Introduction

Hello everyone, my name is Michael Shterk and I am interning here at GNG Research for the 2026 Summer. I am going into my fourth year at the University of Colorado Boulder and pursuing a bachelor of Economics. This publication is my first attempt at deep diving a company. There are easier things to talk about but I am glad I was challenged by the team to work on something that is super sector specific.

When looking at REITs you have to take a step back from everything you’ve been taught and really think about what you’re looking at, wether it’s material, metrics, and even sector competition. I look forward to reading and responding to your comments and or feedback.

Summary

Every so often the market hands you a business whose price and underlying worth have begun to drift apart, and Rayonier Inc. (NYSE: RYN) looks like one of these moments. The shares bubble around $20.87, not far from the 52 week low, while the company sits on more than four million acres of American timberland. I think that land is worth considerably more in a private market than what the public market is willing to pay for it at this moment.

The thesis is simple and is reduced to two things: a price that sits beneath the replacement cost of the underlying land, and a dividend that rewards patience investors while that gap closes. GNG’s valuation model has fair value at $33.22, which puts the stock at a 37.2% discount and earns a “Strong Buy”. I want to be straight about what kind of call this is though. This is a value call, and not a momentum one. Our own quantitative model rates the shares a Hold at 49.5 out of 100, and Wall Street agrees, with a mutually understanding pointing to roughly a 24% upside. This split is the entire story. The asset base is cheap and the market’s short term, however the momentum driven lens has rewarded it yet.

The Company That Just Got a Lot Bigger

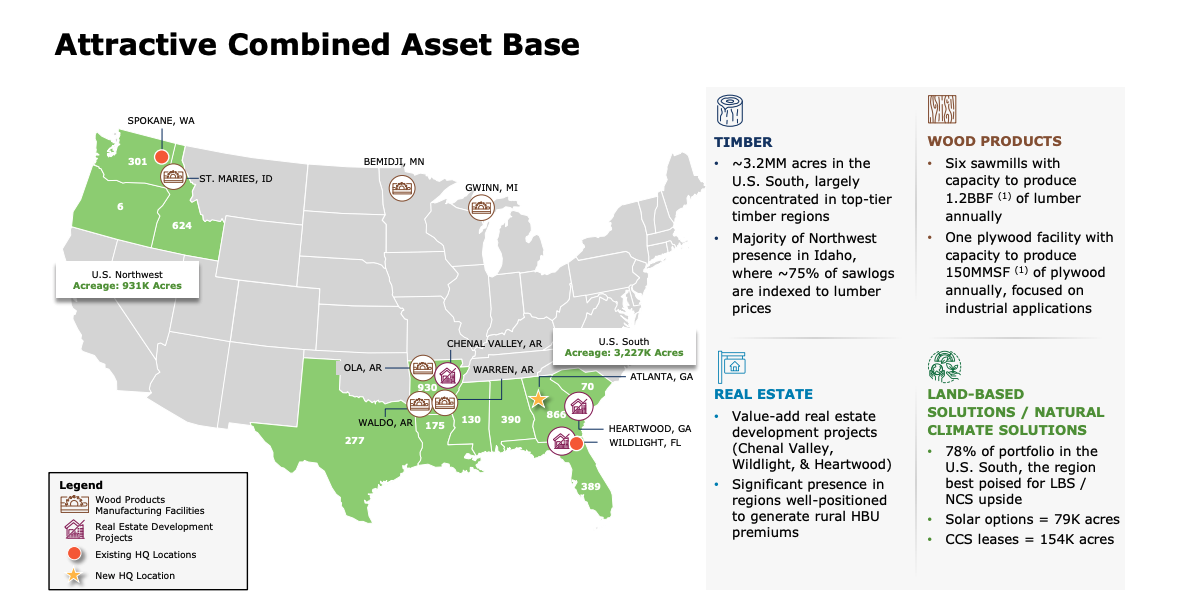

On January 30th, 2026, Rayonier closed on a merger with PotlatchDeltic Corporation. This deal was done ahead of schedule, and overnight Rayonier became the second largest publicly traded timber and wood product company in the United States. Roughly 4.1 million acres of diverse timberland, six sawmills, and an industrial grade plywood mill. Long time legacy Rayonier shareholders ended up with about 54% of the combined company and PotlatchDeltic holders with about 46%. With some talks between leadership, the company decided to keep the Rayonier name and the RYN ticker. In the infographic below this section you can look at company’s management and how the merger brought both sides together.

The merger was much more than just getting larger. The merger rebuilt the business around four reporting segments, Southern Timber, Northwest Timber, a brand new Wood Products manufacturing arm, and real estate. The manufacturing piece plays a pivotal role, because the roughly 1.2 billion board feet of lumber captivity gives Rayonier real world leverage to a housing and lumber recovery when the time comes. Rayonier management has also penciled in about $40 million in annual run rate synergies within two years of closing, most of it coming from trimming the overlapping corporate and operational costs.

The Asset Floor: Why Timberland Is Different

The heart of my thesis comes down to what Rayonier actually owns. Timberland is real, you can walk on it, an appraiser can value it, and it tends to hold up when inflation is running hot. What it’s not is a lease stream that lives and dies by rent multiples, and is not a contract book that depends on one big customer. The difference is exactly why I landed on Rayonier instead of the alternatives in the sector. Weyerhaeuser (NYSE: WY) is the obvious comparison, the largest publicly traded timber REIT at roughly $17.6 billion, and in many ways the bluest of blue chips in the space. But size is doing a lot of the work in its valuation.

This is something Rayonier cannot match up against. WY trades near $24.50 at a normalized P/E north of 100x, pays a thinner dividend yield of about 3.4%, and even Morningstar pegs its fair value around $28.44, which leaves far less room than the discount I see in Rayonier. You are paying a premium for scale and liquidity rather than buying a discount to the dirt, and that is the whole distinction. Rayonier gives me the same hard timberland backing with a wider margin between price and asset value.

Rayonier’s acreage puts a hard floor under the stock. With roughly 4.1 million acres in the ground, even small changes in what we can assume each acre is worth moves the equity value a long way. GNG’s fair value at $33.22 sits comfortably above today’s price, with Wall Street pointing higher as well. My read is that the market has simply not caught up to the larger, more diversified company that the merger brought. The pricing is based on old news and yesterday’s Rayonier.

Getting Paid to Wait

Waiting for the market to come around is a lot easier when you collect a check in the meantime. On a trailing basis, Rayonier’s $1.42 in dividends per share comes out to roughly a yield of 6.8%. Here is an honest footnote that I’m obligated to share and belongs right next to that number: the trailing figure is flattered by a one time $1.40 per share special which was paid in December as part of the merger. The board has since reset the quarterly dividend to $0.26. Either way you look at it, the income is competitive for the sector, and the GNG’s safety model scores the payout favorably, with a Safety Score near 66.71%.

Let’s talk about coverage. This is where a lot of people misjudge timber REITs. If you look at trailing free cash flow, the dividend looks tight, which is not a surprise for a capital heavy land business in a year where the price is somewhat soft. But free cash flow is the wrong metric here.

The right one is Adjusted Funds From Operations, or AFFO, and this basically adds back depletion and other non cash chargers that GAAP treats as money walking out the door. On that basis, coverage has historically had more room to breathe with management reporting the figure every quarter. I think that dividend is backed by real operating cash rather than financial engineering, but I would still tell investors and readers to keep an eye on AFFO coverage as the company’s numbers settle down.

What Closes the Gap

A cheap asset only matters to me if something eventually wakes the market up, and Rayonier has a few things working in its favor. The most interesting is what the company calls higher and better use land sales. This is where they sell acreage for far more than it is worth as working timberland. In the first quarter of 2026, Rayonier sold land to a solar developer for more than $10,000 an acre, and it has a solar option pipeline of roughly 80,000 acres behind it. This is where the real optionality lies, and a plain timberland valuation completely misses it.

There is more. The company is sitting on a cash balance it can seriously put to work, and is already doing so. To start they bought back about 1.5 million shares for $31.1 million to what I think is a discount to a net asset value. Add in the rough $40 million synergy target, the ongoing integration of PotlatchDeltic’s timberlands and mills, and a possible upward bounce in lumber prices, and you have several ways for value to surface.

The Early Numbers Back It Up

Early 2026 was the first look at the combined company, and it came with two months of post merger results baked in. I’ve read the headline GAAP figures with some care and recommend you do the same. Rayonier reported a net loss of $12.4 million, or five cents a share, however that number swallowed $70.4 million of pre tax merger costs. Strip this out and the other one time items out, and the pro forma net income was $17.4 million (seven cents per share). The cleaner read on the business is Adjusted EBITDA, which jumped to $94.1 million from $27.1 million a year before, as well as cash available for distribution right alongside it.

$276.8 million of revenue came in, and every segment chipped in. With no surprise to me, Real Estate stole the show, where the solar deal and broad based land sales pushed results past management’s own timid expectations. Newly added Wood Products turned a profit in a soft lumber market, with prices drifting higher as the new year went on.

The Balance Sheet Is Not Where the Risk Lives

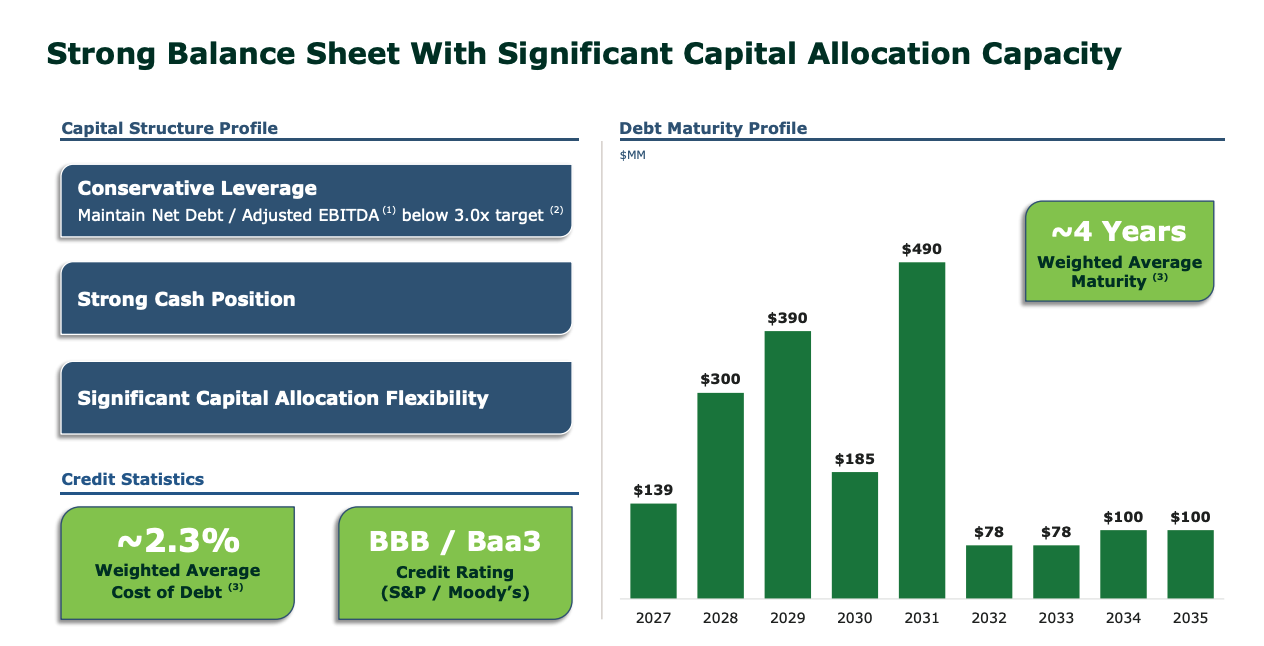

I’m going to say this plainly: this is a valuation and cycle story, not a solvency story. As of March 31, 2026, Rayonier held about $681.7 in cash against a rough figure of $2.06 billion of debt. Management is steering toward a Net Debt to Adjusted EBITDA ratio under 3.0x through the cycle. They have also made a commitment to keeping its investment grade credit ratings.

After merging, the company reworked its facilities into a $200 million revolver that matures in 2030 and roughly $1.61 billion of term loans which are laddered out through 2035. With all this the set up leaves plenty of room for the dividend, buybacks, and an opportunistic deal.

My interest is the whole story and with this a couple of yellow flags come up from mechanical screens. Rayonier’s Altman Z Score lands in what we call the distress zone, and its Piotroski F Score is middled with a 5 out of 9. I’m not losing sleep over either. These read to me as quirks of a capital heavy, asset rich RIET whose earnings are hidden under merger accounting and a weak pricing cycle.

Therefore in my eyes these do not read as warning signs of real trouble. The Z Score was built for industrial and manufacturing companies and in my experience has a habit of misreading land rich REITs. Fair is fair, and investors alongside with readers should put them on the scale next to the bull case.

Valuation: The Gap IS The Whole Point

Industry standard earnings multiples do not get you far with a company like this. GAAP earnings are bouncy and right now they are scrambled or cluttered by merger accounting and big land sales. The way that makes most sense to me is to look at Rayonier’s EV to EBITDA on the combined company’s forward earnings, the dividend yield, and above all what the land is actually worth. The ticker trades at about 0.64 times book and well under GNG’s $32.22 fair value.

I’m personally deciding to chalk this discount up to an undervalued asset base, and not anything going wrong in the business itself.

That split in the ratings is the most interesting thing to me on the page. GNG’s valuation model sees deep value at a 37.2% discount, while GNG’s own quant model and Wall Street both sit on Hold. This is weighed down by soft timber and lumber pricing and the usual noise that comes with integration. I read this hesitation as the market fixates on the next few months while the most important part which is the value of the land goes unnoticed. I am happy to be on the other side of that.

What Could Go Wrong

I am not going to sit here and pretend it’s sunshine and rainbows. Timber, pulpwood, and lumber prices are cyclical, and in this very moment soft right now. Delivered pine pulpwood realizations slipped enough to notice ($30.20 a ton down from $37.83 a ton from a year earlier). A housing market that continues to stay weak for an extended period of time would lean on both the timber and wood products.

Merging two companies this size carries real execution risk, and the synergies are back loaded for a number of upcoming years, so patience is required and a virtue.

As a REIT with floating rate debt, Rayonier feels interest rates twice over in its borrowing costs and in how much the market prices the yield. Because real estate and solar revenue tends to come in big chunks, the quarterly numbers will stay bumpy for a while and I would be lying if I said not to expect some sort of turbulence. Size the position accordingly, and do not expect a straight line.

The Bottom Line

Rayonier brings together something you do not see often. With a real hard asset backing, a competitive income stream, a balance sheet that can take a punch, and a price that sits below what the assets are worth. Post merger this company is bigger, more diversified, and in better shape than the market seems to realize. Timberland underneath it all gives you a floor that rent multiple and single customer competitors just cannot offer.

You are essentially buying dirt below replacement cost and getting paid to wait. GNG’s valuation model calls Rayonier a Strong Buy at a $33.22 fair value, a 37.2% discount to where it’s trading today. I read the Hold ratings from Wall Street and from GNG’s own quant model as an ode and comment for the upcoming months, this by all means is not a verdict on what the land is worth. The land is where my conviction sits firmly and comfortably.

Thank you for reading and again I look forward to many prolonged discussions wether it’s the comments or our rocket chat.