Yesterday, while reviewing and posting my thoughts on Nvidia's blowout earnings, I got to thinking: “Who are the kinds of investors who don’t want to invest in hyperscalers or Nvidia?”

It’s often easy to assume that everyone is like you, so putting yourself into someone else’s shoes and trying to see the world through their eyes honestly is a vital lesson for being a good human being, friend, mentor, husband, and father (and also a successful business owner and leader😉).

I was able to come up with three types of people who might be avoiding hyperscalers and Nvidia, in other words, those who don’t want to participate in the AI boom.

High-yield investors (only interested in safe blue-chips that pay the bills, no time or interest in keeping up with Jensen’s delightful antics😂)

Investors Who For Ethical Reasons Refuse To Participate (If you think big tech is the devil and it’s all blood money, then you might choose not to own AI stocks).

Investors who think it’s all a bubble/scam, “I don’t trust these numbers! I don’t trust Nvidia! It’s all fake! None of the profits are real!”

I actually read that last comment on a Seeking Alpha thread after Nvidia earnings came out, and I have a lot of empathy for all three kinds of investors.

I know that Type one non-AI investors are just tired of hearing about AI, because it won’t directly affect their standard of living, at least not their income streams.

Type 2 non-AI investors, I want to help them live their values (as an ethical Vegan, I 100% understand what it means to put ethics above money, and I want to help people who live this way thrive).

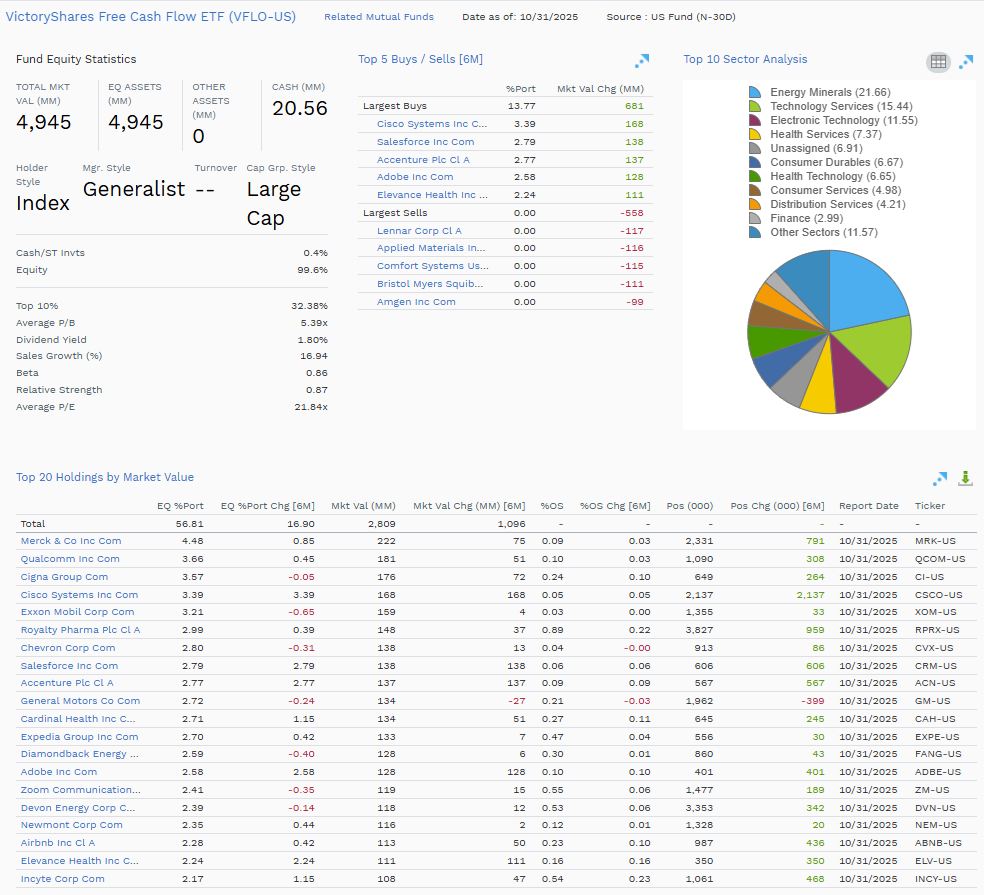

If you are opposed to AI, ETFs like VFLO (Buffett-style deep value investing) are a great way to earn AI-like returns from non-AI deep value blue-chip stocks.

VFLO = Strong Growth, Deep Value = As Non Mag 7 As You Can Get😉

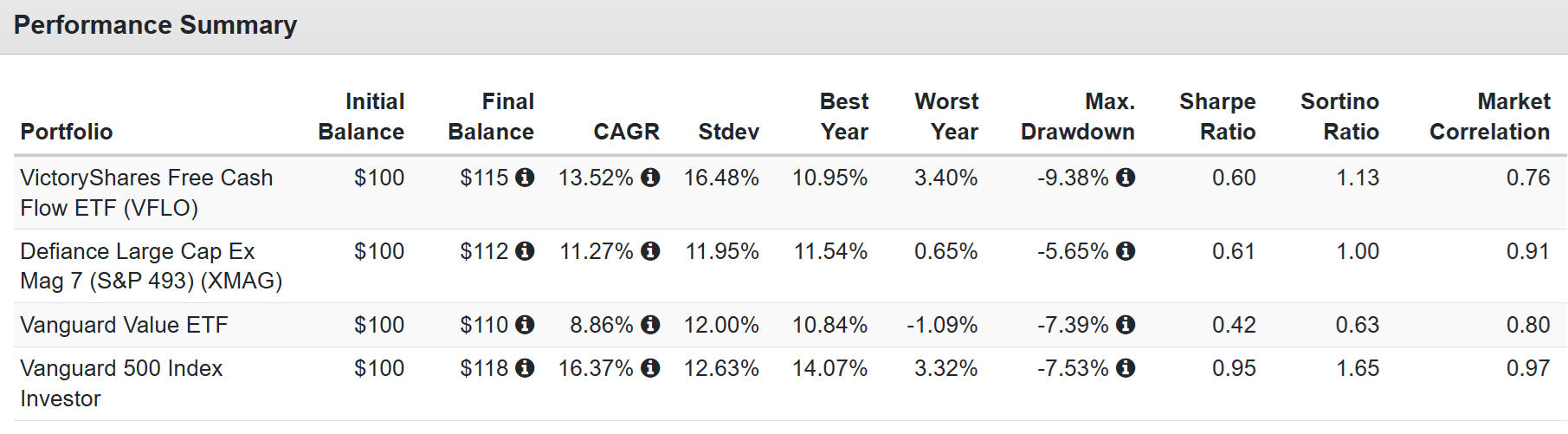

Since Nov 2024 (XMAG Inception)

You can see that, without the Mag 7, investors earned strong returns over the past year and beat value stocks, but VFLO’s deep value growth strategy delivered returns similar to those of the Nasdaq over the last four decades (13.5%).

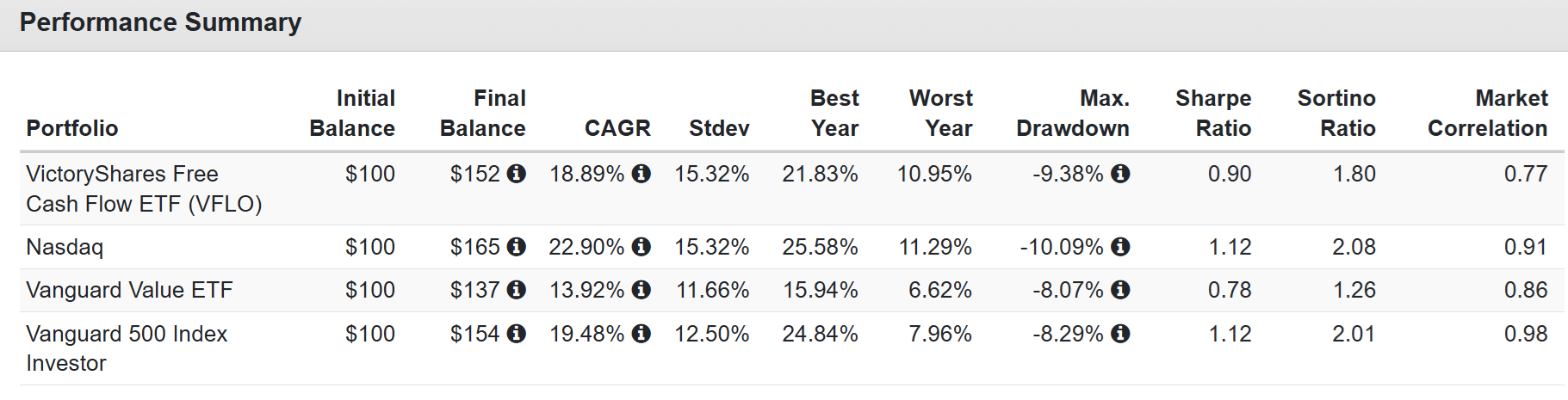

Since July 2023 (VFLO Inception) - Math Matches Historical Strategy BackTest

VFLO has delivered its historical strategy returns since 1991, meaning that this strategy has been validated (at least for the last 2.5 years) with real-world results, not just an impressive backtest.

The point is that if you want to live your ethics, that’s fine, BUT you shouldn’t have to take a vow of poverty, because food, and paying the bills are still a thing😂

For Type 3 non-AI investors, I want to kindly, compassionately, and in as humorous and delightful a way as possible😉 help them understand that this AI boom is real, but many micro-bubbles can be safely avoided.

OK, so today I want to address the type 1 non-AI investors, those who wish to invest, who love the idea of AI, who believe it’s real, but are yelling, “Show me the AI money! Daddy’s got to get paid😉 Bills Are Still A Thing😂”

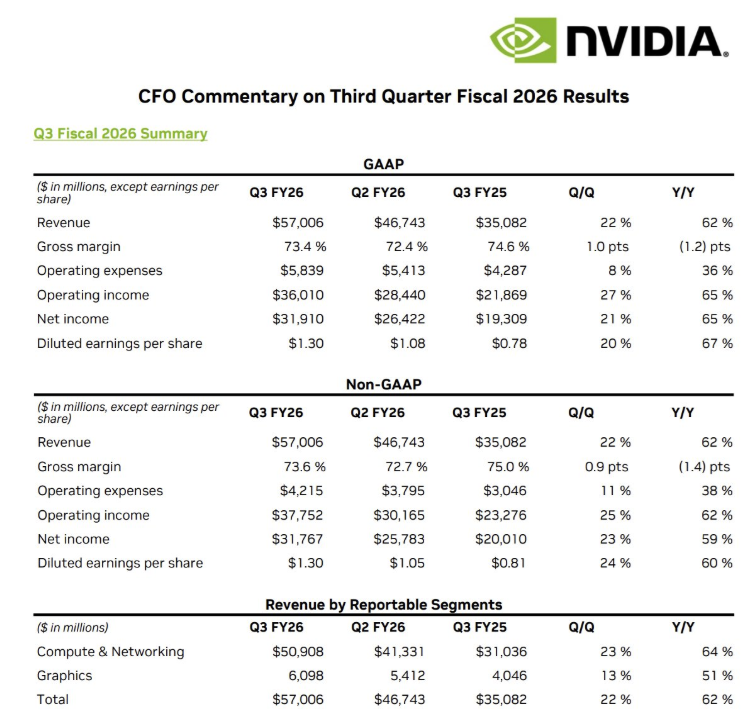

Quick Victory Lap For Nvidia Earnings Results

Yes, I realize the irony of doing an article about alternatives to traditional AI stocks, and beginning it with a review of the ultimate AI stocks’ blowout results.

Please work with me, people. I have so many meetings all the time now, I’m writing these reports when I can, and need to get out as much important info and charts as possible.🤣

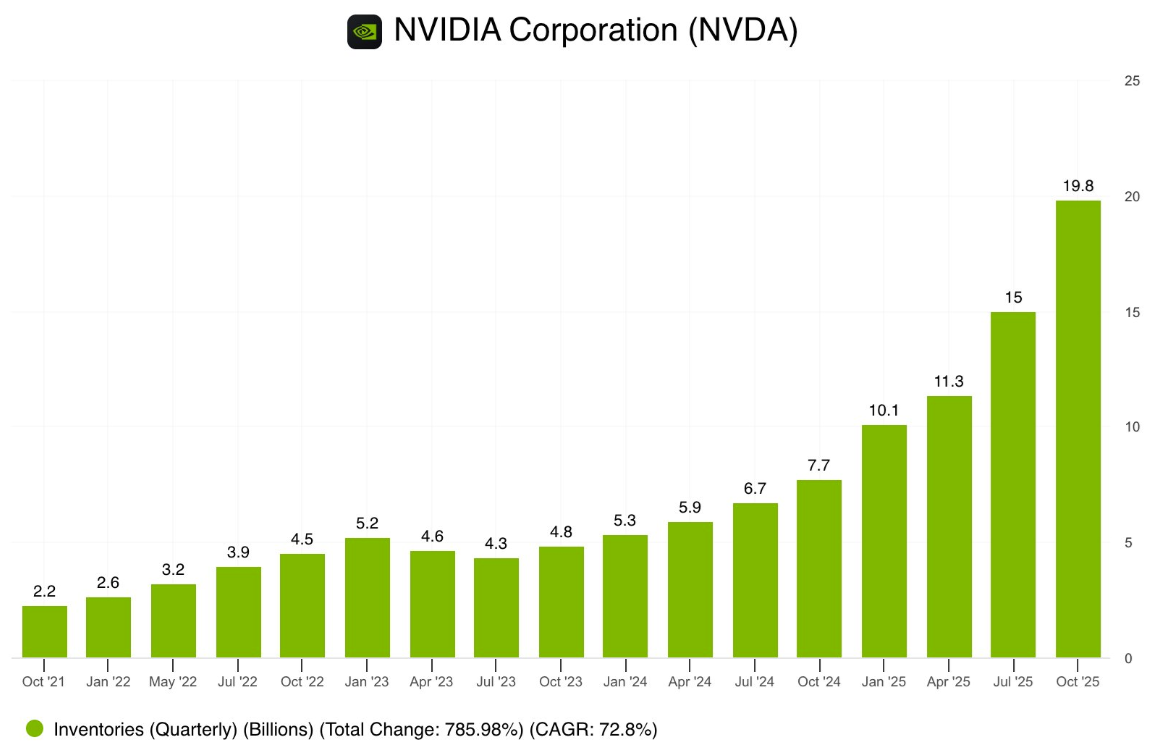

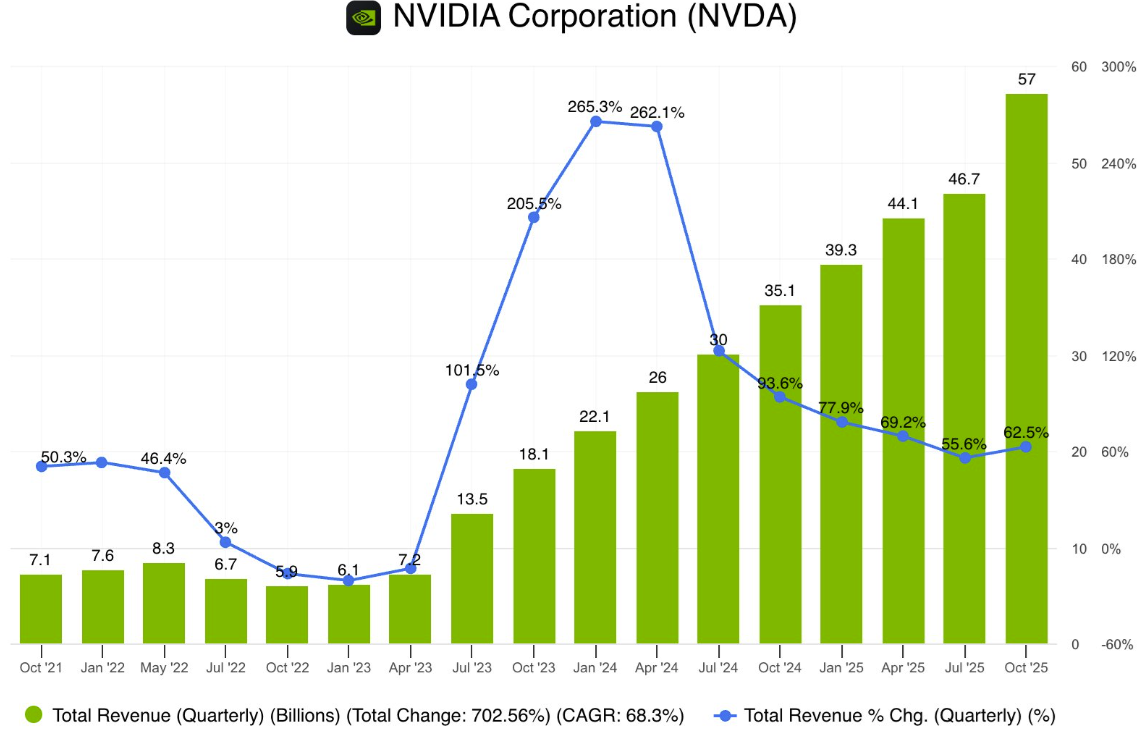

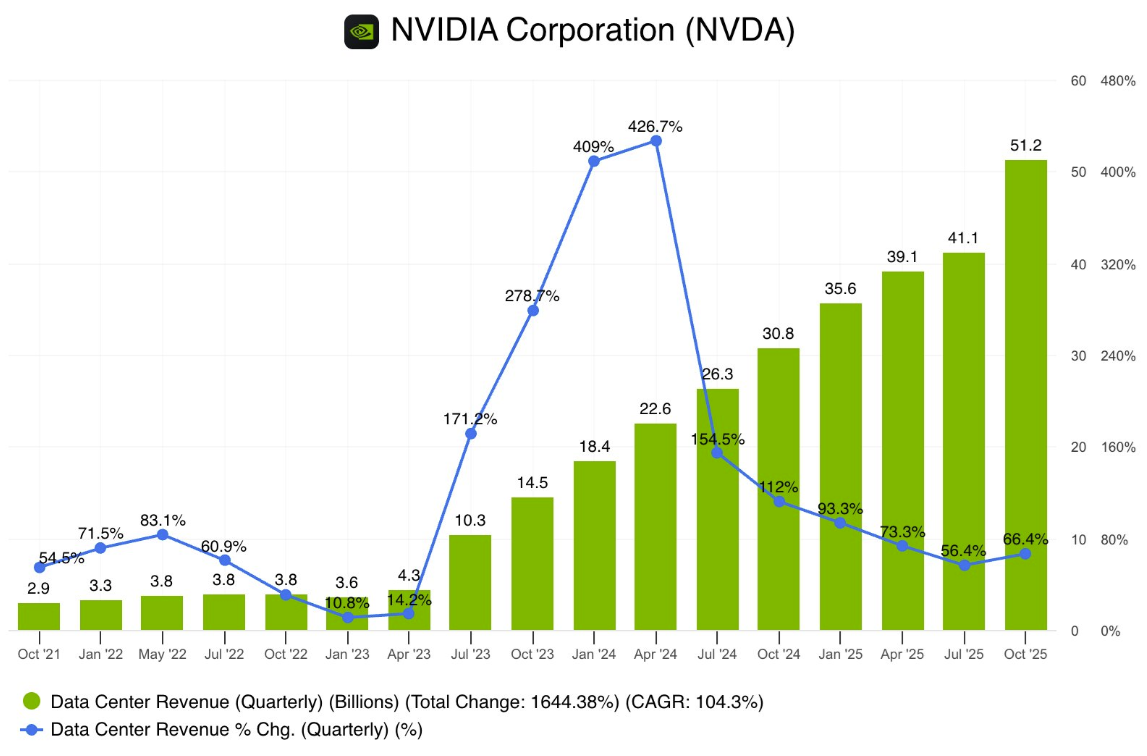

62% sales growth, 67% EPS growth, and guess what? Growth rates have started to accelerate!

Jensen mentioned on the conference call that orders for 2026 are at $350 billion and climbing. They are 100% sold out, and orders keep pouring in.

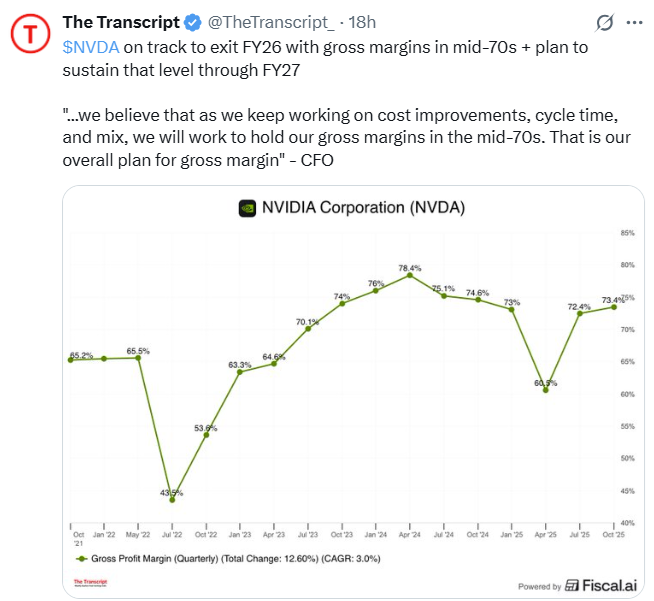

Margins are not mean-reverting when a company is supply-constrained, and for the foreseeable future, Nvidia is not a cyclical company; it is a chip utility that ramps up capacity as fast as possible and sells out every unit it produces at full price.

If that changes, I’ll let you know; it kind of matters a lot to the thesis and the ZEUS family’s financial future😉

Jensen said on the call that in the last quarter alone they had struck deals for 5 million GPUs, vs. the 4 million they sold in all of 2024.

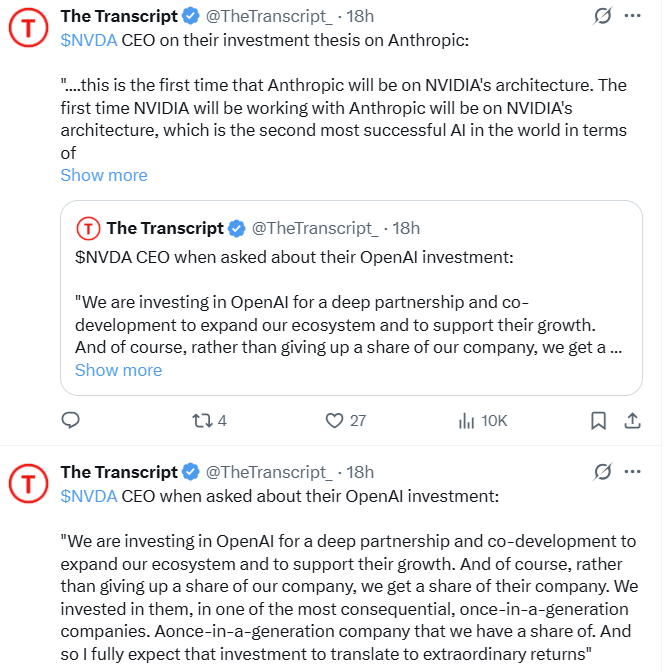

Nvidia has a deal to invest $15 billion into Anthropic (a joint agreement with Microsoft) at a $350 billion valuation. Before you get worried about circular deals, here is how this deal works.

Anthropic has pledged to build 1 GW of data center capacity using Nvidia hardware.

They raise that money from investors or borrow it.

That’s $50 billion and $35 billion goes to Nvidia.

At current margins (which are stable due to supply constraints), that $19.5 billion in net profit.

Nvidia makes $19.5 billion in profit, then gives $10 billion to Anthropic, and ends up owning 2.8% of Anthropic.

If Anthropic goes bankrupt, Nvidia “Only makes $4.5 billion in net profit” on the deal.

The same is true for the OpenAI deal.

10 tranches of 1 GW each.

OpenAI raises money from investors or debt markets.

OpenAI builds 1 GW of datacenters, paying Nvidia about $35 billion for hardware.

Nvidia makes about $20 billion in net profit.

Then, it gives OpenAI $10 billion in exchange for 1% of OpenAI (which is going IPO in 2026 or 2027).

Nvidia is NOT giving money to Anthropic or OpenAI just so they buy hardware; it’s making really good returns on these deals, AND it will own 4.2% of Anthropic and 1% to 10% of OpenAI if Dario Amodei (Anthropic CEO) and Sam Altman (OpenAI CEO) make good on their deals.

No risk to the downside

All the upside potential of owning Anthropic and OpenAI

If both companies go bankrupt, Nvidia either makes no money (and loses none) or makes billions.

In effect, this is like a profit-sharing agreement: if there is no profit, Nvidia loses nothing; if there is profit, Nvidia gets to keep it AND equity upside in the two frontier lab companies that dominate around 90% of the AI market.

FactCheck (Because AI Deals Are Complicated And We Can’t Afford To Be Wrong)

These deals are structured so Nvidia can't lose money because they only pay out if there is a profit. It's "heads I win, tails I don't lose."

OpenAI + Anthropic + XAI Spending is Speculative…HyperScaler Spending Is Smart

$500 billion in orders, and the risk is to the upside🤣😉

63% growth in supply vs 115% potential growth due to the $500 billion in orders.

Nvidia Sales Growth Never Fell Below 50% YOY, AND Might Start To Accelerate Again!

Since the Launch of ChatGPT, NVDA data center revenue has been over 100% YOY. Nothing like this has ever happened in history.

Next-quarter guidance is $65 billion, with zero from China.

$260 billion annualized revenue = $143 billion in annualized free cash flow according to management guidance.

The consensus is 50% growth next year.

So $100 billion in quarterly revenue guidance is likely by the end of next year, which equals $400 billion in annualized revenue.

25% growth consensus for 2027 = $125 billion quarterly guidance, possibly from Jensen by Nov 2027 for Q1 2028.

$500 billion annualized sales = $275 billion in free cash flow.

Welcome to the Age of AI.

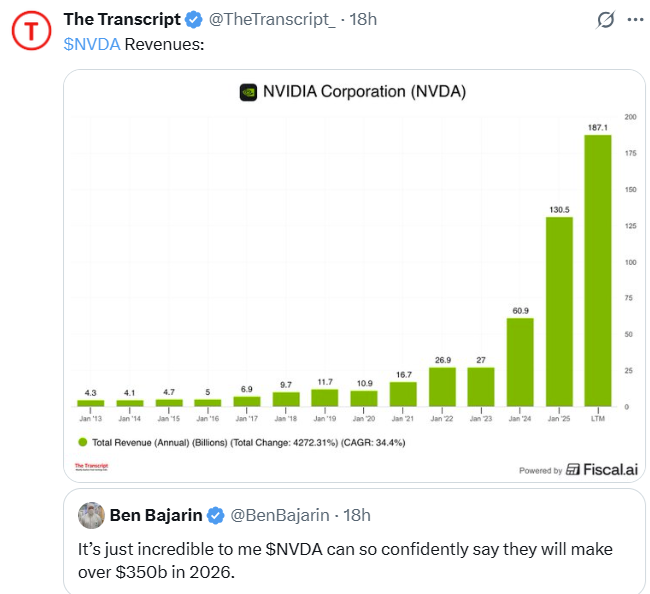

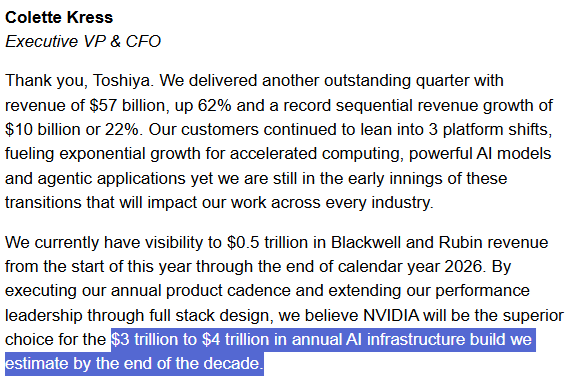

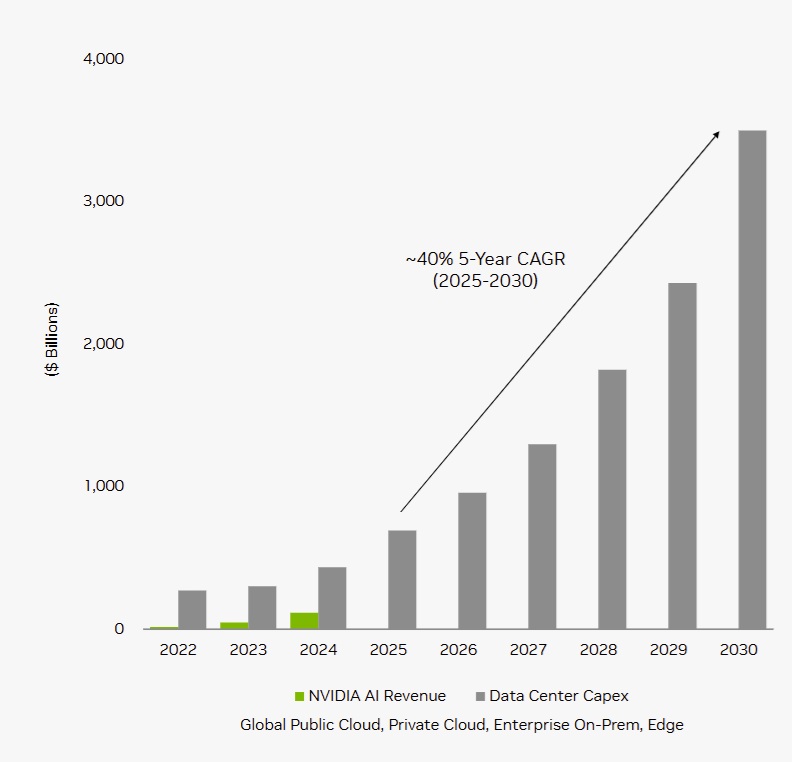

If I quote you, Nvidia’s CFO talking about $3 to $4 trillion in annual AI spending by 2030? I sound like a madman, but it’s not me saying it, it’s Nvidia’s CFO😂 The numbers are so big, the growth is so strong, it breaks out brains just thinking about it.

Why Brookfield Is The Best AI Dividend Stock…For Those That Demand Dividends From Everything They Own😉

Yes, Nvidia, Microsoft, Alphabet, and Meta all pay dividends. But if you want REAL dividends, I’m talking 2.5+% yield (Vanguard high-yield ETF yields 2.5%) from an AI stock, you can’t do better than Brookfield Asset Management (BAM).

Why do I LOVE BAM enough to have it a 4.2% of the ZEUS fund for the foreseeable future?

ZEUS Target Allocation

So why do I consider BAM such an attractive AI stock? Let’s Count the ways!

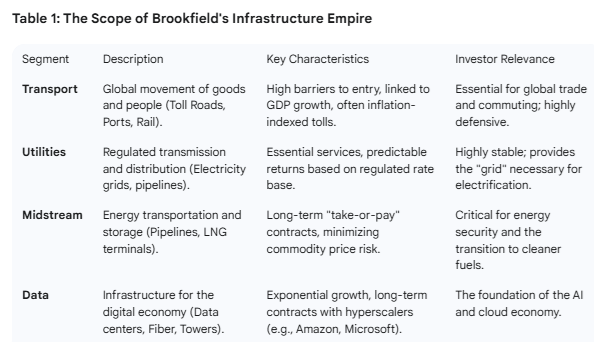

Reason 1: Brookfield Is The World Leader In Infrastructure Investing

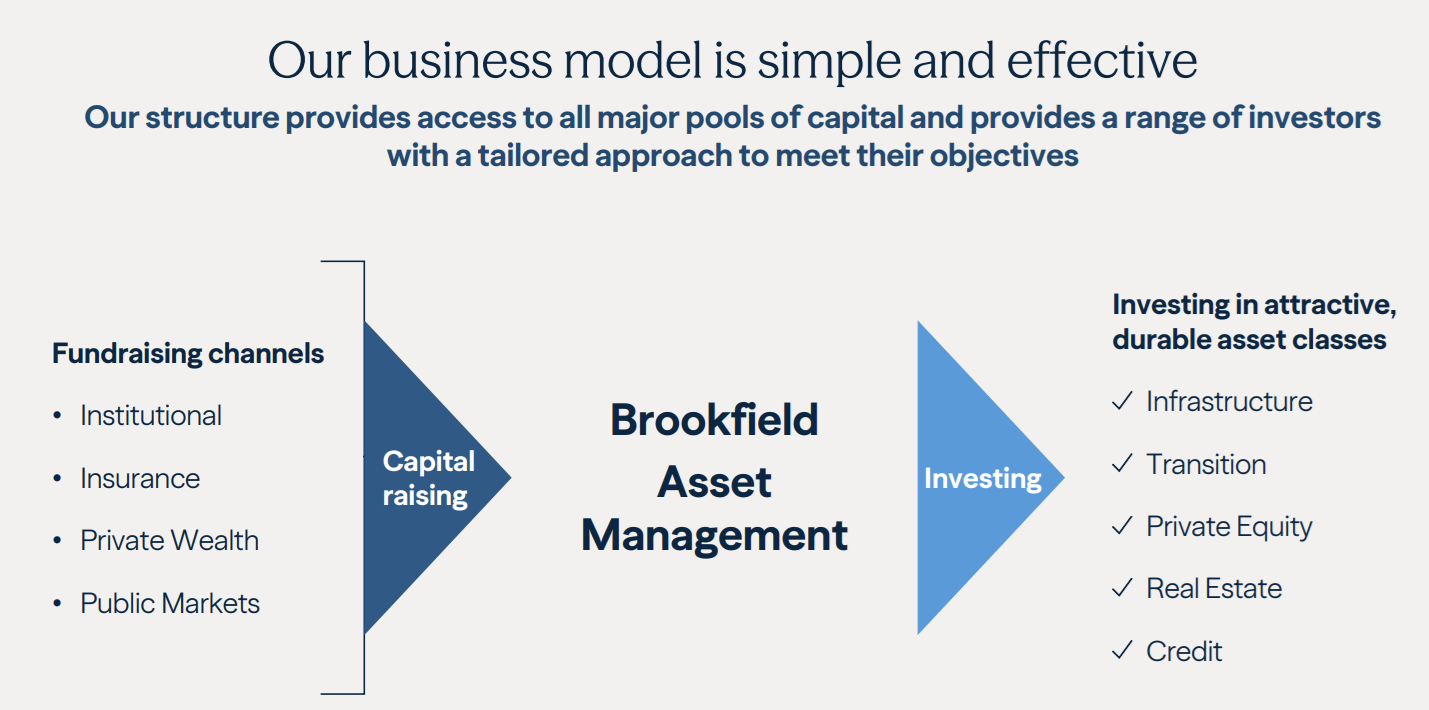

Brookfield essentially pioneered infrastructure as an asset class for institutional investors. Their competitive advantage isn't just the money they manage; it's their global operating expertise, their ability to take on massive, complex projects few others can, and their focus on essential assets.

Key Facts and Statistics:

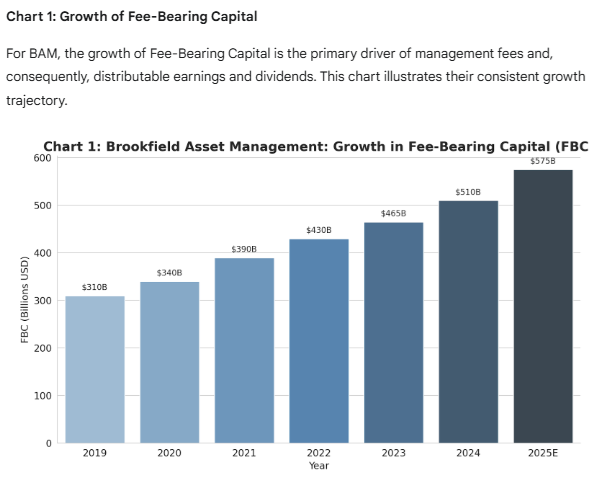

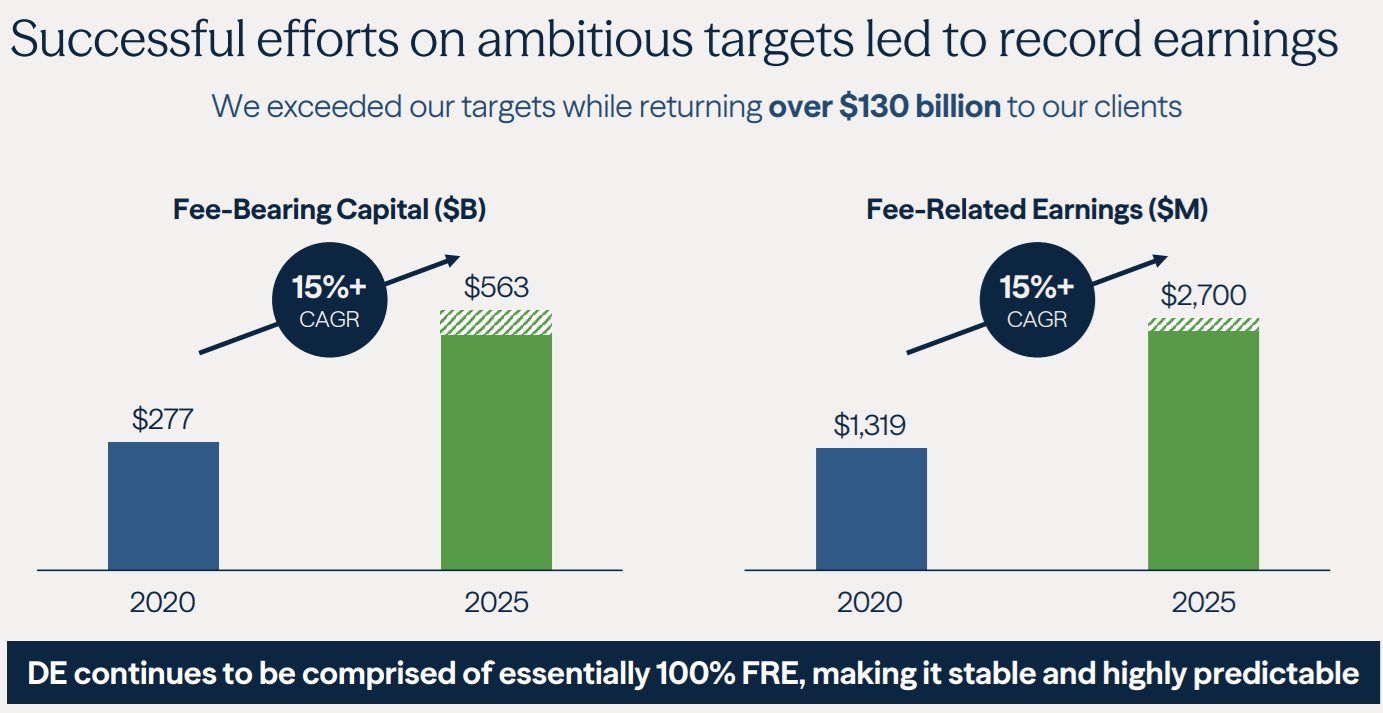

Scale: Brookfield manages over $925 billion in Assets Under Management (AUM). More importantly for BAM (the asset manager), their Fee-Bearing Capital (FBC)—the capital that generates management fees—is rapidly approaching $500 billion.

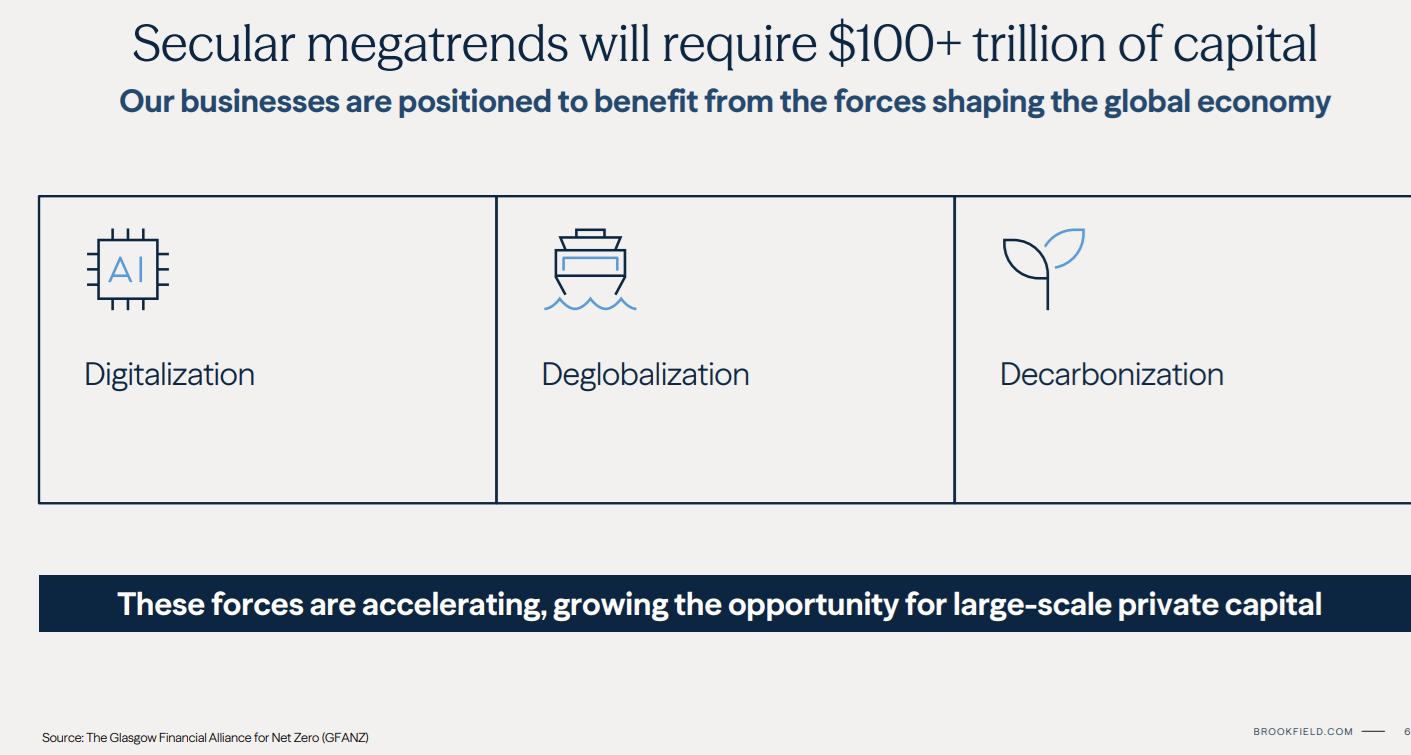

The "3 D's" Megatrends: Brookfield strategically targets investments that benefit from three major global economic shifts requiring trillions of dollars in investment:

Digitalization: The buildout of data centers, fiber, and towers.

Decarbonization: The multi-trillion-dollar transition to clean energy.

Deglobalization (Onshoring): Re-wiring supply chains, requiring massive investment in domestic manufacturing (e.g., the Intel partnership for semiconductor plants) and logistics.

Inflation Protection: Approximately 75-85% of their infrastructure assets have revenues linked to inflation indices (like CPI), possess "pass-through" mechanisms for rising costs, or are backed by long-term "take-or-pay" contracts. This makes their cash flows highly resilient during inflationary periods.

Operational Edge: Brookfield is an owner-operator, not just a financial allocator. They deploy internal teams to improve the efficiency and profitability of the assets they acquire, which is a key differentiator from purely financial buyers.

Fundraising Dominance: Brookfield consistently raises the largest funds in the sector. Their Infrastructure Fund V closed at $28 billion, the largest infrastructure fund ever raised at the time, demonstrating significant institutional investor confidence.

And in case you don’t trust Gemini 3 Pro, here’s management explaining that they expect to deliver Buffett-like “20+% total returns” for the next 5 years.

With Brookfield, you’re not just getting Bruce Flatt and Howard Marks; the team is 1350 Shark Tank-level industry experts specializing in 5 different investment strategies on six continents.

Brookfield isn’t some private equity “barbarian at the gate” who swoops in to buy a distressed asset with leverage, then tries to short-term boost profits to flip it for a quick profit. They are owner-operators that build lasting value and then earn Buffett-like returns for investors over years and decades.

Reason 2: Brookfield Is Helping Finance The AI Boom

Brookfield’s fee-bearing capital, which funds all our dividends, is growing rapidly and steadily, and you might wonder, “How big can it get?”

Of course, you have to be careful when people start quoting total addressable markets or TAM, because it’s the classic Shark Tank swindle.

“This is a $100 trillion market, and if we get just 1% of that, that’s $1 trillion, and the company is worth $20 trillion, and we’ll all be fabulously rich!”

The question is always, “Is the market REALLY that big? And if so, how exactly are YOU going to be the winner who takes and holds 1% market share, PROFITABLY!?”

Snakeoil salesmen will try to sell you on untold riches, but professionals like Brookfield have spent 125 years actually building wealth for the long-term.

Brookfield Always Lowballs Their Growth Estimates

Brookfield is telling its clients that AI spending will reach $700 billion per year over the next decade, and BAM wants to get in on that action with a $100 billion AI Fund.

Brookfield’s risk is likely to the upside, meaning AI spending will be much larger than they are telling clients and investors.

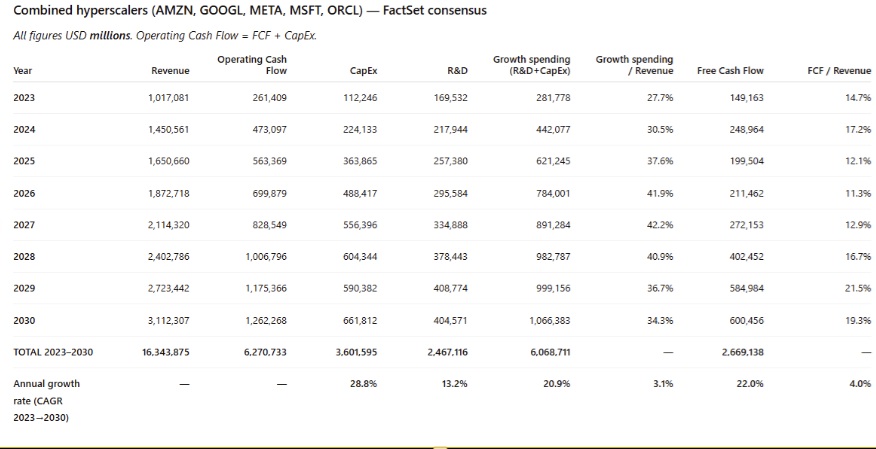

FactSet Consensus For Hyperscalers 2023 Through 2030

$700 billion per year in global AI spending over the next decade? By 2030, analysts currently expect the five hyperscalers alone to spend that much (plus another $400 billion on R&D).

$4 Trillion Of AI Spending Per Year By 2030 (Morgan Stanley, Citigroup, IDC, Nvidia)

Yes, I get excited by big numbers like most investors, but that’s why I’m not running multi-billion corporate empires…yet😉

I trust management teams that underpromise and overdeliver, and when the promise is “20+% long-term returns,” the overdeliver is the cherry on top. Still, as long as they grow at even half that rate, the total returns are 12% to 13% per year, which is historically market-beating and Nasdaq-like returns.

The key to Brookfield’s success is that they are the adults in the room. When a wealthy family wants to invest in infrastructure, they trust Brookfield. When insurance companies want to invest their float into something other than Treasuries? They trust Brookfield.

When sovereign wealth funds, pension funds, and college endowments want to diversify beyond just bonds and stocks, they trust Brookfield because it has been around for 125 years and has an excellent track record for results AND avoiding scandals.

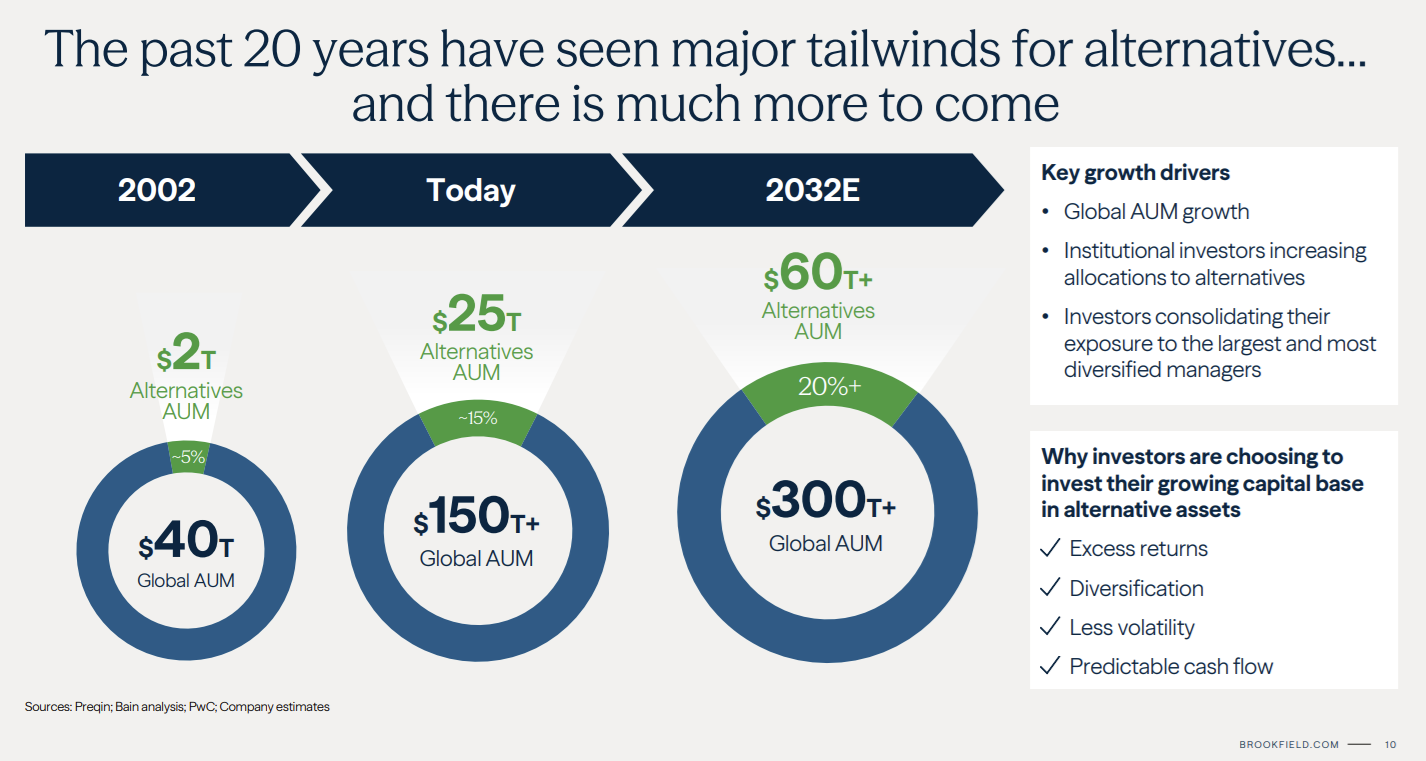

Brookfield is confident that it can keep or increase market share in the alternative asset management industry, which is expected to grow to $60 trillion by 2032. That’s out of $300 trillion in globally managed wealth.

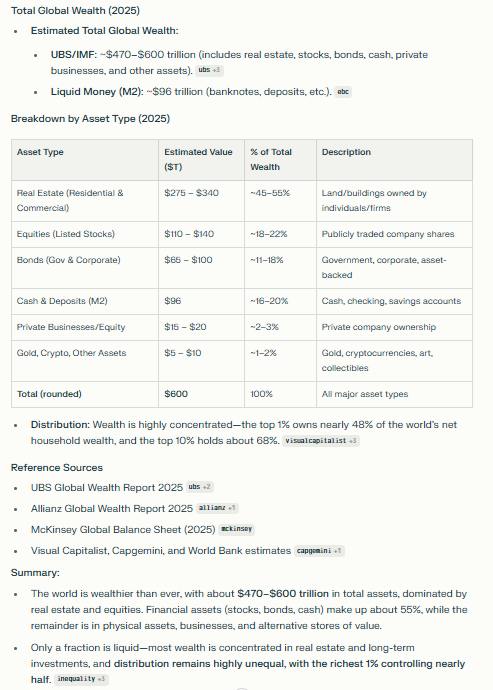

$600 Trillion in Global Wealth (Lots of Money for Infrastructure Spending)

Why should we believe that BAM is going to be a leader in that $60 trillion Alternative asset business in 2032?

Because BAM delivers on its promises to investors.

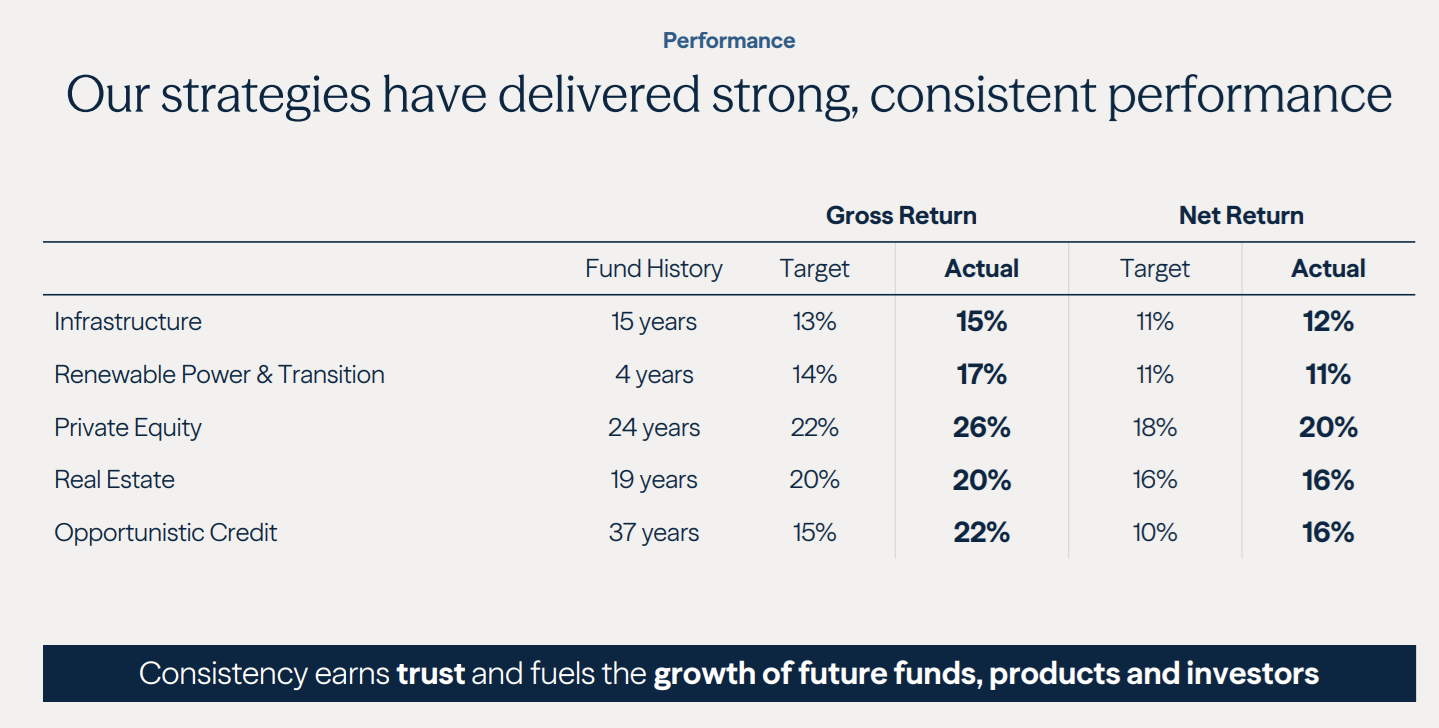

They had an opportunistic credit fund that closed after 37 years, after delivering 22% CAGR gross returns, 47% above target, and even after fees, its was 16% CAGR returns.

Their worst-performing funds? Deliver 11% after fee returns…which is what they told investors to expect.

Private equity strives for 25% annual returns (3X in 5 years). And BAM told clients to expect “just” 22% and 18% after fees. They got 20%, Buffett-like returns, just as expected.

In real estimate, they told investors “16% post-fees returns,” and after 19 years, that’s precisely what investors got.

They told infrastructure investors to expect 11% post-fees returns on infrastructure, and delivered 12%. That wasn’t luck; it was over 15 years, which means a 90.5% statistical probability of skill, not luck.

While not perfect, BAM has a track record of delivering for investors, which is why its fee-bearing capital is approaching $600 billion.

Over $1 trillion in total assets under management because they have hundreds of billions in “dry powder” that only gets called when they see an investable opportunity.

That’s the genius of their business model. They raise funds from institutions, which sign contracts to deliver the money to BAM on short notice. Then BAM starts collecting fees on it and invests it. When BAM says “we can grow 20% annually for 5 years,” they know that they have the fee-bearing capital under contract, and that’s why it’s some of the most reliable guidance on Wall Street.

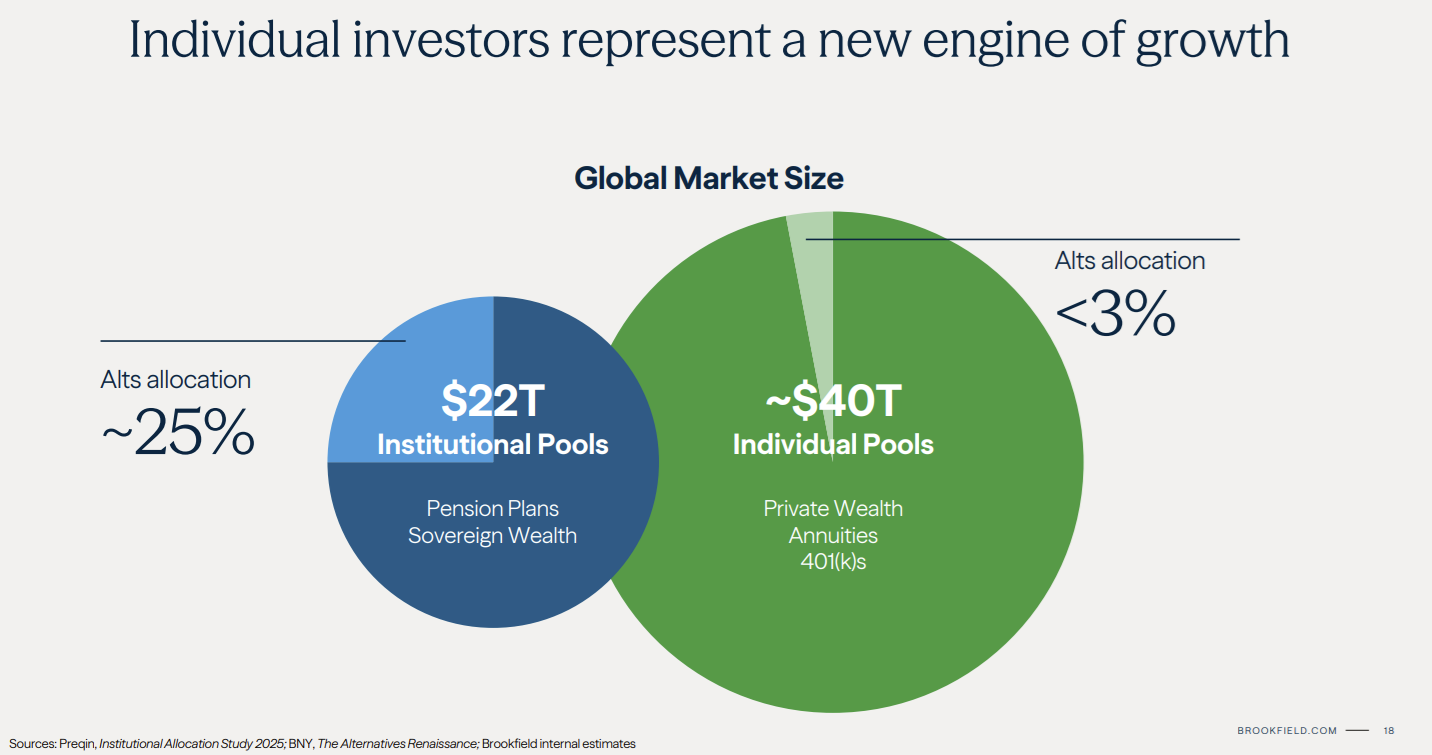

Retirement accounts are the next opportunity for companies like BAM, which will partner with Vanguard, Charles Schwab, and Fidelity to offer investors with 401(k)s and IRAs the chance to invest in alternative assets.

Do you think some fly-by-night operator with $5 billion in AUM is going to get their foot into Vanguard? No, Brookfield, Blackstone, and Apollo are going to get in.

Is this ethical? Are grandparents IRAs about to get raided by hucksters peddling low-quality funds to Vanguard? No, probably not, though the returns are likely to be around 8% to 12% for most such funds.

That’s not bad, and an IRA or 401K where you can’t touch your money for decades IS the place for such investments.

But I personally would rather Brookfield PAY ME 3.5% dividends via fees. Why buy the soy milk when you can own the robot cow? Because if you like soy milk, owning the robot cow that produces the soy milk gets you more soy milk over time.

Yes, I really am this much of a nerd😉 And this is a vegan joke😂

Because in our glorious AI-Star Trek future, our soy milk won’t come from robot cows…but from replicators🤣

And guess what? Brookfield believes it can continue raising funds from even more investors over time.

Pensions might be a small % of companies, but over time, pension funds still grow, and they need to own things other than stocks and bonds.

BAM isn’t just an AI play; it’s about the physical world. No more software is all you need. We need to BUILD STUFF RIGHT NOW! And BAM is all about building; they’ve been doing it for 125 years!

To power AI, you need to build data centers, then build pipelines to supply fuel and water, and finally, the raw power to run the racks. It’s all a holistic strategy that involves infrastructure at every level. AI isn’t about tech or software, it’s about infrastructure!

The “Star Trek Future” will need massive infrastructure to power it. It might seem magical, but it’s all just math and engineering.

And BAM is providing the financial engineering to make it possible.

The AI Age Of Abundance…. Brought To You By Brookfield 😉

What does Brookfield Private Equity look like? It’s as nerdy as the infrastructure! Industrials and infrastructure services!

It’s all about building things in the real world, infrastructure to serve the needs of our robot overlords😂

And finally, real estate, because people and businesses have to live somewhere and put their stuff (until the replicators arrive that disassemble things we’re not using😉

Sorry, Public Storage…The Star Trek Future Is Coming To Kill You…But On The Plus Side, We All Get To Spend More Time at Olive Garden😂

Howard Marks, the man, the myth, the legend, 😉 helping to fund the largest infrastructure building project in history.

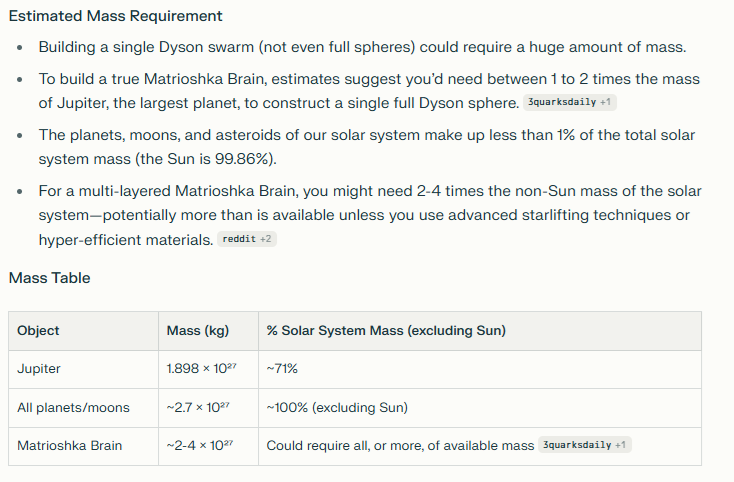

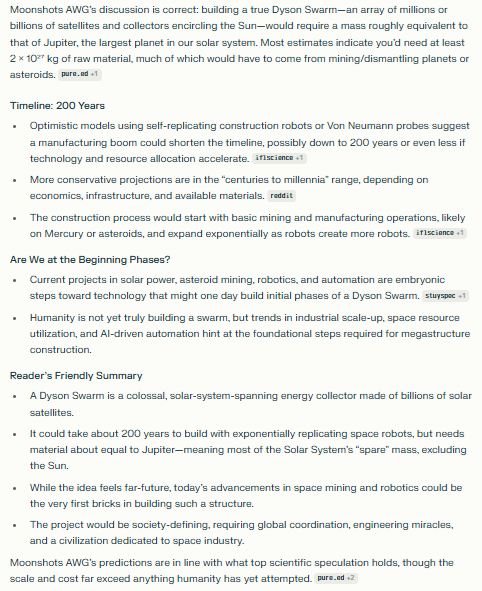

How Big Could The AI Boom Get? Dyson Swams & Matrioshka Brain! AI-Powered Robots Building Solar Panels To Capture All The Sun’s Power (200 Years Of Building)

Brookfield Is Going To Help Us Build This By Financing It (assume that people like Dr. Alexander D. Wissner-Gross are correct and that we are at the start of the construction of a mega project like this.

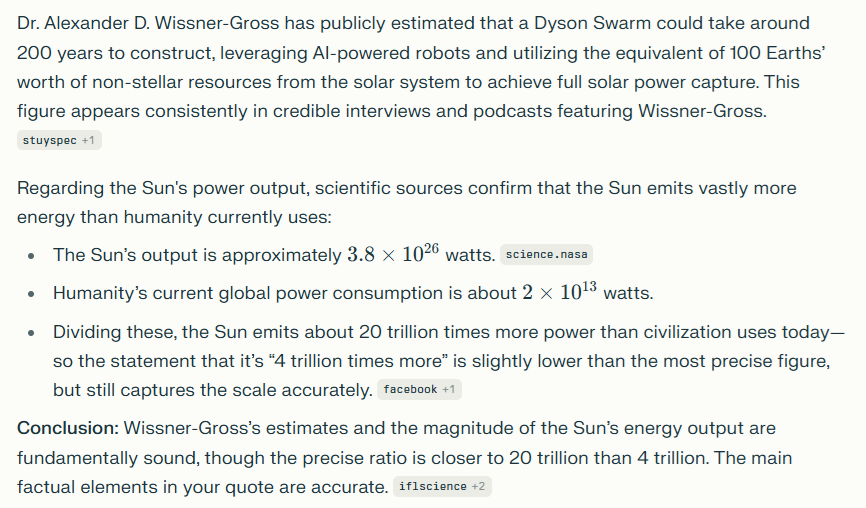

Dr. Alexander D. Wissner-Gross has estimated that it would take 200 years for AI-powered robots to harness the 100 Earths’ worth of resources in the solar system to construct a Dyson swarm, allowing humanity to capture all the power of the sun.

The sun emits approximately 20 trillion X more power than human civilization uses today.

Power isn’t infinite, but 20 trillion X more power is close enough to infinite for government work😉

If you think today’s multi-trillion-dollar spending plans hurt your brain? In the future, we could be measuring things in quadrillions or even quintillions of dollars.

The asteroid Psyche 16 has an estimated $700 quintillion worth of metal in it = 7 MILLION YEARS OF GLOBAL GDP.

Human minds were not designed to think in terms of cosmic scale; thankfully, our robot partners have no problem thinking on these scales.

Reason 3: Brookfield’s Industry-Leading Dividend Stability

All of this AI utopia stuff is fine and good, but we’re here to talk about money and how AI can put it in our pockets.

So let’s talk about why BAM is the ultimate dividend AI stock and the most stable income payer in the alternative asset management industry.

Brookfield is growing fee-bearing capital steadily and rapidly, BUT it’s not just the earnings that matter; it’s the stability of those earnings.

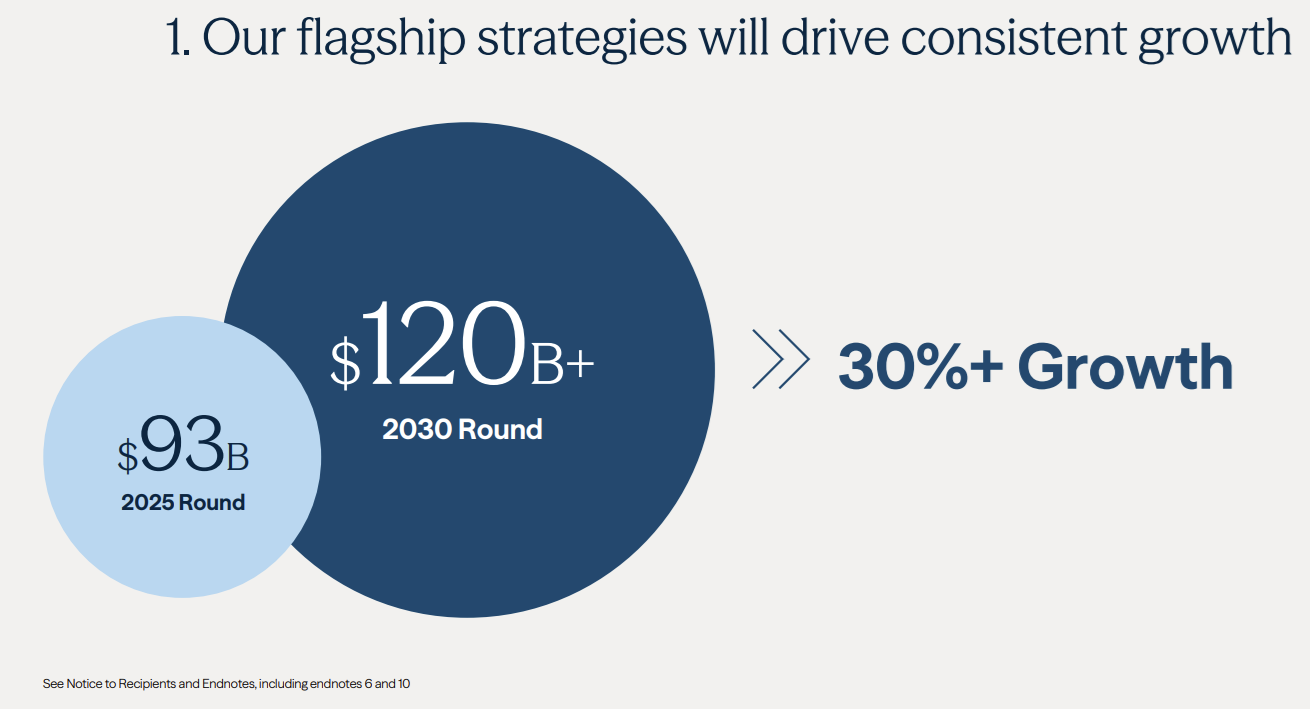

Brookfield is now doing funding rounds of nearly $100 billion, and by 2030, they estimates they will be raising $120 billion per round.

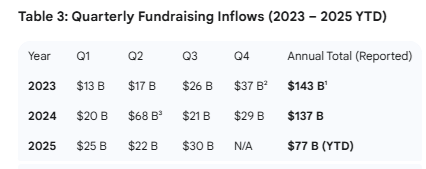

Brookfield is a fundraising machine, raising a record $137 billion in 2024.

Brookfield Is Raising $2 billion per week on its way to $2.5 billion per week ($11 billion per month) by 2030

But remember that AI spending could hit $4 trillion PER YEAR by 2030 (and likely keep climbing), so the amount of infrastructure funding is essentially infinite. No matter how much capital BAM raises, it will likely be able to invest it profitably.

For the next 200 years, at least, according to Dr. Alexander D. Wissner-Gross and his Dyson Swarm😉

In all seriousness, IF WE DO build a Dyson swarm, BAM is going to help finance it and make a lot of money for investors.

Not that we’ll care about money, we’ll all have so much 😂

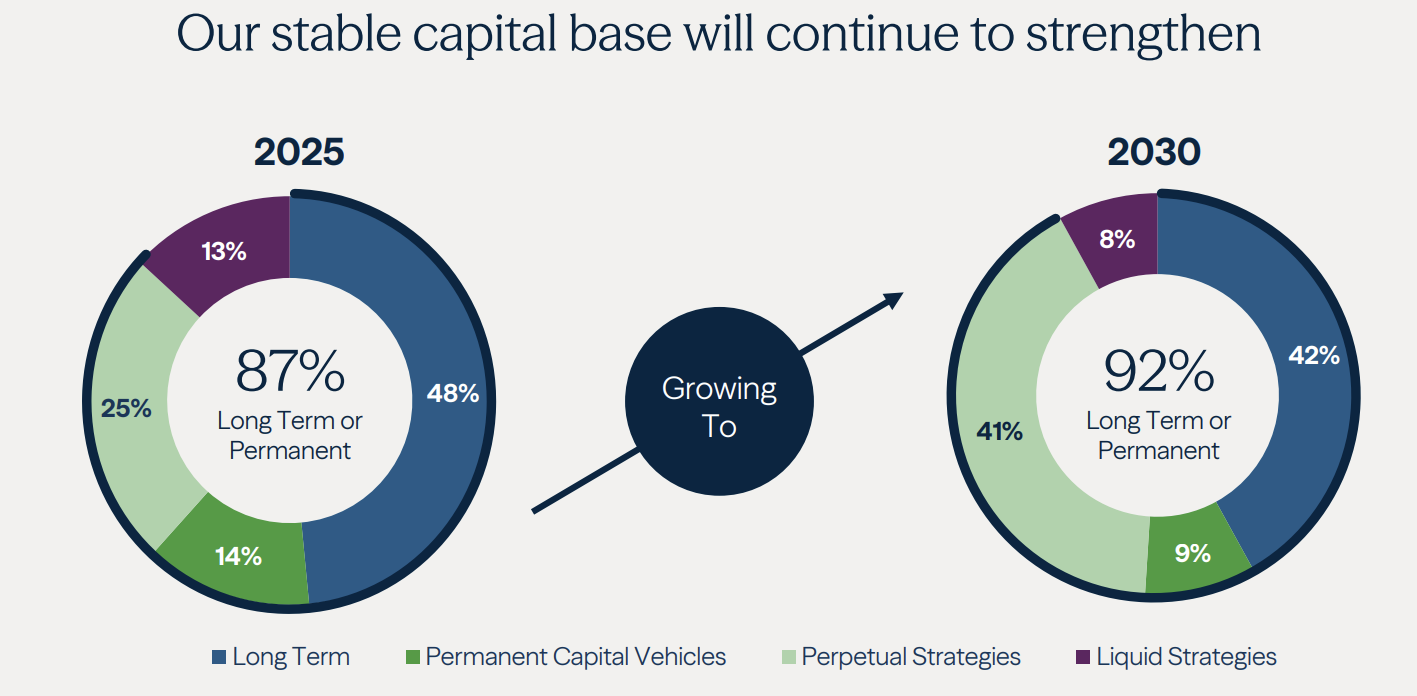

Right now, only 13% of BAM’s funds can be withdrawn at any given time. That’s expected to fall to 8% by 2030 as they focus more on permanent capital sources like BIP, BIPC, BEP, BEPC, and funds with 7 to 15 year lockups.

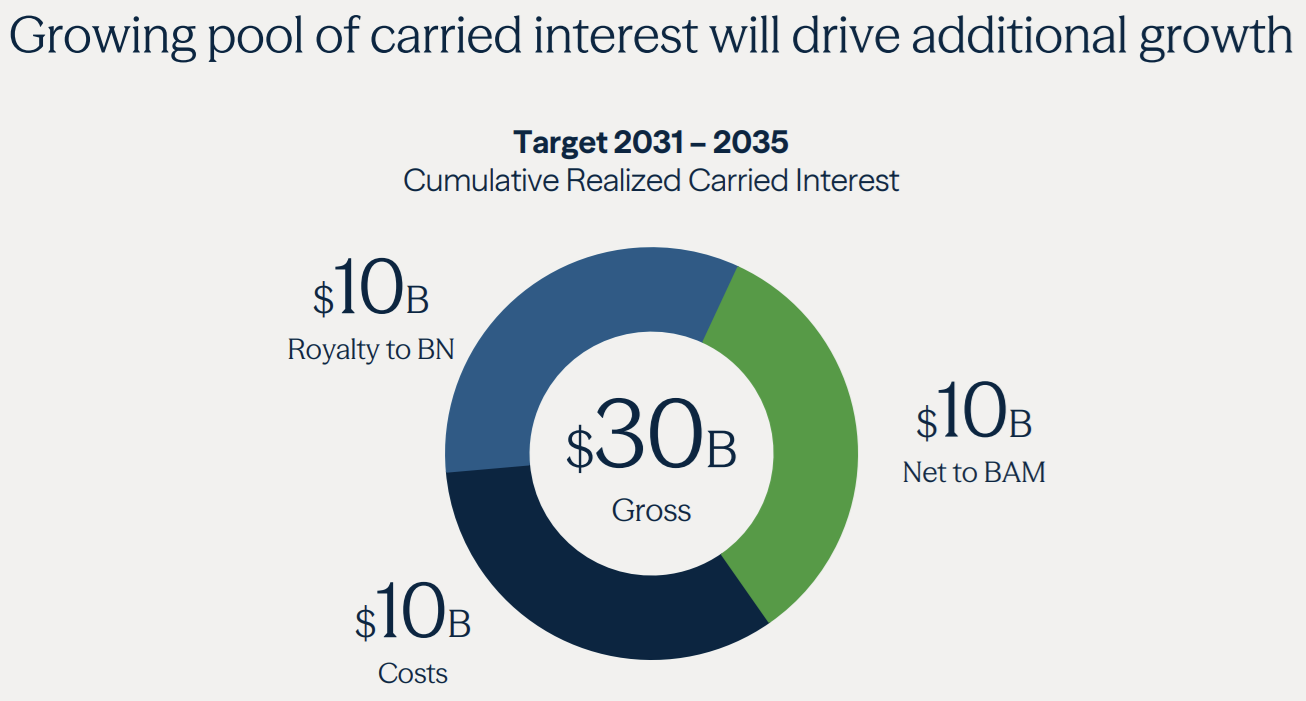

Carried interest is the profits BAM has earned (the profit share) but has not withdrawn or paid taxes on.

BAM has $2.6 billion in liquidity today and can borrow almost $1 billion at a time at 1.3% above the US Treasury borrowing rate.

The most stable fee income in the industry (because BAM is 100% funds paying fees), generating almost pure cash flow that is funding dividends that grow 18% CAGR over time. This is the science-based magic and math-fueled sorcery behind Brookfield Asset Management.

Management Team That Has Been At Brookfield For 147 Years

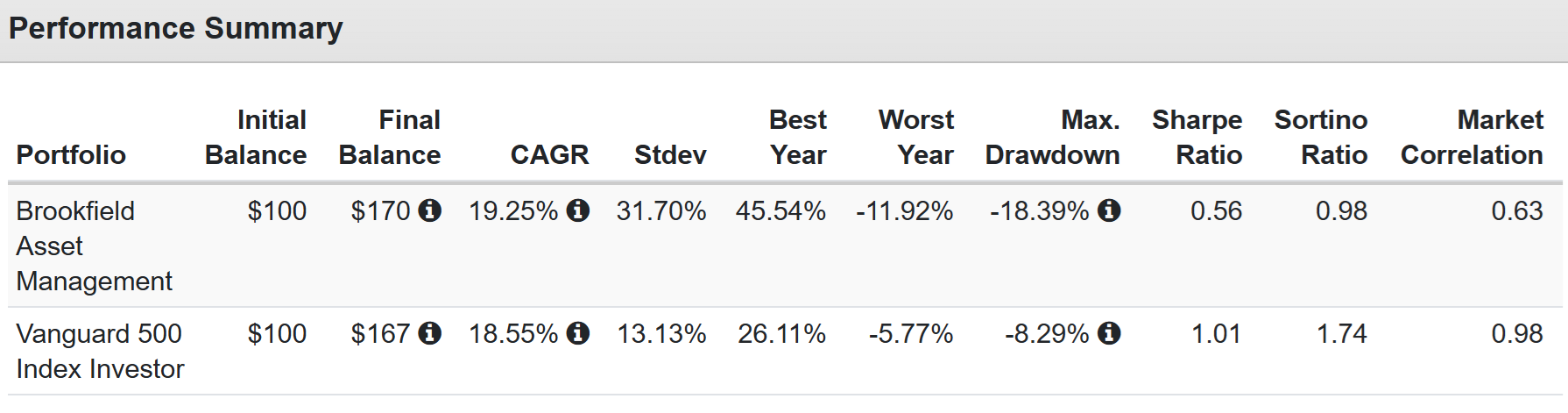

And how has BAM done since its Dec 2022 Spinoff? Has it delivered Buffett-like 20% returns?

Yes, it has, though with a lot of volatility, which is a wonderful thing for patient investors. Buying these dips is what boosts our returns by as much as 32% more than just buying and holding.

By buying BAM, the returns weren’t 19% CAGR; they were 25% CAGR.

Reason 4: Valuation is As Good As It’s Been Since the Spinoff

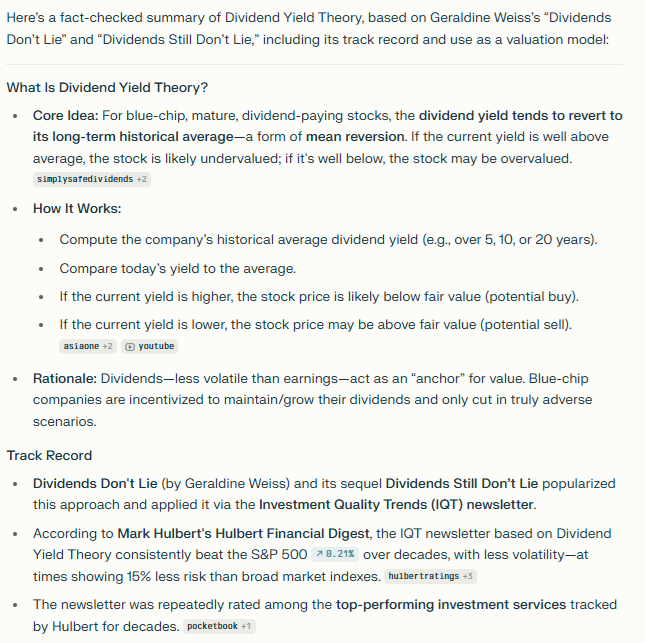

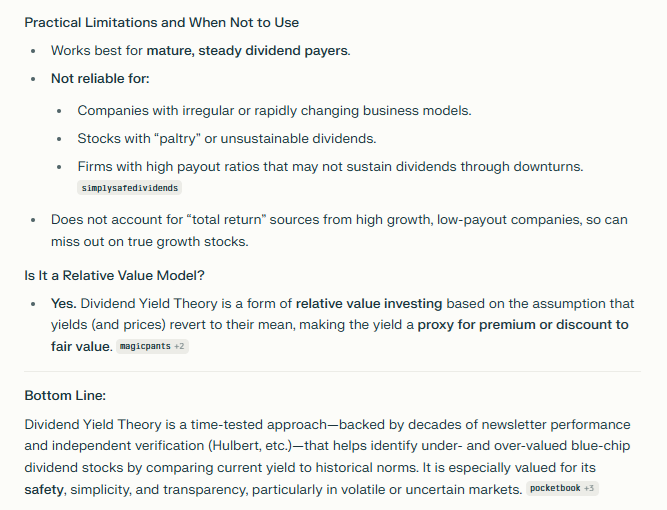

Dividend Yield theory is an effective valuation model popularized by the books “Dividends Don’t Lie” and “Dividends Still Don’t Lie”.

It’s a relative-value model that says that for dividend stocks with relatively stable business models, like Coke or Merck, the long-term historical yield relative to today’s yield can tell you whether there is a margin of safety and whether it's a discount or a premium.

So what does dividend yield theory say about BAM?

BAM was spun out of Brookfield Corp in December of 2022 as a stable yield-paying instrument, the most stable dividend payer among asset managers.

That’s because Brookfield wants to get paid, and so they structured BAM to be as stable as possible, throwing off very generous free cash flow that 95% of gets sent back to the parent company.

That’s why the industry median yield of 6% is so much higher than BAM’s historical 2.96%.

Investors value stability of cash flows and yields, which is why REITs trade at a sector average 18 FFO despite growing at 6% over time.

A PEG of 3! Yet that’s the REIT sector average for the last 20 years.

This is why relative value is so powerful. Peter Lynch and Ben Graham would not tell you that “REITs trading at 18X is fair value”. Ben Graham would say 15 is fair value because that was his rule of thumb.

But if REITs trade at 18X for 20 years, there is a 91% statistical probability that this is fair value, and if you wait for REITs to hit 15X FFO, you will be waiting a long time.

Kind of like how the CAPE ratio hit its historical average (since 1881) for only a few days in March 2009.

Other than that, CAPE has said that stocks are expensive 99.99% of the time over the last 30 years.

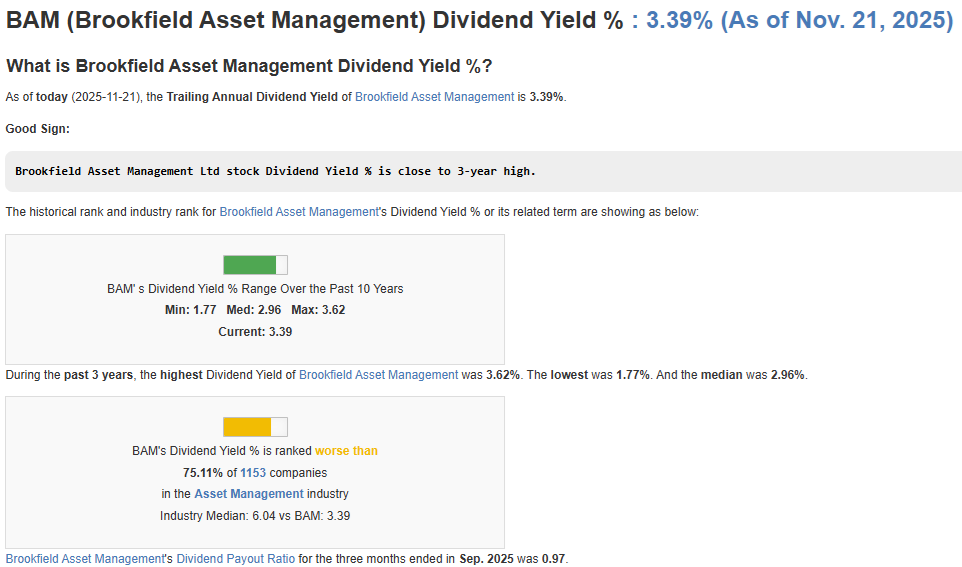

So BAM’s historical fair value is 3%…but the history is only 3 years.

So that’s not statistically significant, BUT we can say for certain that BAM’s highest yield since the spinoff was 3.62% back on April 7th, 2025.

You might be wondering “How do we know that BAM’s yield might not go to 4%, 5%, or even 6% (the industry median) at some point? Maybe in a bear market?

Well we had a 21.3% bear market that was created by an unprecedented crisis and BAM never traded above 3.62%.

Will it in the future? Sure, BUT think about why BAM’s yield doesn’t want to go above 3.6%.

It’s growing cash flow at 18% to 20% CAGR for the next 5 years, with high guidance confidence from management.

It’s an A-rated industry leader in an industry where global infrastructure spending will soon reach $10 trillion per year.

It’s a leader in financing the AI boom, with an addressable market spanning the entire global economy.

It’s cash flow is 94% annuity like, unlike any of its peers.

So THAT explains why the 3% historical median yield makes sense.

If you had a company with this high quality and a stable yield that was growing 19% CAGR for the next 15 years, according to management, would you be OK with “just” a 3% yield?

Would 21% to 23% CAGR total returns for 5 years (better than Buffett’s historical 20.5%) be enough for you to take the risk of owning BAM?

Sure, the yield MIGHT at some point hit 3.5% (it recently hit 3.6% matching the April 2025 peak yield), BUT do you think that it’s reasonable for investors in the future, who have, for 3 years, collectively decided that 3% yield is fair value, to suddenly demand 4%? 5%? or even 6%?

A 6% industry average yield is 6% yield + 18% to 20% CAGR growth = 24% to 26% CAGR total returns. That’s literally Venture Capital target returns and 20% above Buffett’s historical returns.

IS that REALLY going to be the long-term fair value? What is the mean around which BAM’s mean reversion takes place?

Or, as investors have decided, objectively, for the 3 years it’s been around, that BAM is worth 3% yield because that’s the mean around which mean reversion keeps happening?

You can always come up with a story about why BAM’s fair value yield might drop to 2.5% or even 2% (an AI boom where they can raise multiple AI funds for example, boosting growth to 25%), or where investors might demand 4% yield (if interest rates were permanently higher due to AI boom induced inflation).

BUT all such scenarios are speculative. The truth? The gospel truth, for as long as BAM has existed, is that 3% yield is the market-determined, objective fair value that millions of investors have collectively decided this company is worth.

Any story about why it will be higher or lower in the future is inherently speculative, and I prefer not to speculate.

I’m humble enough to know that "Value is what other people are willing to pay” and the “other people” is the entire market, and the entire market has so far said BAM is worth 3% yield.

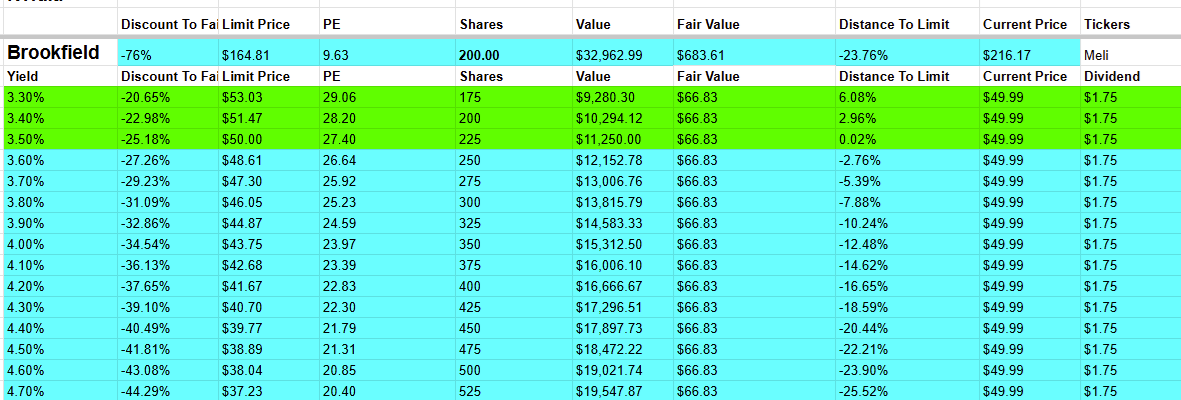

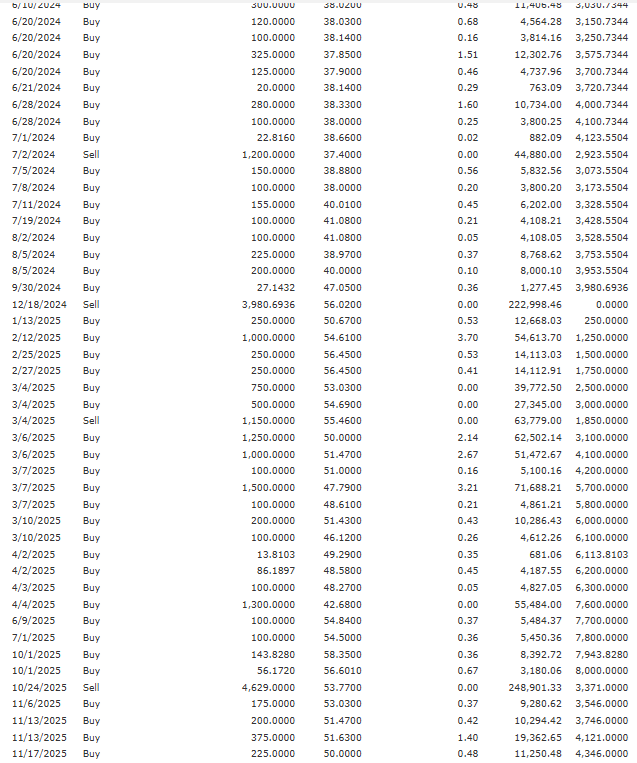

So when the yield recently hit 3.6%, that was when my final limit filled.

My Last Limit Of This Correction (Before I Ran Out Of Buying Power) Was Brookfield at a 3.5% Yield

The limits I set are never a forecast; they are simply there to dynamically rebalance by adding more if a company I own falls.

“Be greedy when others are fearful” via order automation.

Eventually, our tools will allow us to run ZEUS automatically without manual limits.

But I hope you can see why I bought BAM with such confidence on Nov 17th, and would have bought the 3.6% yield limit had I not had to turn off all limits to preserve cash for running GNG.

BAM’s 3% Historical Fair Value Converted Into FAST Graphs 12 Month Trailing Blended PE = Buffett-Like Return Potential From A 3.5% Yielding AI Dividend Bargain Hiding In Plain Sight

How did I make this chart? $1.75 dividend/.0296 (historical fair value yield) = $59.12 fair value divided by the trailing blended PE (2025’s $1.59 consensus) = 37.18 fair value PE.

So there’s the 2-year return potential from BAM as its growth rate accelerated to management’s 19% guidance, and the yield of 3.5% is 17% above its historical norm.

Growth rate is stable, so the PEGY fair value calculation would be very similar.

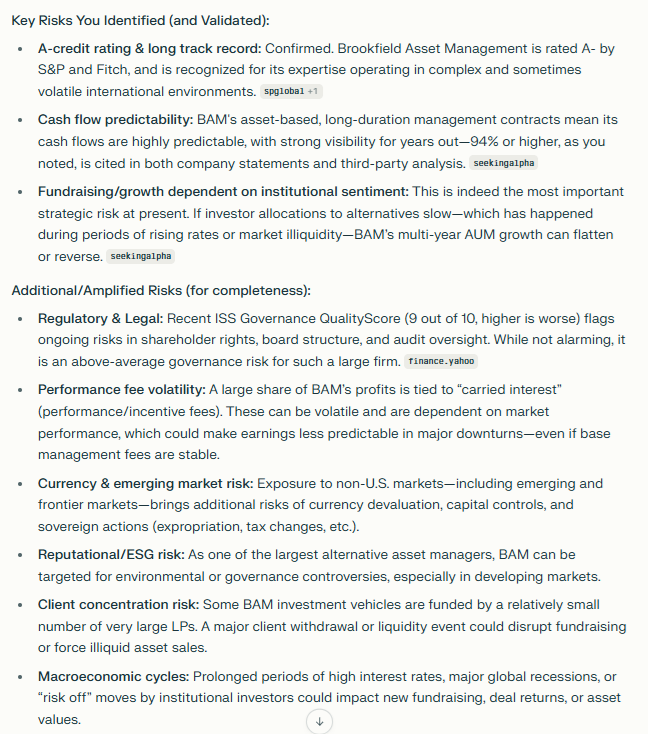

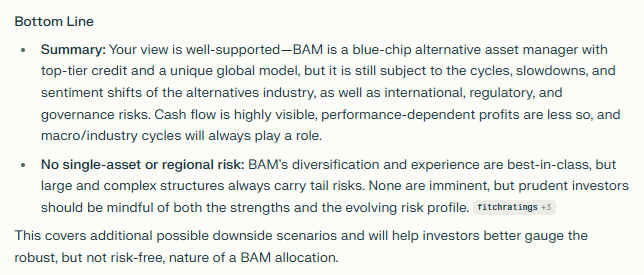

Risk Profile: What Could Break The Thesis

A-credit rating, Brookfield has been around for 123 years and is the world leader in operating under complex, developing-nation regulations, in other words, building infrastructure in poor countries, dealing with populist governments, coups, or even financial market meltdowns like the GFC.

Brookfield has been through it all, and the most significant short-term risk is not to fundamentals, because BAM’s funds are locked up for so long that management can predict with 94% accuracy in any given year what BAM's cash flows will be.

The most significant risk to the thesis is that the large institutions that are BAM’s clients decide that they don’t want to allocate more to alternative assets.

For example, the distribution rate in the industry has reached around 9%, meaning it takes 11 years (on average) to get your money out of an alternative asset manager.

BAM’s fundraising has been so successful that they have strong visibility into growth for the next 5 years, BUT BAM’s MO has been to say “15% to 20% growth for the next 5 years,” and each year they extend that timeline because of another year of strong fundraising.

If the AI boom were to sour, then wealthy and large institutional investors might suddenly decide that alternative assets, with their long lock-ups and high fees, aren’t worth it.

Think of it this way. GNG Research has some giant “whales,” including one RIA member who manages $57 million for others.

That member may own Brookfield Asset Management, but why doesn’t he put his clients' $57 million (or at least some of it) into a Brookfield fund?

Because why would he? BAM is paying a safe 3.6% (backed by the industry's most stable cash flow) and growing 19%.

Is a Brookfield fund going ot deliver more than 24% returns? After fees?

Why not get paid 3.6% to earn 22% to 23% long-term?

If enough rich people and institutions decide that BAM’s funds aren’t worth it, then BAM is in trouble.

And that’s also true for the alternative asset management industry in general.

Now the good news is that this isn’t a big risk, given all the wealth in the world, seeking areas of strong volatility-adjusted returns.

That’s the thing to remember. An institutional money manager isn’t going to forgo investing in a BAM fund because “Nvidia is doing so well, why do I need to pay you 2% and 20% when I can own Nvidia.”

No one is going to leave a hedge fund because the S&P is red hot for so long that “Why shouldn’t we be 100% low-cost index funds!?”

Institutions have fiduciary rules and responsibilities that don’t permit them to go “all in” on anything, but alternative assets have been struggling to return capital to investors, which means it might become trickier to keep raising new capital to secure the growth BAM is guiding toward.

For now? No problem, BAM is setting records at fundraising, but it’s the only real risk to the thesis that needs to be kept in mind. Something that might end the decades-long period of Buffett-like returns for which Brookfield is known.

Fact-Check & Other Risks To Consider

Bottom Line: Brookfield Is The World’s Best AI Dividend Stock

There are lots of companies yielding 3.6%.

There are lots of companies growing by 19%.

I don’t know of any that offer both, but even if there is one, Brookfield offers not just 22% to 23% CAGR total return potential for 5 years, but potentially for decades.

The global infrastructure boom, even before AI, was massive, around $5 trillion per year needed for 30 years, according to Brookfield.

Now we have Nvidia, Morgan Stanley, IDC, and Citigroup estimating $3 to $4 TRILLION PER YEAR in data center spending alone…by 2030!

That means the global infrastructure funding requirement will double within 5 years.

Funding all that is going to take governments, hyperscalers, debt markets, sovereign wealth funds, and every source of capital you can imagine.

And companies like Brookfield? They have 123 years of expertise and reputation that grease the wheels, open the wallets of institutional clients, and make infrastructure magic happen on six continents.

I can’t think of any alternative asset manager more suited to a global AI Boom than Brookfield, and when you factor in a 3.6% yield and 18% to 20% dividend growth for 5+ years? Well, that’s the kind of AI dividend opportunity that I don’t just recommend, I turn it into a core holding of the ZEUS fund.

Because at the end of the day, I believe in paying brilliant people to manage my family’s money better than I can.

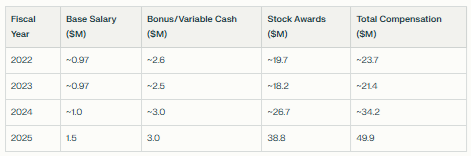

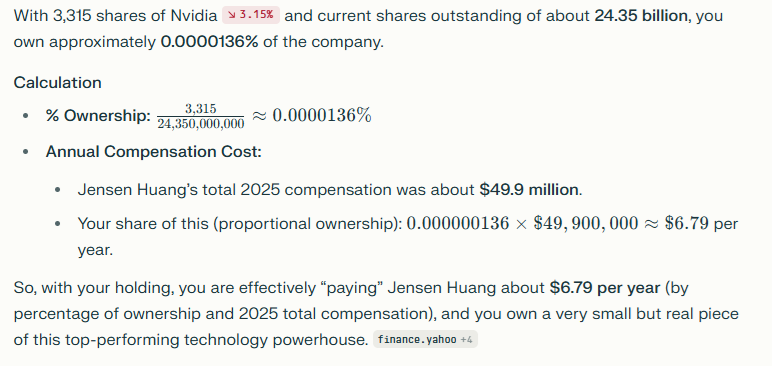

This is How Much The Greatest CEO In History Makes

Every Nvidia shareholder pays Jensen 0.2 cents per share to run the company.

Well, with Brookfield, you are getting paid to have Bruce Flatt, Howard Marks, and, until he became the Prime Minister of Canada, Mark Carney, oversee the Brookfield empire and PAY YOU dividends!

How would you like it if Jensen paid you to own Nvidia shares? Well, Brookfield is a chance to have the world’s best infrastructure experts make smart deals on your behalf, and then pay you for the privilege of making you rich.

That’s the kind of deal that I find so sweet; it makes me grateful we live in a world so wonderful that this is actually legal😉