complex actions across silos rather than merely summarizing text.

Strategic Pivot: The company has successfully opened a massive new Total Addressable Market (TAM) in Finance and Supply Chain workflows by partnering with ERP giants; this "Clean Core" strategy allows enterprises to innovate on ServiceNow without customizing the underlying ERP, securing its role as the indispensable C-suite engagement layer.

Defensive Moat: As enterprises face "AI agent sprawl," ServiceNow’s introduction of the AI Control Tower positions the platform as the governance layer for all enterprise AI—regardless of vendor—creating a new form of vendor lock-in based on compliance, observability, and risk management.

Competitive Edge: While Salesforce’s "Agentforce" competes for customer-facing interactions, ServiceNow’s architectural advantage lies in "middle-office" orchestration where complex, cross-departmental workflows (IT, HR, Legal, Procurement) interact, a domain where CRM-centric data models struggle to compete effectively.

Valuation Reality: Trading at a premium ~76x 2024 P/E and ~19x sales, the stock is "priced for perfection," meaning the primary investment risk is not business failure but valuation compression if subscription revenue growth decelerates below 20% or if the pricing transition causes short-term volatility.

Pricing Paradox: A critical long-term risk involves the deflationary nature of Agentic AI; if ServiceNow’s agents successfully reduce the need for human service desk workers, the company must successfully pivot to volume-based "Assist" pricing to offset the potential erosion of its core seat-based license revenue.

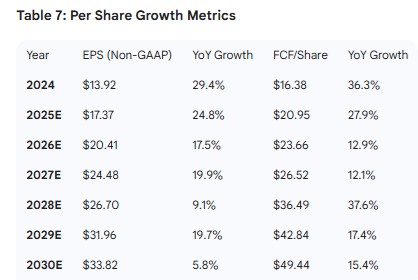

Long-Term Return: With a projected 2030 EPS of $33.82 and Free Cash Flow per share approaching $50, ServiceNow offers a pathway to stable double-digit annualized returns, provided it maintains its leadership in the "AI-first" re-architecture of enterprise software stacks and successfully navigates the consumption pricing shift.

A Table Is Worth A Thousand Words

1. Executive Summary: The Thesis for the "AI Operating System."

The enterprise software landscape is undergoing its most significant structural shift since the transition to the cloud. As organizations move beyond simple digitization toward autonomous operations, the value proposition of software is shifting from "systems of record"—databases that store information—to "systems of action"—platforms that execute work. In this new paradigm, ServiceNow (NOW) has emerged not merely as a participant but as the potential architect of the autonomous enterprise.

This report posits that ServiceNow is uniquely positioned to become the "AI Operating System" for the Global 2000. While the market historically views ServiceNow as an IT Service Management (ITSM) tool, the company has successfully executed a "land and expand" strategy that now touches every corner of the enterprise, from Human Resources and Customer Service to the very core of Finance and Supply Chain operations.

The investment thesis rests on three pillars of durability that extend through 2030:

The Architectural Moat (The CMDB): Unlike competitors who have built their platforms through disparate acquisitions, ServiceNow relies on a single code base and a single data model. This Configuration Management Database (CMDB) provides the necessary context for Artificial Intelligence. An AI agent cannot fix a server or route a supply chain exception if it does not understand the relationships between assets, people, and business processes. ServiceNow owns this map.

The "Clean Core" ERP Strategy: Rather than competing directly with SAP or Oracle to replace the general ledger, ServiceNow has positioned itself as the engagement layer that sits above these legacy systems. By enabling the "Clean Core" strategy—where enterprises keep their ERPs standard and build custom workflows on ServiceNow—the company has unlocked billions in new Total Addressable Market (TAM) without the friction of "rip-and-replace" sales cycles.

Financial Durability: The FactSet consensus data provided for this report paints a picture of exceptional financial health. Revenue is projected to grow from $10.98 billion in 2024 to $29.64 billion in 2030. This trajectory is supported by a transition to high-margin consumption pricing ("Assists") and a deepening entrenchment in the C-suite via the AI Control Tower product.

However, this growth is priced at a premium. With valuation multiples far exceeding software averages, the stock demands flawless execution. The primary risk to the thesis is the "Seat-Based Pricing Paradox"—the potential for AI to cannibalize the very user seats that generate ServiceNow's current revenue. The success of the investment depends entirely on the company's ability to navigate the transition from monetizing humans to monetizing digital agents.

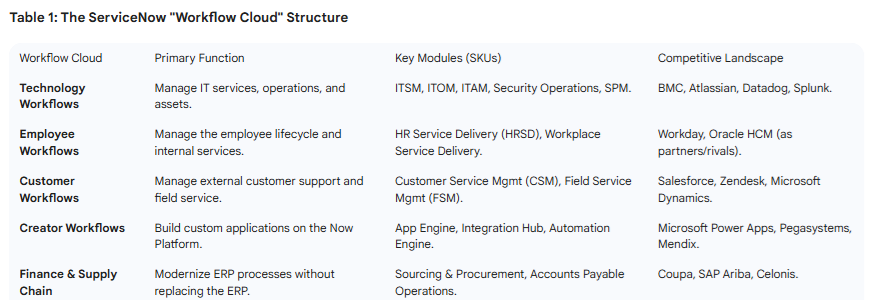

2. Business Overview: The "Platform of Platforms."

ServiceNow was founded in 2004 by Fred Luddy on a simple yet revolutionary premise: that a better technology platform could improve how work flows. What began as a cloud-based tool for IT help desks to manage tickets has evolved into a comprehensive enterprise platform that orchestrates work across the entire organization.

2.1 The Core Philosophy: A Single System of Action

The central tenet of ServiceNow’s business model is the "Platform of Platforms." In a typical large enterprise, data is fragmented across hundreds of systems: SAP for finance, Salesforce for customer data, Workday for HR, and various legacy tools for operations. These systems effectively store data (Systems of Record) but are poor at communicating with one another.

ServiceNow sits above these layers. It does not necessarily seek to replace the system of record; instead, it acts as the connective tissue—the "System of Action." Through its Now Platform, it ingests data from these disparate sources, normalizes it into a single data model, and allows users to build cross-functional workflows.

2.2 The Technical Advantage: The CMDB

The "secret sauce" of ServiceNow is the Configuration Management Database (CMDB). This repository serves as a data warehouse for the enterprise's IT infrastructure. It tracks every server, application, laptop, and software license, along with their relationships.

Why is this critical for the 2025-2030 thesis? Context for AI. Generative AI models (LLMs) are excellent at language but poor at understanding corporate context. If an employee asks an AI, "Why is my email slow?", a generic LLM cannot answer. ServiceNow's AI can look at the CMDB, see that the employee is on a specific Exchange server, note that the server is undergoing maintenance, and provide a precise answer. This contextual awareness creates a defensive moat that chat-based competitors cannot easily bridge.

2.3 The Revenue Model

ServiceNow operates a classic B2B SaaS model.

Subscription Revenue: Accounts for ~97% of total revenue. Contracts are typically multi-year (3 years average) with high renewal rates (consistently 98-99%).

ACV (Annual Contract Value): The primary metric for growth. The company focuses on large enterprises (Global 2000) and is constantly expanding the number of customers paying >$1 million, >$5 million, and >$10 million annually.

The Shift to Consumption: As discussed in later sections, the introduction of AI agents is driving a shift toward consumption-based pricing elements, adding a layer of usage-based revenue to the stable subscription base.

3. Financial Analysis: The Path to $30 Billion (2024-2030)

The quantitative case for ServiceNow is rooted in its ability to defy the law of large numbers. Based on the FactSet consensus data provided, the company is projected to maintain double-digit growth rates well into the next decade, a rarity for a company of its size.

3.1 Revenue Growth Trajectory

The consensus estimates forecast a Compound Annual Growth Rate (CAGR) of approximately 18% from 2024 through 2030.

Analysis of Growth Drivers: The deceleration from 22% to 15.6% is incredibly gradual. This "soft landing" in growth rates implies successful execution on several fronts:

New Product Cycles: The sustained growth in 2027-2028 suggests analysts expect the AI and Finance/Supply Chain products to reach maturity and significant scale during this window, offsetting the natural maturation of the core ITSM market.

Pricing Power: Revenue growth exceeds projected customer count growth, indicating strong pricing power from the "Pro Plus" AI SKUs, which drive higher Average Selling Prices (ASP).

Resilience: Even in the outer years (2029-2030), growth remains above 15%, characterizing ServiceNow as a "durable compounder" rather than a hyper-growth stock.

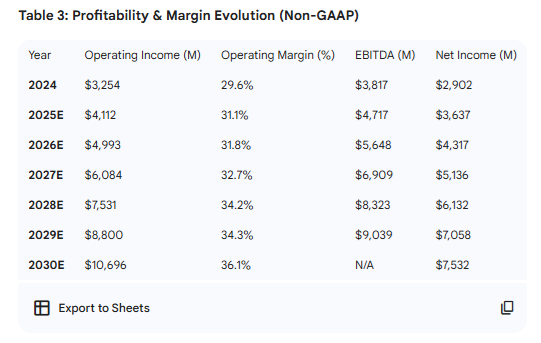

3.2 Profitability and The "Rule of 60."

ServiceNow is not just growing; it is growing profitably. The company is effectively operating at a "Rule of 60" level (Revenue Growth + Free Cash Flow Margin), significantly outperforming the industry standard "Rule of 40."

Insight on Margins: The expansion of operating margins from ~29% to ~36% demonstrates immense operating leverage. As the company scales, Sales & Marketing (S&M) expenses as a percentage of revenue are expected to decline due to the efficiency of cross-selling to the installed base. The "Net Expansion Rate" effectively subsidizes customer acquisition costs. Furthermore, R&D spend, while growing in absolute terms to fund AI development ($4.6B by 2030), will likely stabilize as a percentage of revenue.

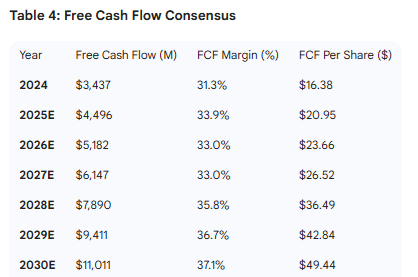

3.3 The Cash Flow Machine

For long-term investors, Free Cash Flow (FCF) is the ultimate truth. ServiceNow is projected to become a cash-generating behemoth.

Strategic Implications of FCF: With FCF projected to cross $11 billion by 2030, ServiceNow will have enormous capital allocation flexibility. This cash pile can be used for:

Strategic M&A: Buying niche AI or vertical software companies to fold into the platform.

Share Buybacks: Offsetting stock-based compensation dilution (historically high for SaaS companies) and potentially reducing the share count to boost EPS. The consensus shows share count dilution stabilizing, aiding the massive jump in FCF per share from ~$16 to ~$50.

4. Deep Research: The AI Pivot – From Generative to Agentic

The single most important variable in the 2025-2030 thesis is Artificial Intelligence. ServiceNow is not merely adding "chatbots"; it is re-architecting its platform to support Agentic AI.

4.1 "Now Assist" and the Pro Plus SKU

ServiceNow was one of the first enterprise software companies to monetize Generative AI effectively. The "Now Assist" family of products is embedded directly into the workflow.

Functionality: It summarizes complex cases, generates code for developers (text-to-workflow), and creates resolution notes for agents.

Monetization Mechanism: These features are gated behind the "Pro Plus" and "Enterprise Plus" SKUs.

Pricing Power: Research indicates these SKUs command a 30% to 60% price uplift over standard editions. This is a massive lever for revenue growth without needing to add a single new customer logo.

Traction: In Q3 2025 earnings, management noted that Now Assist Net New ACV (Annual Contract Value) beat expectations, putting the company on track to exceed $500M in AI ACV in 2025 and aiming for $1B by 2026. This is the fastest-growing new product in the company's history.

4.2 The "Assists" Consumption Model: A Hedge Against Deflation

A critical and often overlooked detail is the introduction of "Assists" as a metering unit.

The Risk: If AI is successful, it reduces the need for human agents. Since ServiceNow charges per seat, successful AI could theoretically cannibalize revenue (fewer seats needed).

The Solution: ServiceNow introduced "Assists." Customers receive a baseline allowance of AI interactions (Assists) with their subscription. If usage exceeds this (e.g., an automated agent resolves 10,000 tickets autonomously), the customer purchases "Assist Packs."

Implication: This hybrid model (Subscription + Consumption) hedges the company against seat erosion. It allows ServiceNow to capture value from the work performed by the software, not just the humans using it. In Q3 2025, consumption of AI Agent Assist grew 55x, validating this model.

4.3 The AI Control Tower: The Governance Layer

As enterprises adopt AI, they face "Agent Sprawl"—hundreds of disparate AI agents from Microsoft, Salesforce, and open-source models running unchecked.

The Product: ServiceNow launched the AI Control Tower to solve this. It serves as a centralized dashboard to track, monitor, and govern all AI agents across the enterprise.

The Strategy: By integrating with the CMDB, the Control Tower maps AI agents to the business processes they support. It monitors for hallucinations, compliance risks, and ROI.

The Moat: This positions ServiceNow as the "manager" of the AI ecosystem. Even if a customer uses a Microsoft Copilot agent, ServiceNow wants to be the platform that governs that agent. This is a defensive masterstroke, preventing disintermediation by LLM providers.

5. Strategic Growth Vector: "Clean Core" ERP Modernization

While AI grabs the headlines, the "Clean Core" strategy targeting Finance and Supply Chain workflows is the stealth driver of the $30 billion revenue target.

5.1 The Problem with Legacy ERP

Global enterprises run on SAP and Oracle. Over the last 20-30 years, these companies heavily customized their ERPs to fit their specific business processes.

The Trap: These customizations act as "concrete," making it impossible to upgrade the ERP to the cloud (e.g., moving to SAP S/4HANA) without breaking the business. This is known as "technical debt."

The Dilemma: CIOs are terrified of multi-year, billion-dollar ERP migration failures.

5.2 The ServiceNow Solution

ServiceNow, in partnership with ecosystem giants like Deloitte and SAP itself, proposes the "Clean Core" strategy.

Stop Customizing the ERP: Keep the ERP "vanilla" (standard code).

Move Complexity to ServiceNow: Build all the custom workflows, vendor portals, and procurement approvals on the ServiceNow App Engine.

The Result: The ERP becomes a simple ledger (easy to upgrade), and the complexity lives in ServiceNow (easy to modify).

5.3 Financial Impact

This strategy opens up the Office of the CFO and Chief Supply Chain Officer as major buyers.

Source-to-Pay: Automating the entire procurement lifecycle.

Accounts Payable: Automating invoice reconciliation.

Supplier Lifecycle: Managing vendor onboarding and risk.

Evidence of Success: In recent quarters, ServiceNow has cited massive wins in this segment, including a 70% productivity increase in Accounts Receivable case management for customers. The "Finance and Supply Chain" workflow is becoming a legitimate fourth leg of the stool alongside IT, Employee, and Customer workflows.

6. Competitive Landscape: The Battle for the Enterprise

ServiceNow operates in a "frenemy" ecosystem, integrating with the very companies it competes against.

6.1 ServiceNow vs. Salesforce (CRM)

This is the heavyweight title fight of the decade.

The Battleground: Customer Service Management (CSM).

Salesforce's Pitch: "Agentforce." Salesforce argues that customer service should be centered around customer data (Customer 360). Service is an extension of Sales and Marketing.

ServiceNow's Pitch: "Service Operations." ServiceNow argues that in complex B2B industries (banking, telco, healthcare), a customer problem usually stems from a broken process or asset (e.g., a server down, a lost shipment). Therefore, service should be connected to Operations (IT/Supply Chain), not Sales.

The Verdict: Salesforce wins in B2C and high-volume, low-complexity support. ServiceNow wins in B2B and regulated industries where resolving an issue requires cross-departmental work. The FactSet consensus shows ServiceNow growing faster than Salesforce, suggesting this "middle office" strategy is resonating.

6.2 ServiceNow vs. Workday (WDAY)

The Dynamic: Workday owns the employee record (HCM). ServiceNow owns the employee experience.

The Friction: Workday is trying to expand into "employee experience" with its own portals. ServiceNow is holding the line by aggregating all services (IT, HR, and Legal) into its Employee Center. An employee doesn't want to log into Workday for PTO and ServiceNow for a laptop; they want one portal. ServiceNow is winning the "portal wars" due to its broader scope.

6.3 ServiceNow vs. Atlassian (Jira)

The Threat: Atlassian (Jira Service Management) disrupts from below. It is cheaper, easier to set up, and beloved by developers.

ServiceNow's Defense: ServiceNow dominates the large enterprise (Global 2000), where compliance, governance, and the CMDB are non-negotiable. Atlassian struggles to move up-market into complex, non-IT enterprise workflows.

7. Valuation and Investment Scenarios

ServiceNow is a premium asset with a premium price tag. Understanding the valuation requires looking beyond simple P/E ratios to Free Cash Flow yields and growth-adjusted metrics.

7.1 Historical Valuation Context

Current P/E (Forward): ~45x-50x.

Current EV/Sales: ~12x-14x.

Historical Norms: ServiceNow has historically traded at >10x sales due to its high growth and predictability.

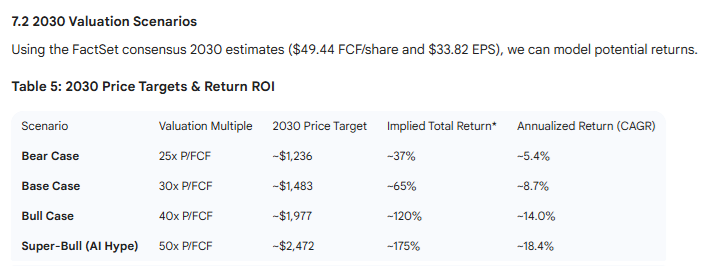

7.2 2030 Valuation Scenarios

Using the FactSet consensus 2030 estimates ($49.44 FCF/share and $33.82 EPS), we can model potential returns.

Note: Assumes entry price of ~$900. Total return excludes dividends (ServiceNow does not currently pay one).

Investment Implication: The "Base Case" return of ~9% CAGR might seem modest for a tech stock, but it represents risk-adjusted durability. The probability of ServiceNow hitting these numbers is high given its sticky customer base. The "Bull Case" relies on the market maintaining a premium multiple for AI leaders. If ServiceNow proves to be the definitive "AI OS," a 40x FCF multiple in 2030 is plausible, offering mid-teens annualized returns.

8. Risk Analysis: What Could Break the Thesis?

Despite the bullish consensus, significant risks exist.

8.1 The "Seat-Based" Deflationary Spiral

This is the structural risk of the AI era.

Mechanism: If ServiceNow's "Agentic AI" is truly effective, it will automate Tier 1 and Tier 2 support tasks. Enterprises will inevitably reduce their headcount of human support agents.

Impact: ServiceNow charges per human user. A 20% reduction in global support staff could mean a 20% headwind to seat expansion.

Mitigation Failure: If the new "Assist" consumption pricing does not scale fast enough to offset the lost seats, revenue growth could stall. This transition period (2025-2027) introduces model volatility.

8.2 Adoption Friction & "Shelfware"

Pro Plus Fatigue: Customers are being asked to pay 50% more for AI features. If the ROI isn't immediate and obvious, CIOs—facing tight budgets—might churn off the "Plus" SKUs, reverting to standard editions. The current "hype cycle" might be pulling forward demand that won't sustain.

Complexity: As ServiceNow expands into ERP and Supply Chain, the platform becomes massive and complex. Implementation times could lengthen, and the "ease of use" advantage could erode, making it vulnerable to simpler, nimbler competitors like Atlassian.

8.3 Macro-Economic Sensitivity

IT Budgets: While ServiceNow is "mission critical," the expansion modules (Creator, Governance) are often discretionary. In a recession, net retention rates could dip below the historic 115% threshold as customers consolidate spend.

9. Conclusion: The Long-Term View

ServiceNow represents a rare combination of offensive growth and defensive durability. It has successfully navigated the transition from a single-product company (ITSM) to a multi-product platform. The current pivot to becoming the AI Control Tower for the enterprise is the logical next step in this evolution.

The financial data support a bullish long-term view, projecting a company that will triple in size and become a cash flow machine by 2030. While the current valuation captures much of this optimism, the "Clean Core" ERP strategy and the consumption-based AI model provide credible upside optionality that is not fully appreciated by the market.

Final Recommendation: For investors with a 5+ year horizon, ServiceNow is a foundational holding for the AI era. It is the "pick and shovel" play for enterprise automation—not the flashy LLM builder, but the indispensable platform that manages the agents, governs the risks, and orchestrates the work of the future.

Sources

Source: FactSet Consensus

download (98).xlsx

How ServiceNow Is Turning AI Strategy Into Real Revenue - MarketBeat

Now on Now ERP Modernization - ServiceNow

Salesforce Agentforce vs ServiceNow AI: A Full Comparison - EmpowerCodes Technologies

Can Workflow Adoption Drive NOW Stock in 2026 Post 25% Drop? - Finviz

What is ServiceNow? A 2025 Guide for Decision-Makers - Aelum Consulting

What is ServiceNow? Explained Simply for Beginners - YouTube

How Does ServiceNow Make Money? ServiceNow Business Model In A Nutshell

ServiceNow's $1B AI Plan: What It Means for Customers - YouTube

ServiceNow Financial Results for Q3 2025

ServiceNow (NOW) Q3 2025 Earnings Call Transcript | The Motley Fool

ServiceNow (NOW.US) Q3 Earnings Call: Assist Growth Exceeds Expectations, Targeting Over $500 Million by Year-End

ServiceNow Pricing Guide (2025): Costs, License Types & Hidden Fees - Hiver

ServiceNow AI Control Tower: Govern any AI at Scale

Maximizing ERP Value with ServiceNow & SAP Integration - Rimini Street

Agentforce vs. ServiceNow: A Head-to-Head Comparison - Salesforce

Workday Vs. ServiceNow: The Big Shift

Is ServiceNow AI good? An honest review for 2025 - eesel AI

What does ServiceNow do - in simple terms - The Cloud People

Exploring Now Assist - ServiceNow

What is Now Assist in ServiceNow? A complete 2025 overview - eesel AI

New research: 6 AI priorities for investment firms - ServiceNow

ServiceNow's SWOT analysis: ai-driven growth propels workflow automation leader's stock

Salesforce vs. ServiceNow Battle Intensifies With Agentforce for IT Services

AI Agents Take Center Stage: Workday, ServiceNow, and SAP Challenge Agentforce - SalesforceDevops.net

From Insight to Action: How ServiceNow AI Agents Are Reshaping Business Operations

Finance & Supply Chain - Knowledge 2025 - ServiceNow

ServiceNow, Inc. (NOW) | The Henry Fund - The University of Iowa

ServiceNow Financial Results for Q3 2025

ServiceNow Q2 2025 Investor Presentation

ServiceNow Q3 2025 Investor Presentation

Events, Webcasts & Presentations - ServiceNow Investor Relations

ServiceNow 1Q25 Investor Presentation

AI Agents FAQ and Troubleshooting - ServiceNow Community

How Are AI Agents Priced - ManoByte

Can Rising Workflow Adoption Push ServiceNow Shares Higher? - Nasdaq

ServiceNow Partners Riding the ITSM Growth Wave in 2024 | SA Global Advisors

ServiceNow's 'Follow the Workflow' Strategy: Building a Multi-Product SaaS Platform

What does ServiceNow do | How does ServiceNow work | Business Model - The Strategy Story

ServiceNow Now Assist for Customer Service Management

How ServiceNow Now Assist Brings AI to IT Service Management - Xavor Corporation

Now Assist | Overview - YouTube

Top 8 ServiceNow Alternatives And Competitors In 2025 - Monday.com

8 Great ServiceNow Alternatives to Improve Your CX - Nextiva

Top 15 ServiceNow Competitors & Alternatives in 2025: Best ITSM Tools Reviewed

Top 10 ServiceNow Alternatives for IT Service Management (ITSM)

ServiceNow ITSM vs. Top Competitors: Choose the Right ITSM Solution with Mergen

Generative AI (GenAI) - ServiceNow

Using AI to unlock growth: A conversation with ServiceNow's Paul Fipps - McKinsey

ServiceNow (NOW): A Leader in the Monetization of Generative AI - Insider Monkey

AI agents bring consumption models to SaaS: Goldilocks or headache?

AI vs. ServiceNow: A Comparative Analysis of Features, Costs, and Scalability in 2025

Now on Now: Transforming our procurement and strategic sourcing workflows - ServiceNow

ServiceNow for Procurement: A Guide to Service Management - Cyber Infrastructure, CIS

Why Data Has Never Mattered More For ServiceNow's AI-Driven Strategy

Summer Reading: Soak up the ServiceNow strategy - CoreX Corp.

ServiceNow Commits to Science-Based Targets and to Achieve Net-Zero Greenhouse Gas Emissions by 2030

Financial Services in the Agentic Corporate Services Era - Workflow™ - ServiceNow

7 Ways AI Will Change the Future of Work by 2030 - Workflow™ - ServiceNow

ServiceNow Reports Third Quarter 2025 Financial Results; Board of ...

ServiceNow (NOW) Q3 2025 Earnings Call Transcript - MLQ.ai | AI for investors

Earnings call transcript: Snowflake Q3 2025 earnings beat estimates, stock rises

ServiceNow Q3 2025 Results Beat Estimates with 21.8% Revenue Growth - IndexBox

ServiceNow Financial Results for Q3 2025

ServiceNow Investor Relations — Overview & Latest Updates

ServiceNow to Announce Q3 Earnings October 29, 2025

ServiceNow to Announce Third Quarter 2025 Financial Results on October 29

ServiceNow Reports Second Quarter 2025 Financial Results

Earnings call: ServiceNow targets becoming top enterprise software firm by 2030

ServiceNow vs Salesforce: A Comprehensive Analysis - Reco AI

A practical ServiceNow AI review for 2025 - eesel AI

ServiceNow 2025 Year in Review: A Year of AI Momentum and Platform Expansion - SDI

The Big ServiceNow AI Experience Announcement: A Closer Look - CX Today

ServiceNow's AI Efficiency Push Has Analysts Targeting Big Gains - TradingView

ServiceNow (NOW) Stock Price Prediction: 2025, 2026, 2030 - Benzinga

ServiceNow (NOW) Stock Forecast and Price Target 2025 - MarketBeat

ServiceNow Stock Prediction: Where Analysts See the Stock Going by 2027 | TIKR.com

NOW Raises '25 Subscription Sales Outlook: Buy or Hold the Stock? - November 12, 2025

Can Workflow Adoption Drive NOW Stock in 2026 Post 25% Drop? - TradingView

Is ServiceNow's AI Push Enough to Support Its Lofty 2025 Valuation? - Simply Wall St News

Is ServiceNow's AI Push Enough to Support Its Lofty 2025 Valuation? - Webull

A Complete Guide to ServiceNow AI Pricing in 2025 - eesel AI

Servicenow ai pricing calculator: A 2025 breakdown of tiers & costs - eesel AI

Finance and Supply Chain - ServiceNow

ServiceNow's Workflow Adoption Rises: A Sign for More Upside? - July 14, 2025

ServiceNow Review: Is It Worth It in 2025? [In-Depth]

Honest ServiceNow Review 2025: Pros, Cons, Features & Pricing - Sprinto

ServiceNow IT Operations Management Customer Reviews 2025 | Systems - Info-Tech

Compare 12 Best FinOps Tools: Features, Price, Pros & Cons

What is a Field Technician? - ServiceNow

List of classes added by the CMDB CI Class Models app - ServiceNow

Multiple Award Schedule - GSA Advantage

Announcing the 2024 ServiceNow partners of the year

Plat4mation Wins the ServiceNow 2024 Reseller Partner of the Year Award

Independent Review of ServiceNow - Third Stage Consulting

6 Reasons CIOs Choose ServiceNow App Engine for Modernization - Rimini Street

ServiceNow IT Service Management Review: 50+ Users Experience Analyzed - Asista

Top ServiceNow Process Mining Competitors & Alternatives 2025 | Gartner Peer Insights

A Closer Look: Celonis, ServiceNow and Find, Frame, Fix

Bridging the gaps: How Celonis drives a predictable supply chain with Process Intelligence and AI

Top Celonis Process Intelligence Platform Competitors & Alternatives 2025 - Gartner

6 Coupa competitors for mid-market and enterprise finance teams - Stampli

ServiceNow Expands Vision For AI Transformation - CX Today

What is responsible AI? - ServiceNow

ServiceNow's AI Game Drives Growth But Valuation Stays Lofty - Finimize

ServiceNow & SAP: Unified Change Management - CoreALM

2026 Trends in SAP® Automation, Modernization, and BTP Adoption - Precisely

How to Transform GBS into a Customer-Friendly Service Organization - SSON

ISG Provider Lens™ Quadrant Report – SAP Ecosystem 2025 - Atos

SAP ERP Integration: Streamline Business Processes Across Platforms - Redwood Software

Plat4mation wins ServiceNow Devvies People's Choice Award

What are ServiceNow AI Agents? With Features + Use Cases - NGenious Solutions

ServiceNow ITOM Pricing - Cost Breakdown & Optimization Playbook - GEM Corporation

What is ServiceNow? Products, Pricing, and Benefits Explained - Cyntexa

An Enterprise Low-Code Leader for 6 Years - ServiceNow Blog

Plat4mation Honored with Prestigious 2025 ServiceNow Employee Workflow Partner of the Year Award

ServiceNow wins ITAM technology award for driving autonomy

ServiceNow Pricing Guide: Custom Quotes for Tailored IT Solutions

AI Risk and Compliance release notes - ServiceNow

ERP Core Modernization - ServiceNow - Deloitte

The clean-core myth: 3 tried-and-tested ways to keep your S/4HANA really clean

SAP Clean Core Strategy Guide: My Practical Steps for 2025

ERP Modernization with SAP & ServiceNow: 2025 Strategy Guide

Now Assist in AI Search FAQ - ServiceNow Community

What are Now Assist Skills and what benefits does GenAI provide? - Teiva Systems

Disney Stock Drops Below $100 As Recession Fears Intensify: Retail Stays Bearish

ServiceNow AI Control Tower: A complete 2025 overview - eesel AI

How Customer Insights Shaped ServiceNow University and AI Control Tower

Why Is ServiceNow AI Control Tower More Than Just Compliance? - Inclusion Cloud

What are your considerations in buying Now Assist? : r/servicenow - Reddit

ServiceNow Products | Read 3343 Reviews on G2

ServiceNow Overview and Interactive Capability Map | PDF | Artificial Intelligence - Scribd

Notice of 2024 Annual Meeting of Stockholders and Proxy Statement - SEC.gov

A practical guide to ServiceNow AI Control Tower lifecycle management - eesel AI

ServiceNow Reports Fourth Quarter and Full-Year 2024 Financial Results

ServiceNow's Q4 2024 Financial Results: A Mixed Bag of Growth and Market Uncertainty

ServiceNow ranks No. 1 in 6 tech workflow segments

ServiceNow Partner Awards 2025: Leading the future of work with AI

ServiceNow and Salesforce Enter the AI Agent Arena: Paving the Way for Autonomous IRM

ServiceNow Agentic AI: Save Time, Reduce Risk, Improve Support | ClickUp

An overview of ServiceNow AI: Capabilities, pricing, and a simpler alternative - eesel AI

ServiceNow: A Risky Bet on AI Agents | by Grant Gamble | Medium

Compare ServiceNow HR Service Delivery vs. Workday HCM - G2

ServiceNow Vs Salesforce Vs Workday: Which One Matches Your Operational Needs?

ServiceNow Vs Workday: A Detailed Software Comparison

ServiceNow and Workday Integration Seamlessly Transform Operations

Workday and ServiceNow: Is Integration Right for You? - Virtelligence

Now Assist FAQs - ServiceNow Community

Now Assist and Agentic AI glossary - ServiceNow

New features and products in Yokohama - ServiceNow

Did Our 2025 ServiceNow Predictions Come True? - CoreX Corp.

Finance & Supply Chain - Knowledge 2025 - ServiceNow

ServiceNow joins CPO Outlook 2025 - EBG | Network | Nordic Procurement Insights & Events

Is ServiceNow CTA Worth It? A Complete Breakdown of the Certified Technical Architect Journey

ERP Core Modernisation - Deloitte

Driving ERP modernization with a "clean core" - ServiceNow

ERP Modernization Toward a Clean Core - ServiceNow

Service Now for AI Governance? : r/servicenow - Reddit

Evaluation tab in AI Control Tower - ServiceNow

Why ServiceNow's AI Control Tower Matters - RL Canning

Using the AI Control Tower in ServiceNow for Enterprise-Wide AI Governance

Salesforce vs. Servicenow- Which is Best? - igmGuru

ServiceNow vs. Salesforce: Which is Better In 2025? - NGenious Solutions

Servicenow vs Salesforce - Comparison, Differences - GeeksForLess